by Chris Becker

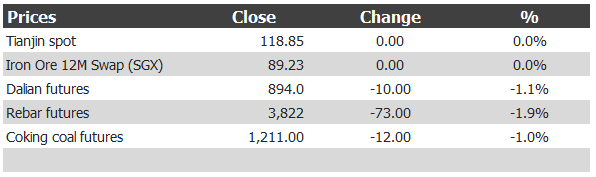

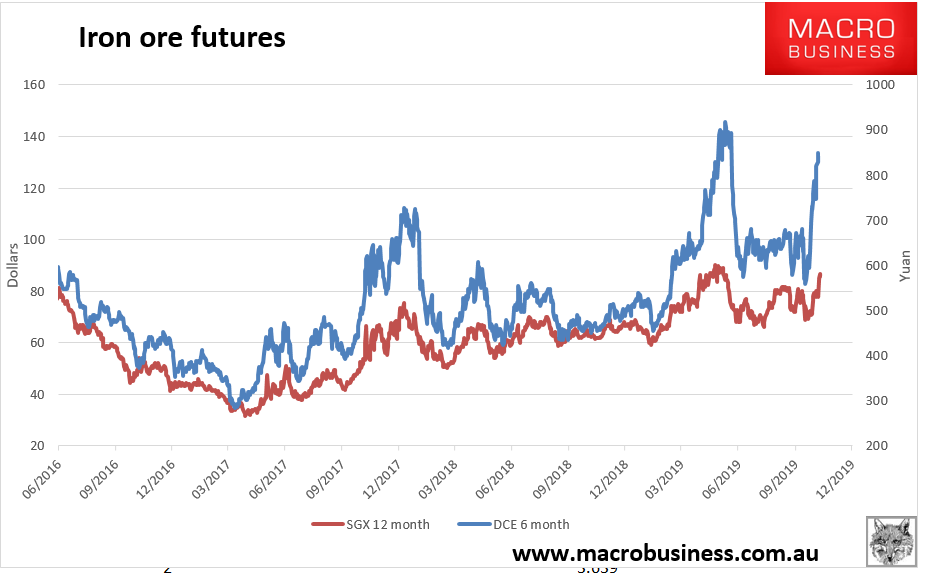

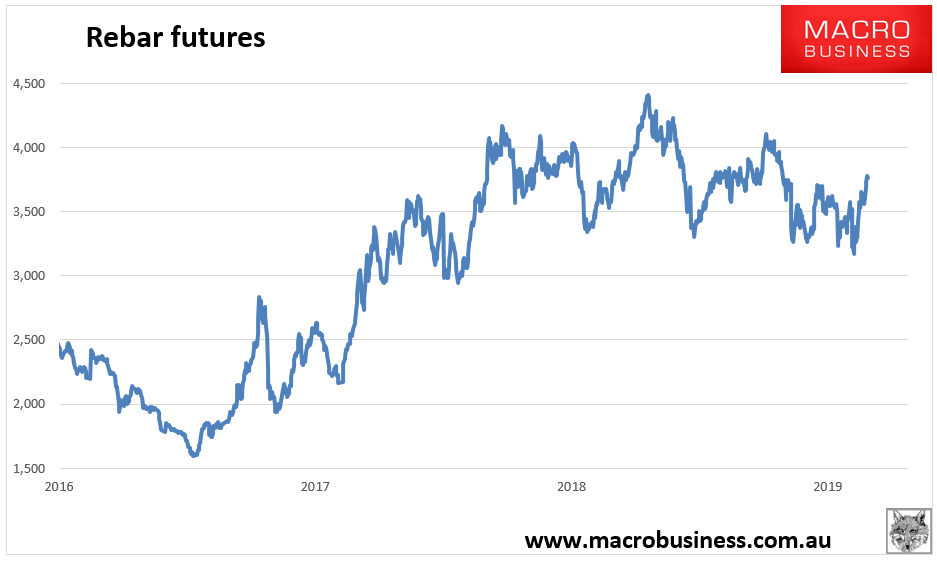

The iron ore complex is having a mixed start to the week due to the Singaporean holiday, with spot prices and 12 month Singapore futures unchanged, while Dalian futures dropped on increased US tensions:

Advertisement

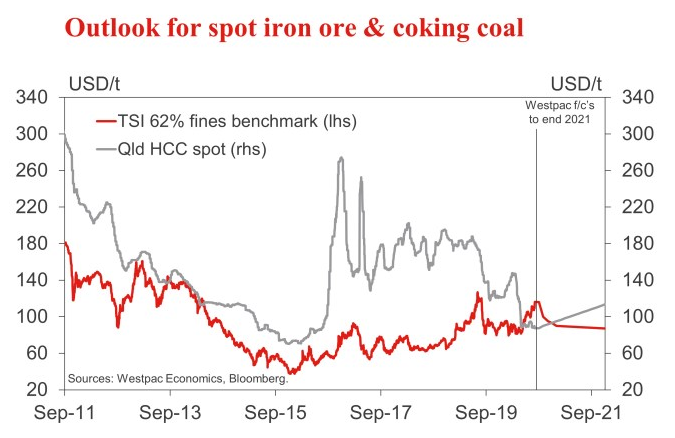

Westpac are still moderately bullish with a $100US per tonne forecast, but see a decline down to $87 by the end of 2021 as supply concerns mount:

Advertisement