The Grattan Institute has shot down Paul Keating’s, Labor’s, and the superannuation industry’s incessant scaremongering over the Morrison Government’s early superannuation release policy, claiming that it will only reduce retirement incomes by around 1% for the typical worker:

Policy makers can only justify forcibly lowering someone’s living standards during their working life – by lifting compulsory super – if we are protecting them from even worse outcomes in retirement.

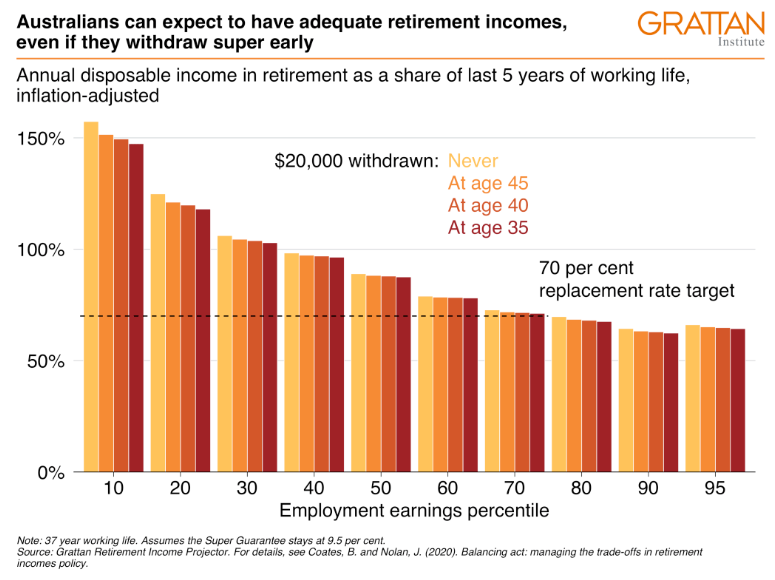

Nonetheless, our modelling shows that Australians can look forward to a comfortable retirement with compulsory super contributions of 9.5 per cent, even if they take the full $20,000 from their super.

Workers on all but the highest incomes will retire on incomes at least 70 per cent of their pre-retirement (post-tax) earnings – the so-called ‘replacement rate’ benchmark used by the OECD and others.

The median worker earning around $60,000 who takes out $20,000 in super at age 35 would see their replacement rate fall from 89 per cent to 88 per cent, assuming compulsory super stays at 9.5 per cent, still well above the 70 per cent benchmark.2

Even if COVID means they remain unemployed for the next three years, making no super contributions, that worker would still end up with a retirement income of 86 per cent of what they earned in the years before retirement. And the more than 500,000 Australians that have emptied their super accounts completely, the impact on their retirement incomes is likely to be smaller since they have, by definition, withdrawn less than $20,000.

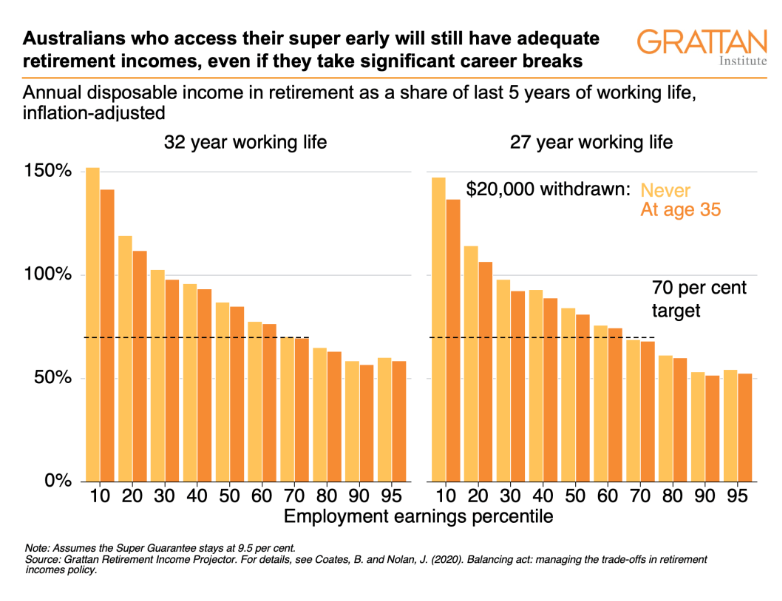

Retirement incomes would also remain adequate even for the many Australians who access their super early and work part-time or go on to take significant career breaks, such as to care for children. For example, someone who works for 32 years at the median income, and takes out $20,000 in super, will see their retirement income drop from 87 per cent to 85 per cent of their pre-retirement earnings. A median worker that only works 27 years and takes $20,000 in super would see their retirement income fall from 84 per cent to 81 per cent of their pre-retirement earnings.

Of course, some low-income Australians remain at risk of poverty in retirement – especially those who rent. But struggle even more before they retire.

And boosting Rent Assistance would do far more than higher compulsory super to help these vulnerable Australians, and without reducing their take-home pay before they retire as higher compulsory super would.

Brendan Coates also advised against lifting the superannuation guarantee to 12%, noting that it would lower wages and would hamper the economy’s recovery from COVID-19:

Before COVID-19, there were good reasons to abandon the planned increases in compulsory super. COVID-19 is just one more reason.

Higher compulsory super would reduce workers’ take-home pay and do little to boost the retirement incomes of many Australians, while widening the gender gap in retirement incomes. The Government’s early release scheme does nothing to change that story.

The government will bear much of the cost of the super early release scheme via higher pension payments when today’s workers retire.

But raising compulsory super to 12 per cent would make the problem worse, since higher super costs the budget more in extra super tax breaks than it saves in lower Age Pension spending for decades to come.4 It’s a $2 billion a year hit to the budget once super hits 12 per cent, and those extra super tax breaks skew heavily to the wealthiest 20 per cent of Australian workers.

But most importantly, higher compulsory super would also exacerbate the economic problems caused by COVID-19. Past Grattan work has shown that higher super comes at the expense of workers’ wages. And the Reserve Bank agrees: it’s forecasting lower growth in wages next year when compulsory super begins to rise.

Scheduled increases will see household savings rise at a time when aggregate demand is weak.

Raising super in the midst of a deep recession would only slow the pace of economic recovery. And that would be bad news for all Australians, regardless of the size of their super account.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.