According to Martin North’s Digital Finance Analytics surveys, the majority of Australians still believe that property values rise on average every seven years.

In the above video, Martin North sets the record straight, busting this myth using a number of examples.

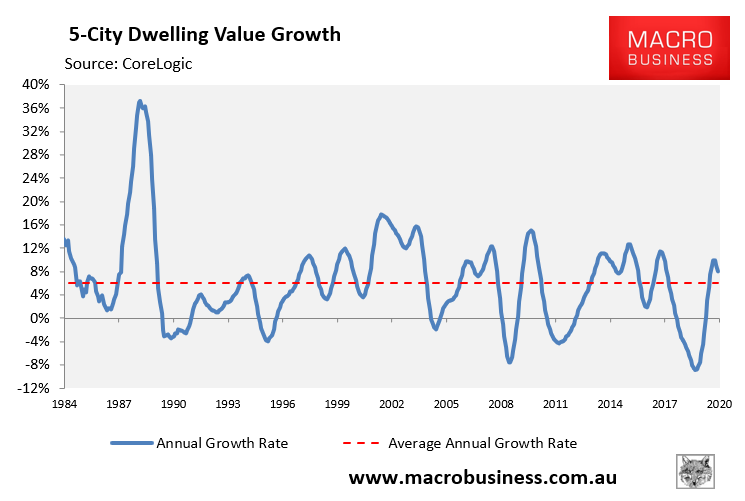

For Aussie property to double in value every seven years, values would need to grow on average by about 10% per annum. This has not happened over the past 40 years, as illustrated in the next chart:

According to CoreLogic, property values have grown on average by 6.0% per annum at the 5-City level since 1980. This means that prices have doubled every 12 years on average.

Nor should these types of growth rates be anticipated in the future.

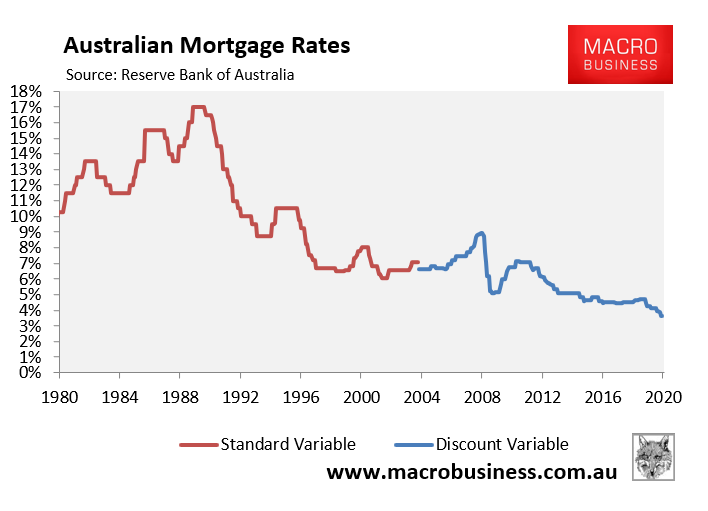

Australian mortgage rates plummeted from 17% in 1990 to a record low 3.65% currently, which is a key reason why property values have risen so much.

However, with the RBA cash rate now at a rock bottom 0.25%, and with no room to drop, Australian property values will no longer benefit from the strong tailwinds of falling mortgage rates. This means that prices will have to rely on rising household incomes to push them higher, which are also likely to be constrained going forward.

Hence, expect minimal real growth in Australian property prices in the future, even after the COVID-19 pandemic passes.

As an aside, I’d also like to remind readers of the free Property Calculator launched this year by our partners at Nucleus Wealth. This allows you to look at growth scenarios for residential property.