By Chris Becker

You can’t beat the optimism out of Wall Street which surged again on tech stocks exuberance, this time on Microsoft taking over TikTok, plus a big beat in US manufacturing conditions. This will lift all boats here in Asia while the USD lifted slightly against the majors, with gold putting in another record high but only just.

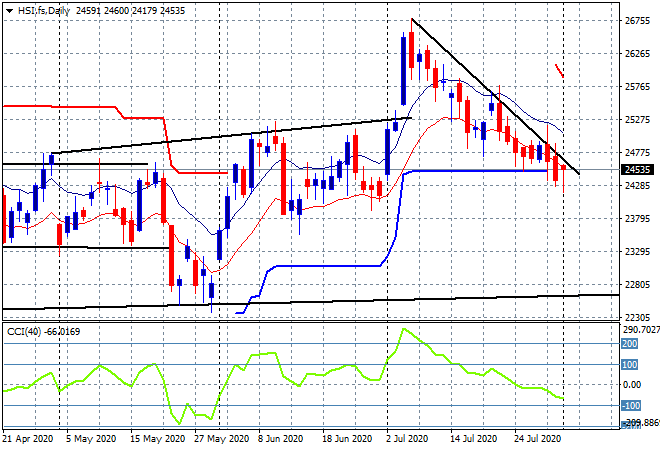

Looking at share markets in Asia from yesterday where in mainland China, the Shanghai Composite had a solid day, closing 1.7% higher at 3367 points, while in Hong Kong the Hang Seng Index continued its divergence to slip 0.8% to 24397 points. This shunts price just below trailing daily ATR support with momentum pushing into the negative zone but the overall dour mood may reverse here as futures indicate a fill on that decline, but wait for the downtrend line to be broken decisively before getting excited:

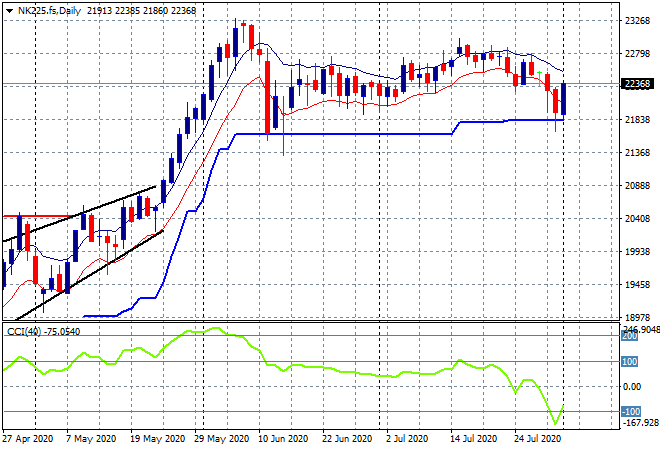

Japanese stocks bounced back from their bad Friday session, with the Nikkei 225 lifting over 2% to 22195 points to a two month high, pulled along by a much higher USDJPY pair. Futures are up this morning in line with Wall Street with price looking to bounce up from key support at both the daily ATR and weekly price level at 21800 points but this market still looks very weak:

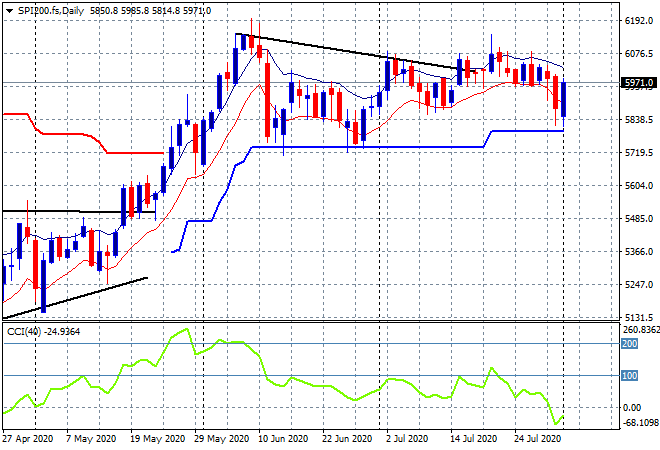

The ASX200 was still wobbly, falling a few points to remain well below the 6000 point level, closing at 5926 points as a softer Australian dollar helps calm the losses from the expected fallout of the Victorian shutdown. SPI futures however are up more than 80 points or over 1% as hopium returns Down Under so we could see a break above 6000 points on the open, possibly until the RBA meeting in the afternoon where questions about any sustained rally in the medium term will be asked:

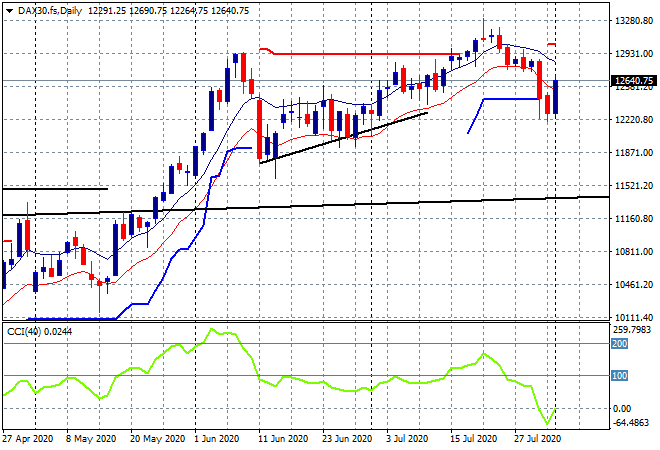

European markets threw away their bad news playbook and went full in to catch up to Wall Street with 2-3% daily returns the norm across the continent. The German DAX was the strongest, closing 2.7% higher to 12646 points, as momentum decisively rebounded back into positive mode on the daily chart, as price clawed back above ATR support. A very solid one day bullish reversal which has for now forestalled a proper trend reversal below 12000 points:

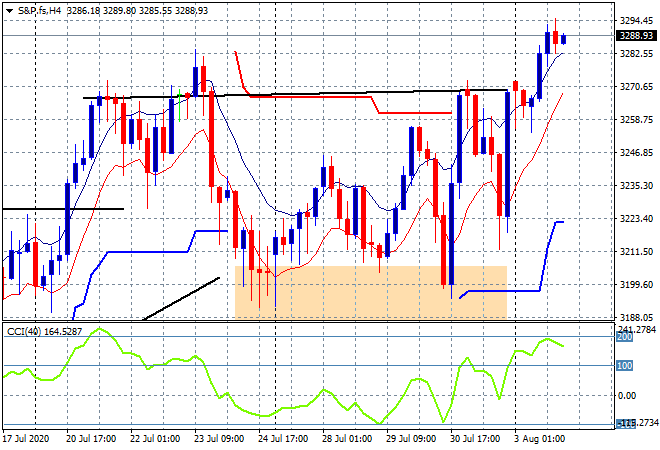

Wall Street continues to run on hopium and delusion, with tech earnings still outweighing all the underlying trends with the S&P500 finishing 0.7% higher to 3294 points, surpassing the previous record high alongside the NASDAQ (up 1.5%) as well. The four hourly chart show price clearly breaching previous resistance and looking nicely overbought ready for the next stage:

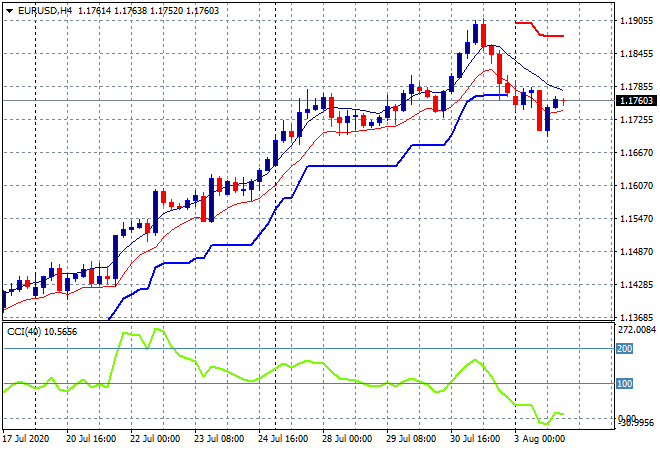

Currency markets are oscillating back to a weaker USD but only in fits and spurts with Euro still unable to recover from its start of week shunt, finishing up this morning below the 1.08 level and in a downtrend. Trailing ATR support remains broken on the four hourly chart with momentum almost negative as price stabilises somewhat, watch the session lows at 1.1720 for signs of another follow through:

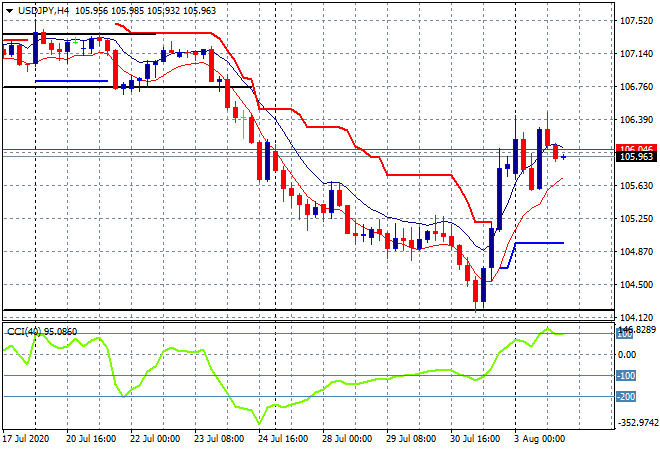

The USDJPY pair remains bid higher following its Friday night reversal, remaining above the 106 handle before weakening slightly this morning. This second stage whipsaw has seen four hourly momentum get into overbought mode with the low moving average untouched, the usual signs that more upside is possible from here, but volatility bears watching:

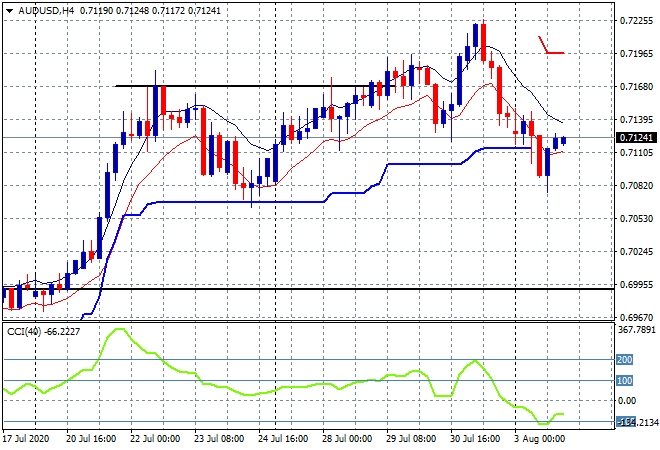

The Australian dollar is still falling against USD, heading below the 71 handle overnight before a late reprieve this morning as traders await today’s RBA meeting, which is expected to have no change except in language around the Victorian lockdown. Momentum remains oversold with price finding a small amount of support here at the 71 handle, but not making a new weekly low:

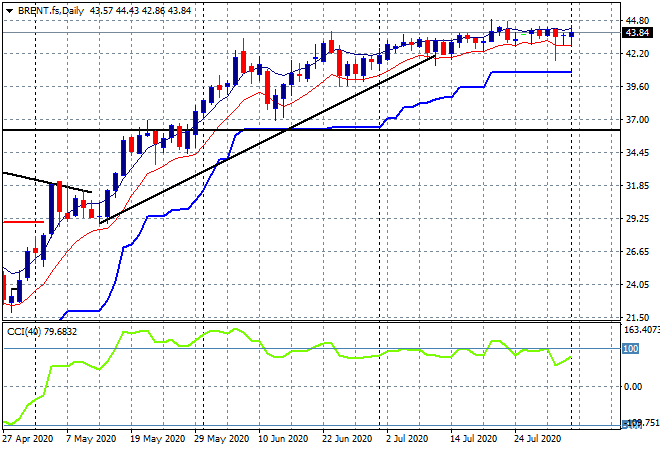

Oil futures rose again but only just with the Brent marker remaining shy of the $44USD per barrel level again. The daily chart still shows a sideways bullish trend with price still unable to make a volatile breakout or breakdown as per usual for the black gold:

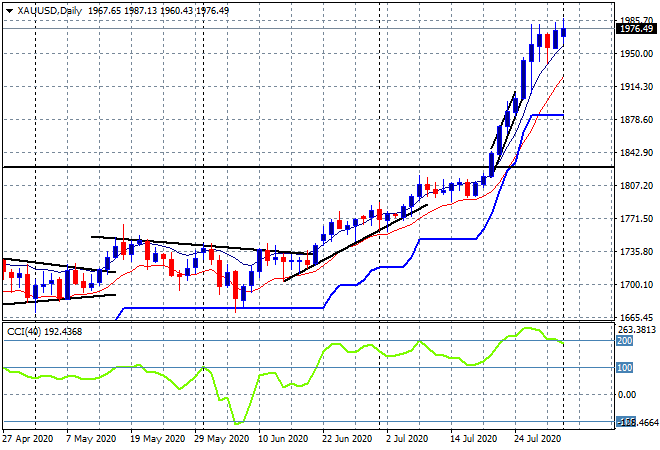

Gold remains untouched by the sell off in other undollars with another record high but only just with a few dollars gained to the $1976USD per ounce level. The daily chart still shows a market impatient for further upside as this short term consolidation still requires more breathing room before another retest of the $2000 level:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

BOJ/Abenomics: Bank of Japan, economic policy/direction enacted by PM Shinzo Abe

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!