Even before COVID-19 hit, Aussie households had become more prudent.

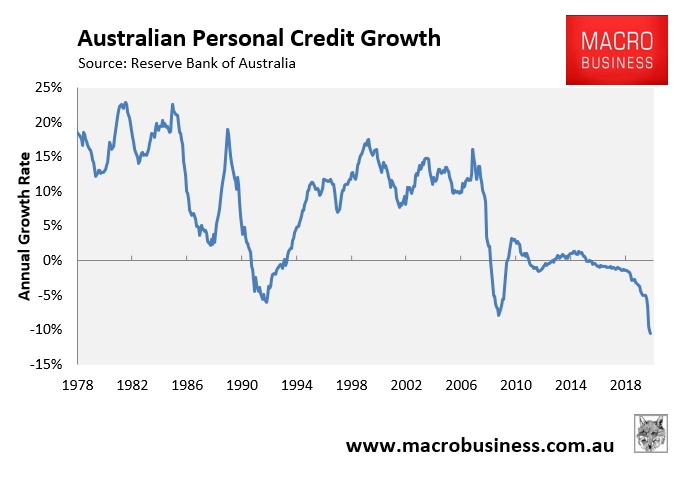

Personal loan growth had plummeted into negative territory:

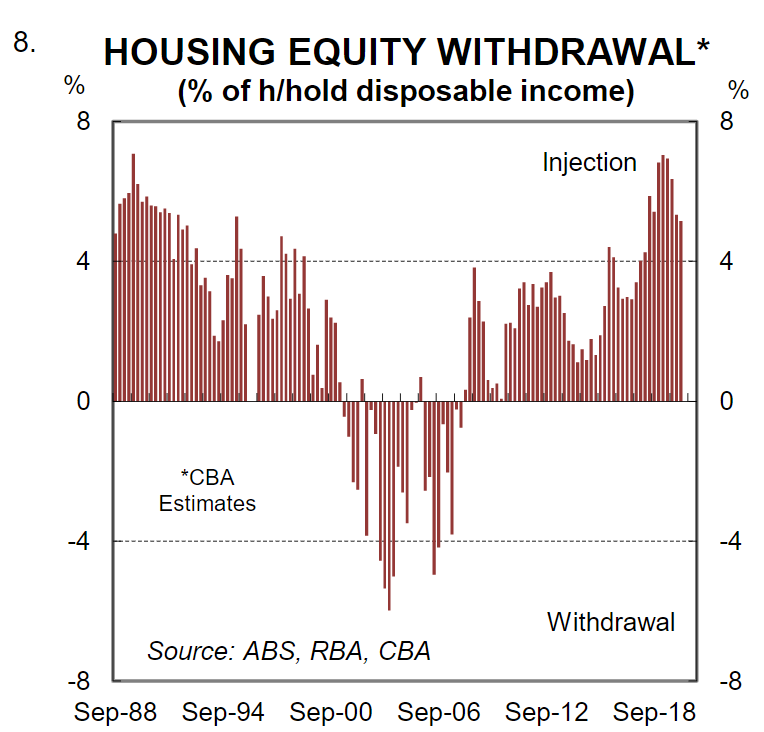

Mortgage equity injection was running near the highest level in living memory:

Advertisement

Even before COVID-19 hit, Aussie households had become more prudent.

Personal loan growth had plummeted into negative territory:

Mortgage equity injection was running near the highest level in living memory:

The full text of this article is available to MacroBusiness subscribers