By Chris Becker

The divergence between reality and Wall Street grows ever stronger with equity markets outside Manhattan continuing their sideways or lower moves as valuations get stretched. But the NASDAQ and S&P500 both put in new record highs on Friday night as hope continues to delude traders as the USD slumped to a new two year low against almost everything, particularly Australian dollar and Pound Sterling. The shock resignation of Japanese PM Shinzo Abe rocked local markets but also the continued market response to the new inflation targeting method of the US Federal Reserve.

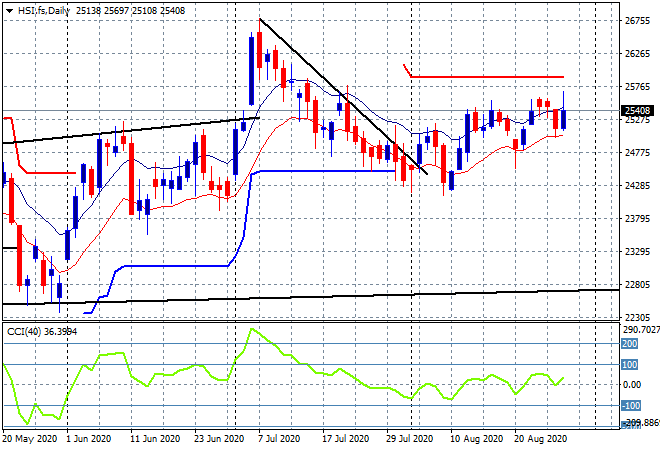

Looking at share markets in Asia from Friday’s finishing session where in mainland China the Shanghai Composite was able to finally crack the 3400 point barrier, putting in a new three month high, up 1.6% to 3408 points while in Hong Kong the Hang Seng Index lifted more sedately by 0.5% to 25422 points. Price was ready to push higher again through resistance around the 25400 point level but as I’ve warning all of last week there’s still considerable selling pressure ahead despite the positive daily momentum. Watch for a potential break below the low moving average here, but its likely this will follow Chinese stocks:

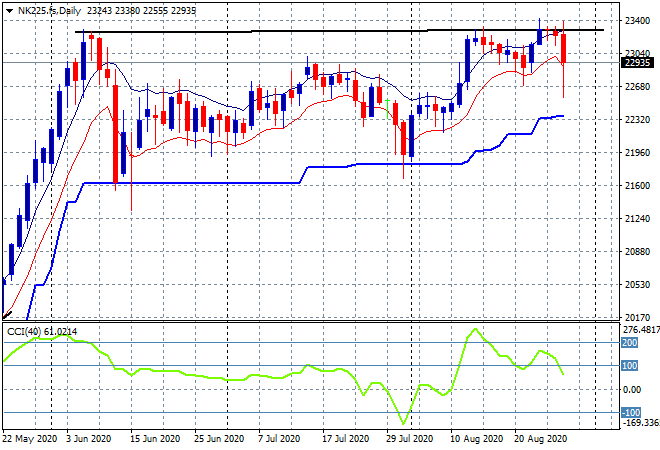

Japanese stock markets were looking set to breakout on Friday but the sudden resignation of PM Shinzo Abe saw the Nikkei 225 stumble over 2% lower before marginally recovering to finish 1.4% lower at 22882 points. Futures are indicating a staid start to the trading week as resistance at or around the 23400 point level on the daily chart continues to be rejected, but watch for some potential support around the 22700 point level:

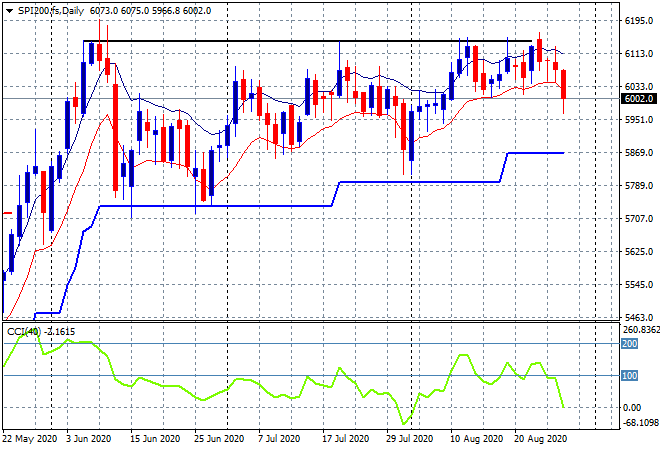

The ASX200 managed to fumble at the end of the week closing down 0.9% to 6073 points as earning season rolled on while the Australian dollar shot ahead significantly to new weekly highs, putting a dampener on local results. SPI futures are down just over 40 points with a potential to break below the magical 6000 point barrier despite the big up sessions on Wall Street. The daily chart of the SPI reveals a market unable to make substantial headway with significant resistance above, mostly due to the lack of confidence in banking stocks (which make up half the index):

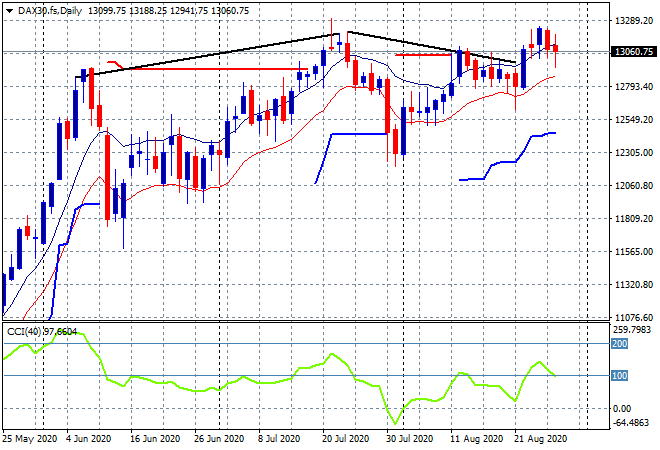

European markets stumbled yet again, with scratch sessions across the continent as a much higher Euro and Pound Sterling weighed on stocks. The German DAX retraced again after recently hitting a new monthly high by closing nearly 0.5% lower to 13033 points. The daily chart had been looking to clear the triple top bearish pattern but this rollover may have legs – watch for any further retracement below the 13000 point level:

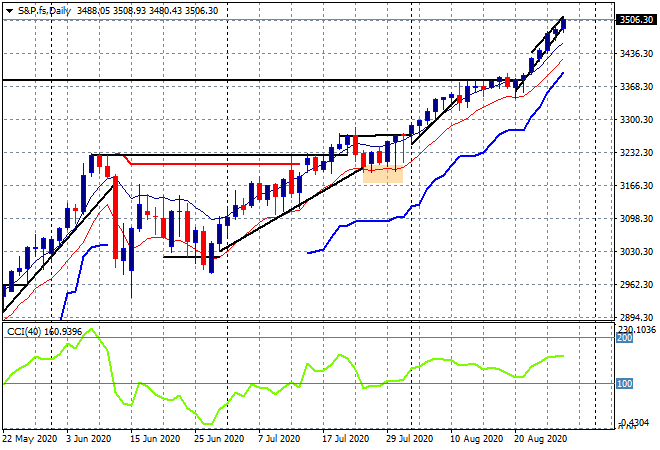

Wall Street was all guns firing as the Fed kept up the juice with the NASDAQ to a new record high by 0.6% while the S&P500 broke through the 3500 point barrier, closing with a 0.7% gain to 3508 points. The daily chart continues to show a market well overbought and ready to pop even higher, but you just can’t stop this music:

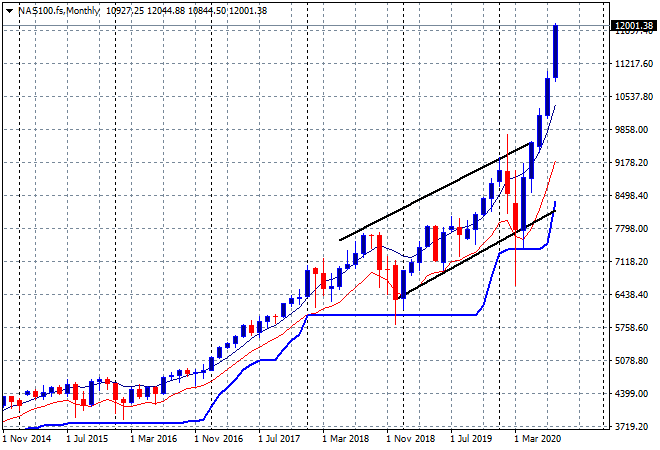

NASDAQ can’t stop the music, even though by rights it should be nearer 9000 points, not 12000:

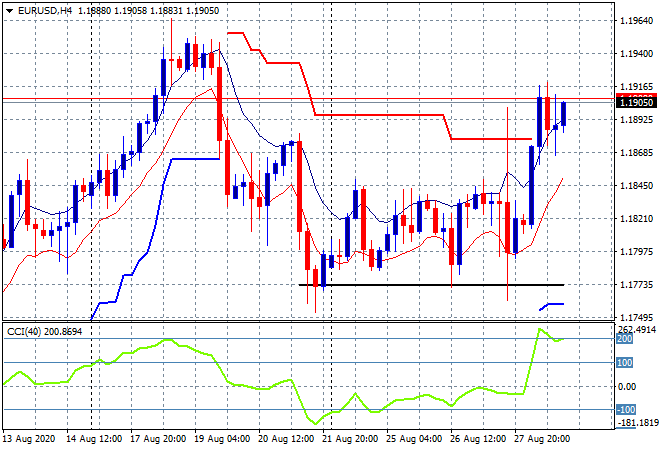

Currency markets were quite volatile with the Abe resignation and the US PCE release unexpectedly going higher, with the US Dollar Index hitting a new two year low. Yuan also accelerated its gains against USD, now at a 2020 high while Euro advanced and stuck up through the 1.19 handle finally making good on its mid week breakout. Four hourly momentum is now nicely overbought and ready to engage the previous weekly high at the 1.1950 level:

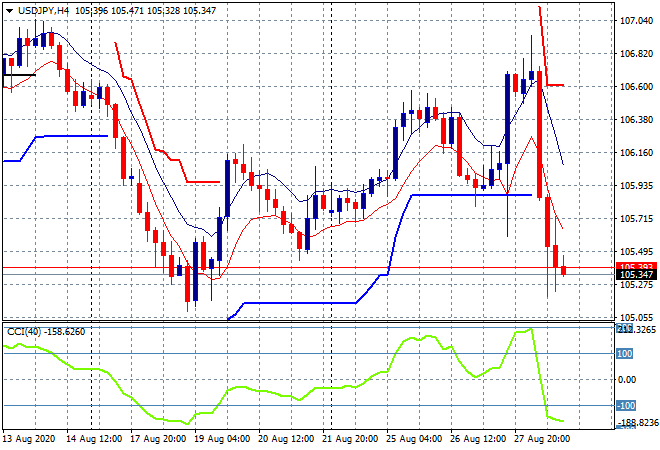

The USDJPY pair had the most volatility as Yen buyers lept in on the Abe resignation on the possibility that “Abenomics” may be coming to an end. The pair swung down violently towards the 105 handle and stayed there, almost making a two week low which shows that this move may only be a precursor of what is to come. Watch for the 105 handle proper to come under pressure this morning on the weekend gap open:

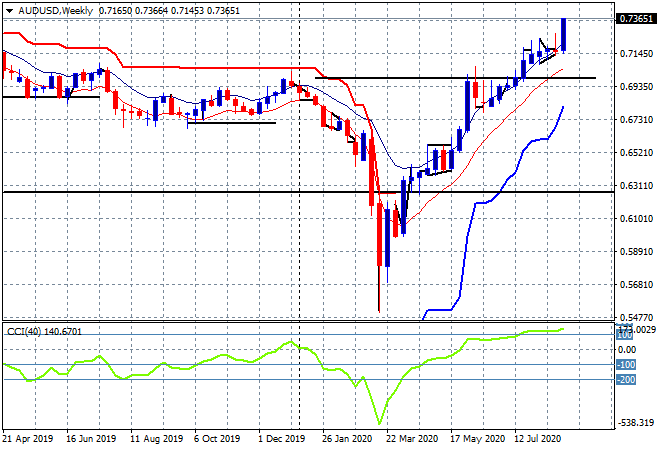

The Australian dollar launched over 100 pips higher on Friday, breaking out above the 72.50 level and closing the week out at another new high for 2020, back to late 2018 highs just below the 74 handle. How far can this go? Certainly not parity, but the weak USD meme will take it a bit further from here, with my terminal target still at 80 cents believe it or not:

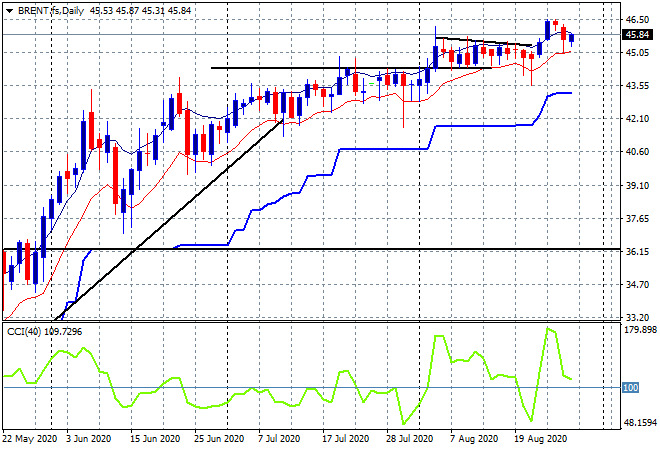

Oil futures fell back over 1% on Friday night despite the lower USD with Brent pulling back below the $46USD per barrel level again. This breakout doesn’t look like extending higher and maybe a one off as price gravitates back to the long held neutral positions at or around the $45USD per barrel level:

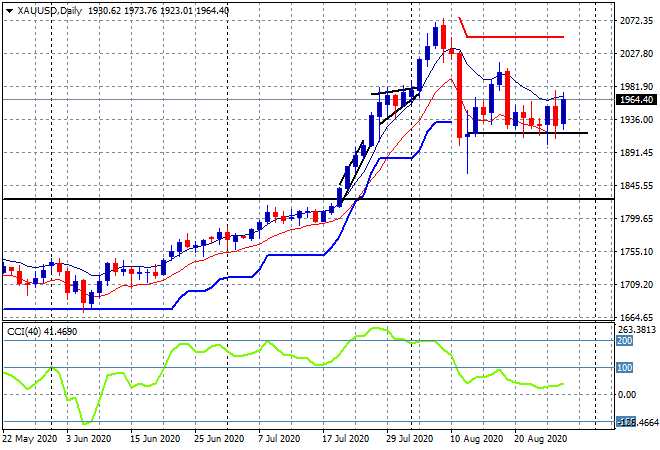

Gold is slowly firming here, mainly due to the new inflation expectation by the Fed, but not responding as violently as I expected. Price continues to be supported at the several week long $1930USD per ounce level, but needs a bit more momentum here before calling a new uptrend in comparison with other undollar assets:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

BOJ/Abenomics: Bank of Japan, economic policy/direction enacted by PM Shinzo Abe

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!