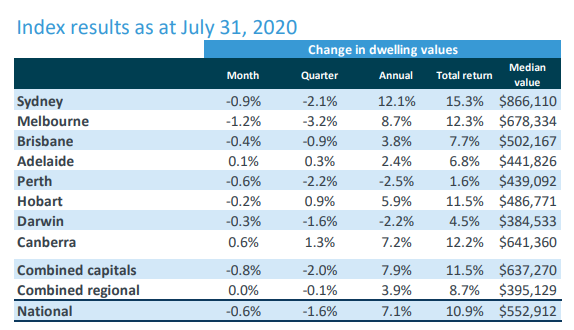

CoreLogic has officially released its dwelling value results for July, which reported an “orderly” 0.8% decline in values across the capital cities:

According to CoreLogic’s head of research, Tim Lawless, housing markets have remained relatively resilient through the COVID period so far. “The impact from COVID-19 on housing values has been orderly to-date, with CoreLogic’s national index falling only 1.6% since the recent high in April and housing turnover has recovered quickly after it’s sharp fall in late March and April.”

“Record low interest rates, government support and loan repayment holidays for distressed borrowers have helped to insulate the housing market from a more significant downturn. Advertised supply levels have remained tight, with the total number of properties for sale falling a further 4.3% in the 4 weeks to July 27th , sitting 15.2% below where they were this time last year. Additionally, increased demand driven by housing specific incentives from both federal and state governments, especially for first home buyers, have become more substantial”…

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.