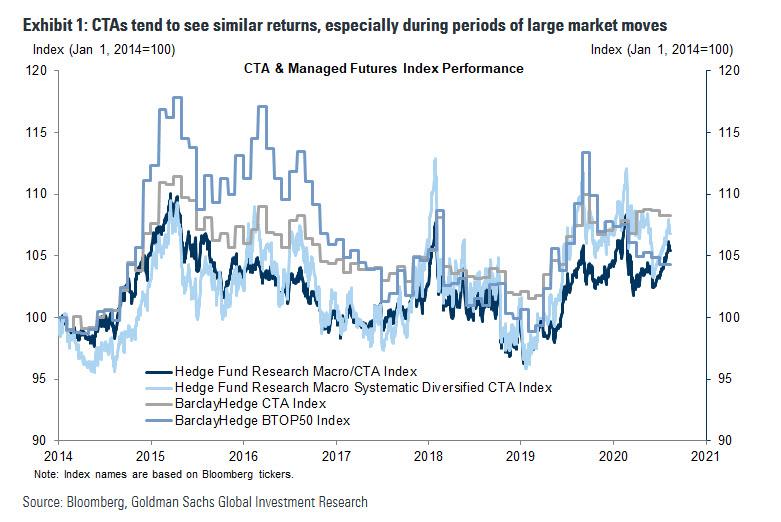

Momentum-based trading systems have been popular for decades, given their low correlation with traditional benchmark returns and, therefore, their potential for generating alpha. The strategies tend to have common components, including set rules for entering and exiting positions. Although there are a variety of methods employed to produce a trade signal, many rely on simple moving averages—such that a buy (sell) is triggered if spot moves above (falls below) a specified moving average. Other popular methods include “crossover strategies,” where a trader goes long (short) if a faster-moving average exceeds (breaks below) a slower-moving average, and “breakouts,” where a trader buys (sells) an asset if spot surpasses (undershoots) the prior high (low) over a certain time horizon. For example, the “Turtle Experiment” of 1983 relied primarily on a breakout-based system, according to Faith (2013). Despite the different methodologies, CTAs tend to see similar returns, especially during periods of large market moves (Exhibit 1). In fact, according to Clenow (2013), most of the variation in returns between funds comes from factors such as asset composition, risk level, and position size, rather than the specific trade signal.

…even though CTAs are probably already short Dollars, we see scope for further weakness as (i) fresh shorts could be triggered soon and (ii) longer-term investors start to participate as well, particularly in the Euro and other European assets.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.