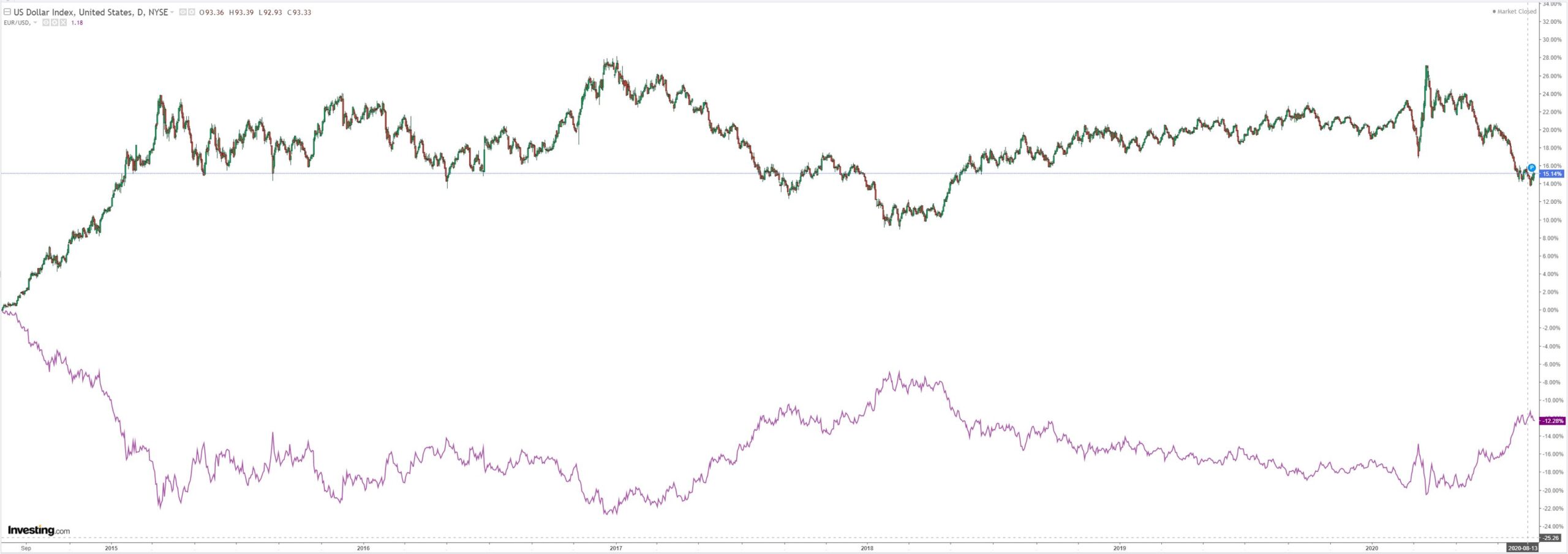

DXY was firm last night:

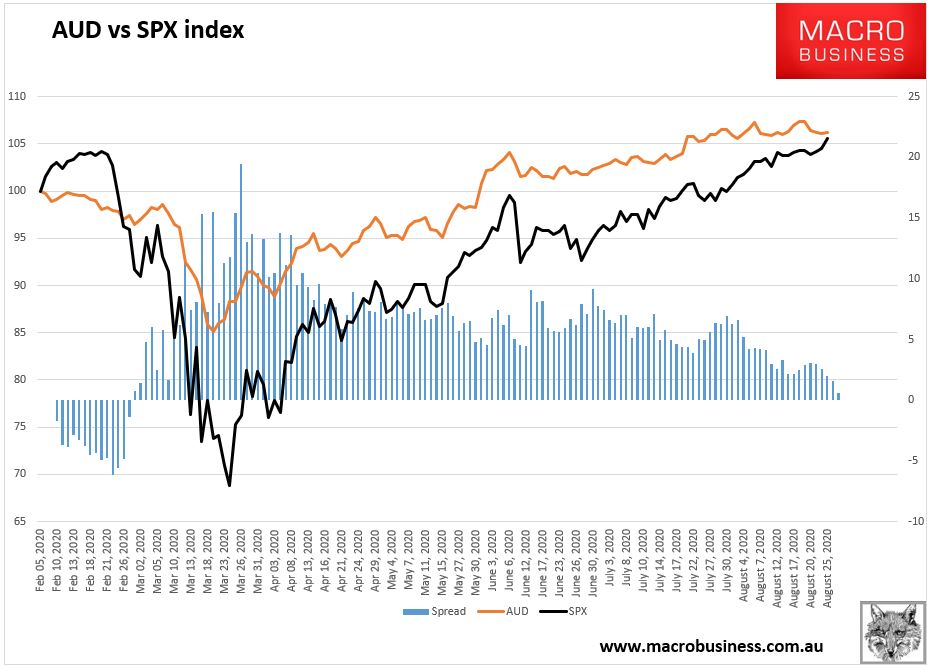

The Australian dollar was roughly flat:

Gold looks shaky in terms of its ongoing correction:

Brent is stuffed until WTI catches up:

Metals were OK:

And miners:

EM stocks jumped but couldn’t hold:

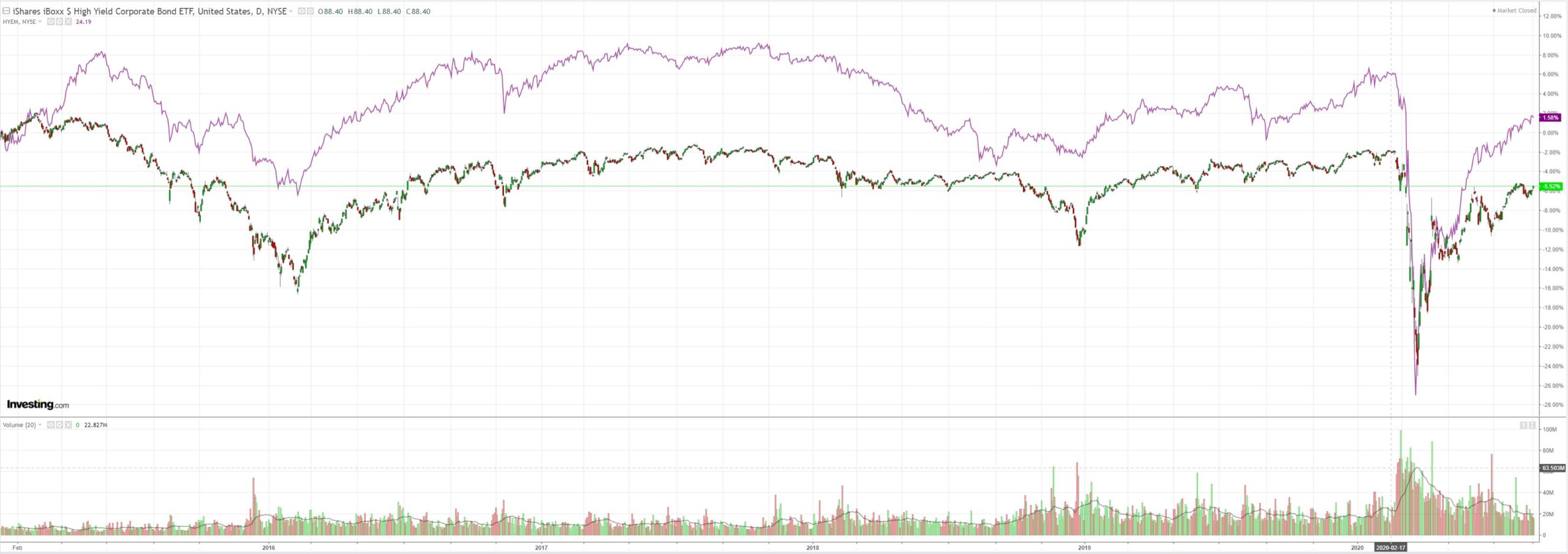

Junk firmed:

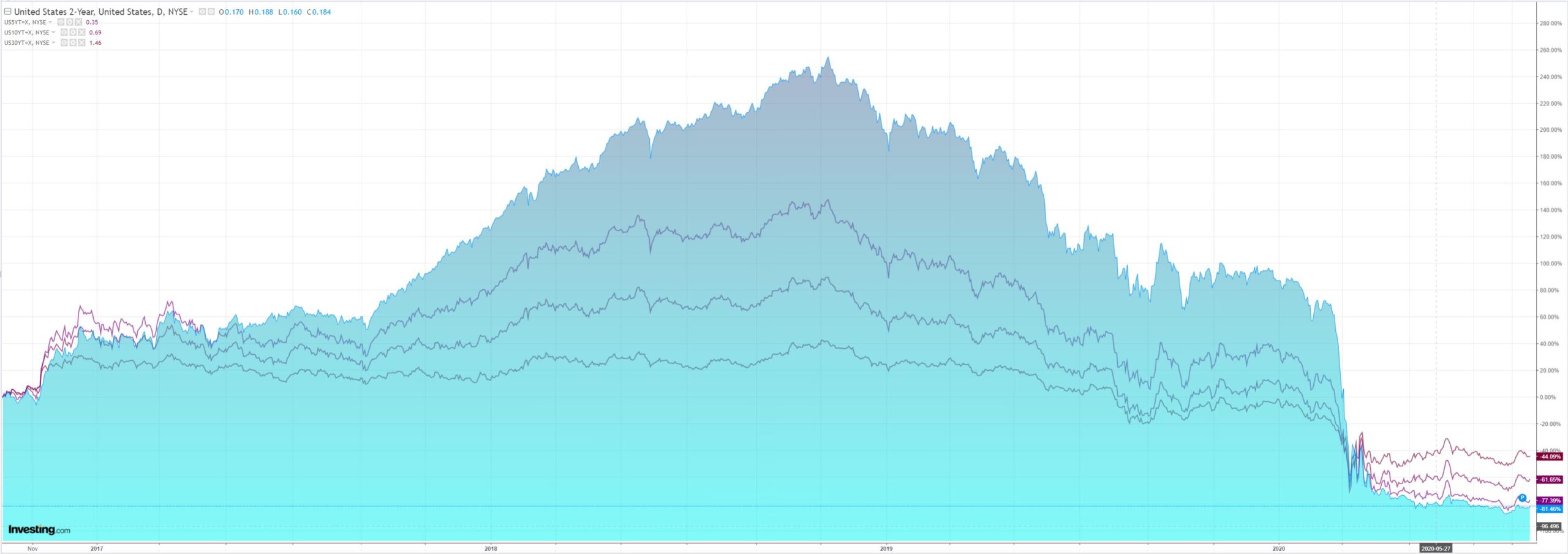

Despite rising yields:

The Nasdaq bubble swelled:

The only chart that matters has almost ceased to matter:

Westpac has the wrap:

Event Wrap

US Chicago Fed. National Activity survey for July: the index fell to 1.18 from an upwardly revised record high of 5.33 (initially 4.11) in June. For context, the index had been between -0.5 and +0.5 since mid-2009 before plunging to almost -18 in April (a record low). 56 of the 85 indicators made positive contributions. The July decline is consistent with other indicators for a month which saw virus cases rise and re-openings stall.

Positive recent developments on the Covid vaccine front included weekend news that the U.S. Food and Drug Administration is working to expand access to a virus treatment involving blood plasma from recovered patients. Separately, the Financial Times reported that the Trump administration is considering whether to bypass regulatory standards to accelerate an experimental vaccine.

Event Outlook

Australia: Weekly payrolls for the week ending 8 Aug are likely to exhibit an emerging loss of momentum due to the Melbourne lockdown.

Germany: The August IFO business climate survey is on a clear upward trend as the virus continues to be reined in (prior: 90.5, market f/c: 92.2).

US: The FHFA house price index captures data with a lag. The May result of -0.3% reflected contracts signed under stay-at-home orders in Mar/Apr; prices are forecast to lift 0.3% in June. Similarly, the market expects the June S&P/CS home price index to rise from 0.04% to 0.1%. New home sales point to a return to normal conditions for home demand, aided by low mortgage rates. Sales are seen rising from 775k to 785k in July. Sentiment as indicated by the August Conference Board consumer confidence index is improving, but policy gridlock remains a material risk (prior: 92.6, market f/c: 93.0). New shipments and orders suggest further gains lie ahead for Richmond Fed district manufacturers (prior and market f/c: 10). FOMC’s Daly will speak on inequity and COVID-19 (05:25AEST).

The Great Fakeflation rolls on but the Australian dollar is increasingly left behind. I put this down to a number of factors:

- the long EUR, short DXY trade is overstretched;

- doubts about more Fed easing (though stocks don’t care);

- Australian growth prospects are terrible, even relative to everywhere else as its immigration-led model implodes;

- increasingly, the tech bubble is overtaking all markets and Australia has no part in it.

I still think that so long as the Great Fakeflation persists then DXY will resume its weakness and drive commodities plus AUD higher but it’s no longer a slam dunk and could reverse for a goodly period to work off market imbalances.