The ABC’s business editor, Ian Verrender, reports that the National Broadband Network (NBN) has been plagued by cost over-runs and delays in its rollout. This is due primarily to the decision to use a mix of fibre-optic and copper cables, alongside the generous $11 billion deal struck by the Gillard Government to compensate Telstra for customers migrating across from its fixed-line service.

These factors, according to Verrender, have resulted in many Australians missing out on high-speed internet access, alongside paying premium prices.

With the NBN rollout nearing completion, the federal government will be keen to offload it. However, there are likely to be few buyers and they will not be prepared to pay anywhere near the cost of building it. As such, Telstra is shaping up to gain control of the NBN at a peppercorn price and, thus, could ultimately play a major role in the future of the network:

The NBN is on the books with a $51 billion valuation tag, but the Parliamentary Budget Office in June last year calculated its fair value at just $8.7 billion.

Of the $51 billion total, the Federal Government has an equity stake of just under $30 billion with most of the remainder debt held by the NBN.

If and when the project is sold, that debt will travel with the NBN to its new owners. So it is the equity stake, the value of the shares, that is the sensitive issue for us as taxpayers…

There’s also some dodgy accounting practices that render it slow and expensive.

To keep the NBN “off the books” and not part of the federal budget, the Rudd government classified the project as an “investment” rather than just government spending. That facade has been maintained by the Coalition.

As an investment, however, the NBN has to deliver a commercial return. That means it needs to cover its costs, plus a bit on the top. And so, given the cost blowout, it’s had to charge the telco companies an arm and a leg to achieve that goal.

They, in turn, have to offer a decent priced service to customers, and the only way they can do that is by skimping on the speeds.

The end result? We pay a fortune for a sub-standard service.

So how do we fix it?

The only solution to this is for the Federal Government to write down the value of the project and take the financial hit.

If it wrote down that $30 billion equity stake to just $8.7 billion, that would crystallise a $21 billion loss, which would hit the Federal Budget and our national debt…

It may seem like a rerun of an old horror movie but Telstra, the company that did everything it could to thwart a fibre-optic cable rollout in order to profit handsomely from it, may end up playing a key role in the NBN’s future…

The Gillard government struck an $11 billion deal with Telstra in a desperate attempt to get the project to fruition…

Ironically, a big reason the NBN is so expensive is the overly generous deal the Gillard government struck with the company back in 2012…

Whatever the outcome, it’s highly likely Telstra shareholders will end up reaping most of the benefits of the NBN at the expense of taxpayers.

Telstra is shaping up as the nation’s biggest winner from the NBN debacle.

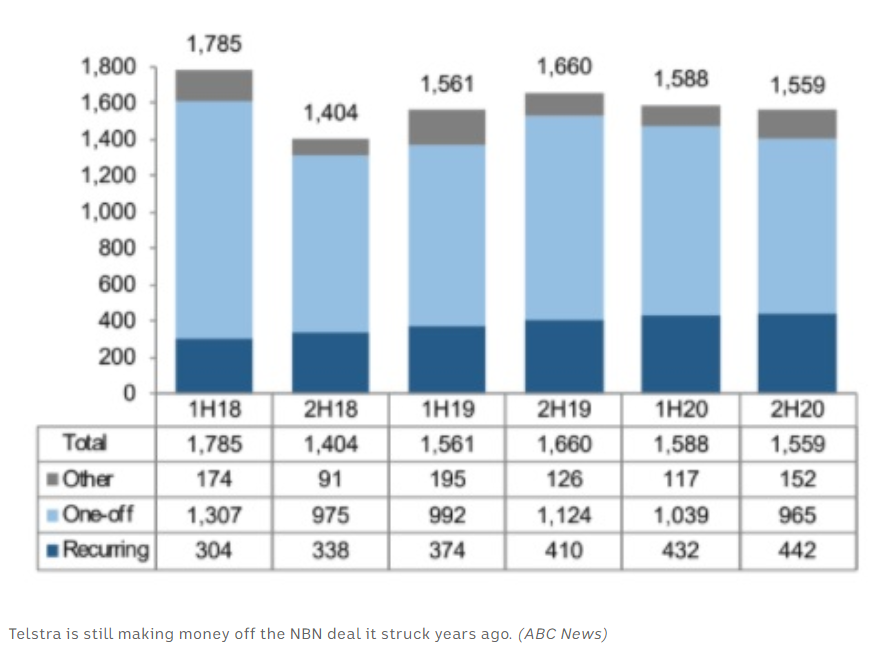

In 2011, the Gillard Government agreed to pay Telstra $11 billion in instalments for its fixed line customers to migrate to the NBN, which have lined Telstra’s pockets ever since:

This decision to pay installments was made, in part, to fix the structural mess made when the Howard Government privatised Telstra in the late-1990s, which gave Telstra control of both the wholesale and retail fixed line networks, thus creating a vertical integrated monopoly.

While it has received billions of dollars in annual installments, Telstra has also worked actively to undermine the NBN by demanding deep price cuts to its wholesale charges, as well as by pledging to steal market share via Telstra’s 5G mobile broadband rollout.

Now we’ve got Telstra’s infrastructure arm, InfraCo, lining up to acquire the NBN at a peppercorn price, which would once again hand it control of both the wholesale and retail networks.

History doesn’t repeat but it sure does rhyme.