CBA’s economics team has released more stunning data showing the extend to which government emergency income support is propping up the Australian economy:

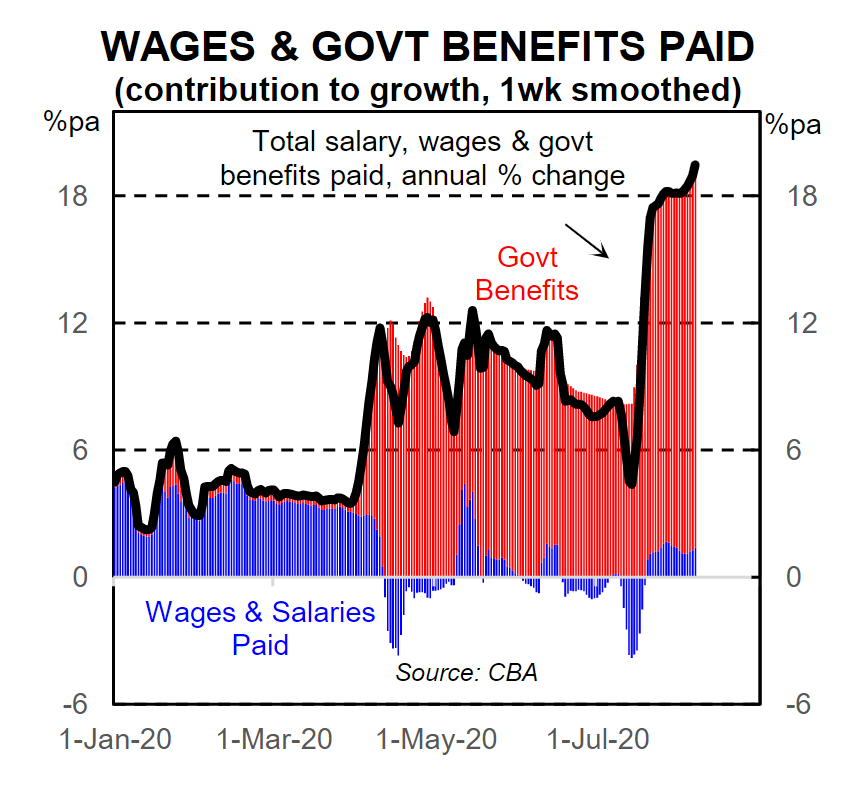

Household income has surged in recent weeks primarily due to government payments(latest data to 7 August).

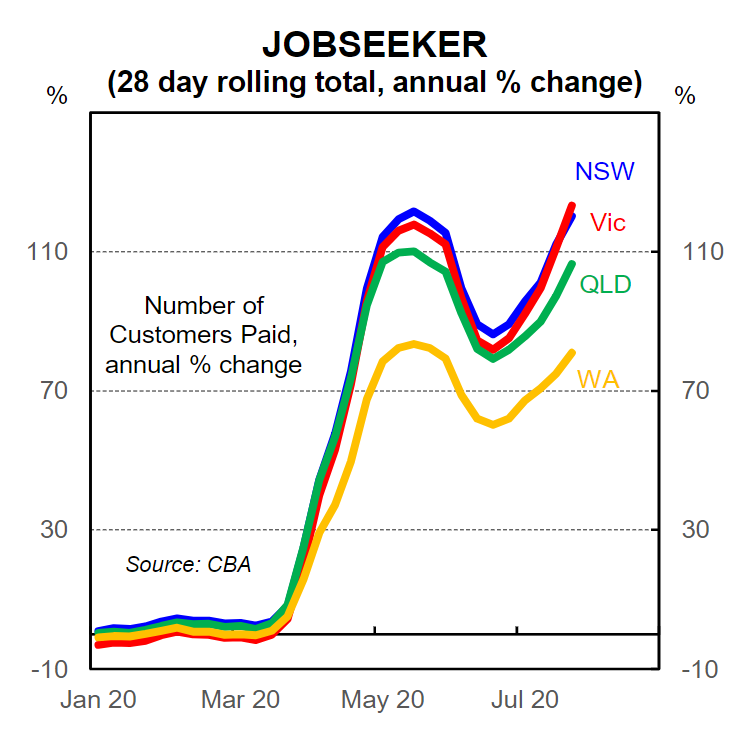

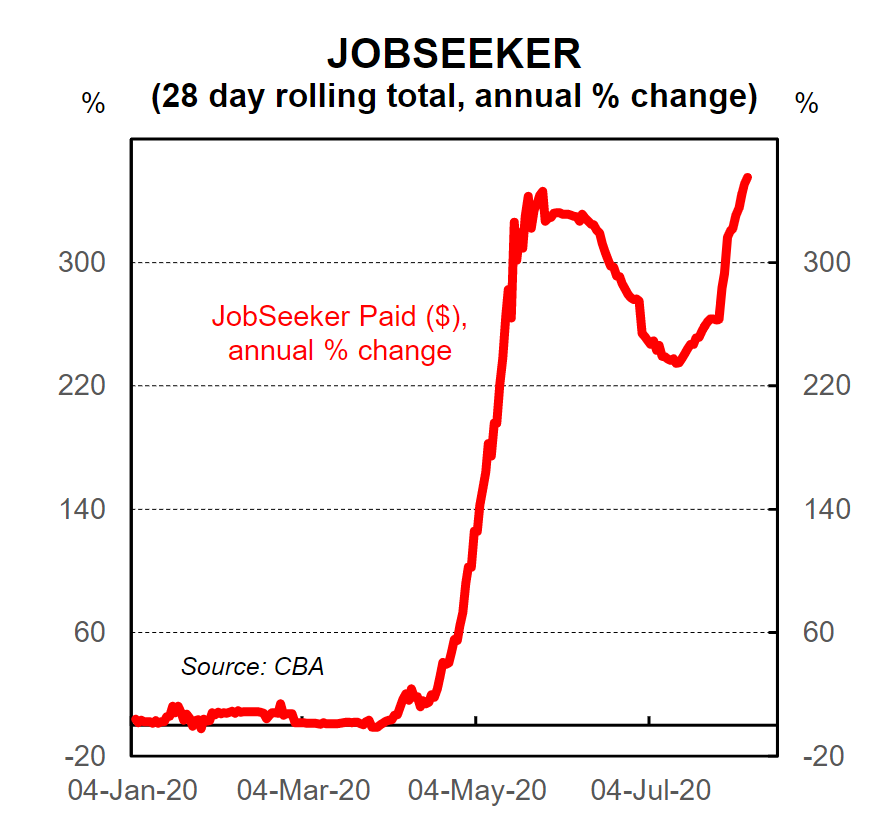

The number of people receiving JobSeeker has been increasing since early July across all states and territories.

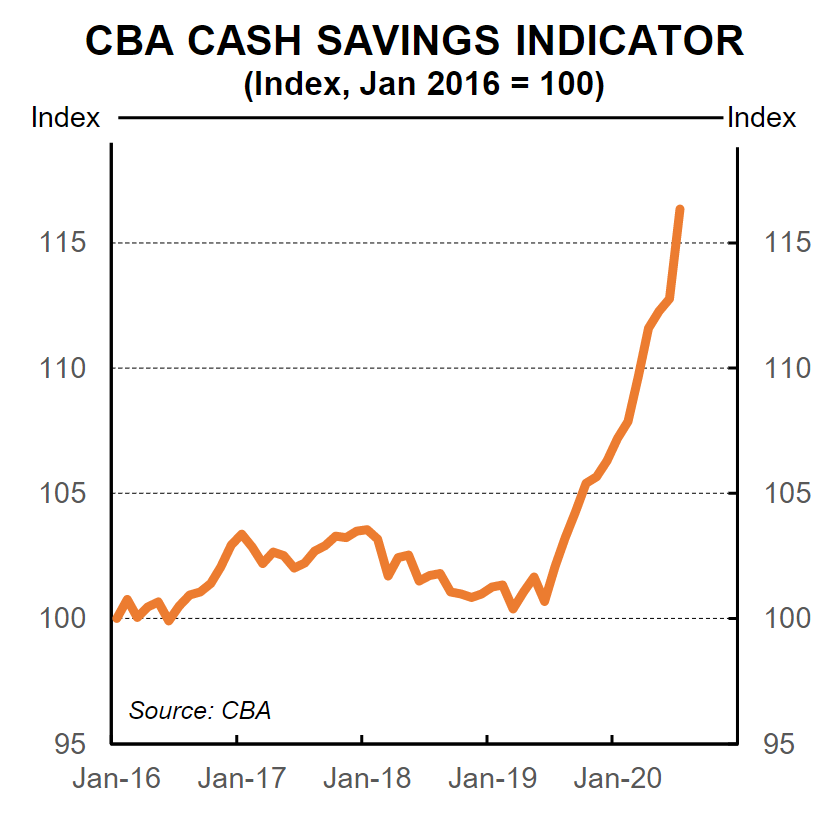

The average total savings balance per household has risen sharply as growth in income has been stronger than growth in spending.

The divide between income and production has further widened over Q3 20.

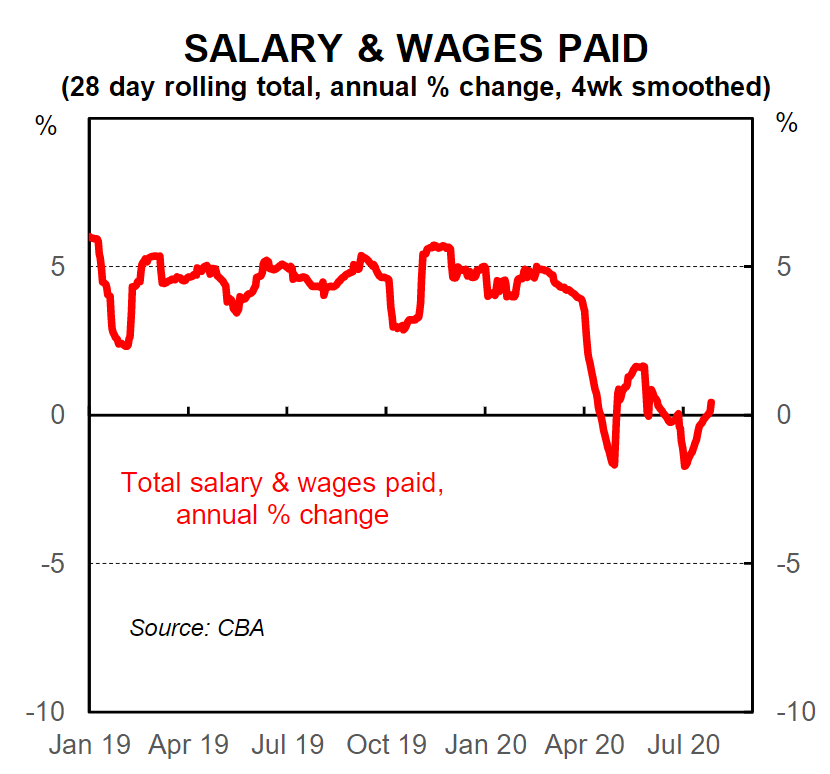

Growth in wages and salaries paid into CBA bank accounts has firmed a little over recent weeks. Overall the shock to wages and salaries from COVID-19 is around -5% (our wages and salaries data includes JobKeeper).

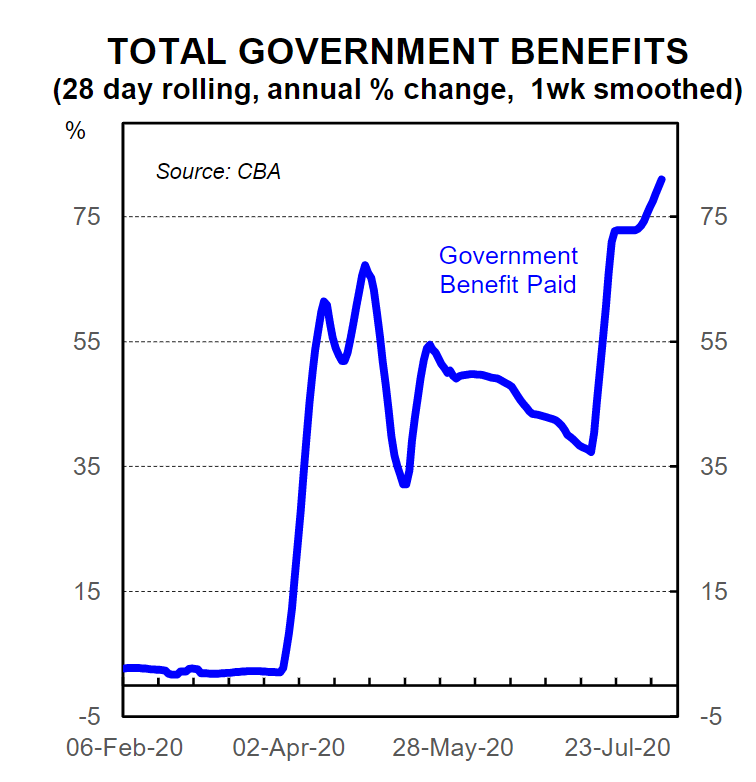

Government benefit payments have stepped up sharply due to the second tranche of $A750 stimulus payments and an increase in the number of people receiving JobSeeker. Government payments are up a whopping 85%/yr.

The number of people receiving JobSeeker has increased since early July across the board. NSW and Victoria have posted the sharpest increases amongst the larger states. Victoria is expected to see further increases due to the stage 4 lockdown.

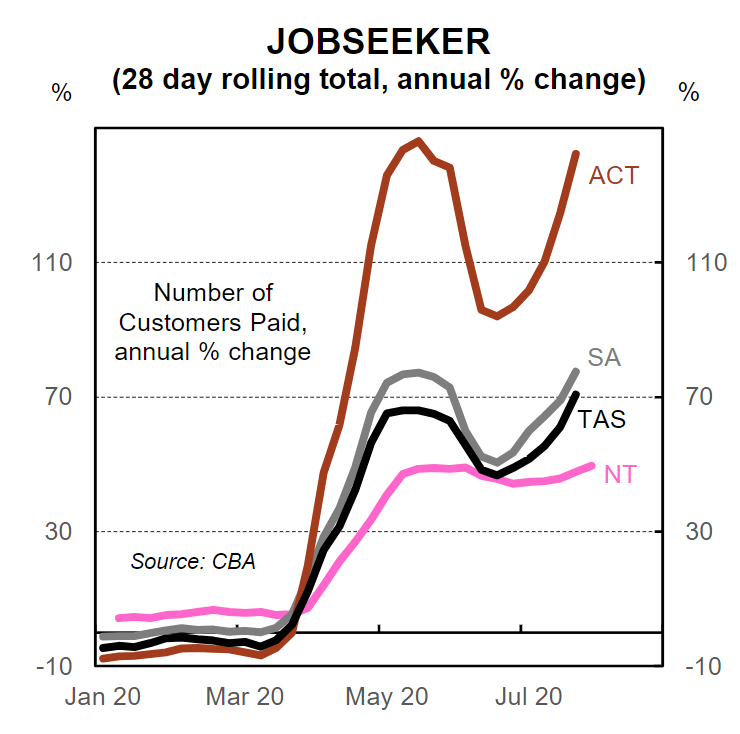

The number of people receiving JobSeeker has accelerated very quickly in the ACT over the past month. It is not clear to us why the number of people receiving JobSeeker has surged so quickly in the ACT.

The value of JobSeeker received has also lifted over the past month. The lift in the value of JobSeeker paid is much higher than the number of people receiving JobSeeker due the $A550 per fortnight ‘coronavirus supplement’. The ‘coronavirus supplement’ steps down to $A250 per fortnight in Q4 20.

The increase in government benefit payments is massive and has more than offset the decrease in wages and salaries paid. Our partial read on household income, which comprises wages & salaries and government payments, indicates household income surged over recent weeks(latest data 7August2020).

Growth in income has been significantly stronger than growth in spending. Savings have risen materially as a result. The CBA average total savings balance per household, including home lending related savings and transaction or savings accounts, was up 14%/yr at July2020.

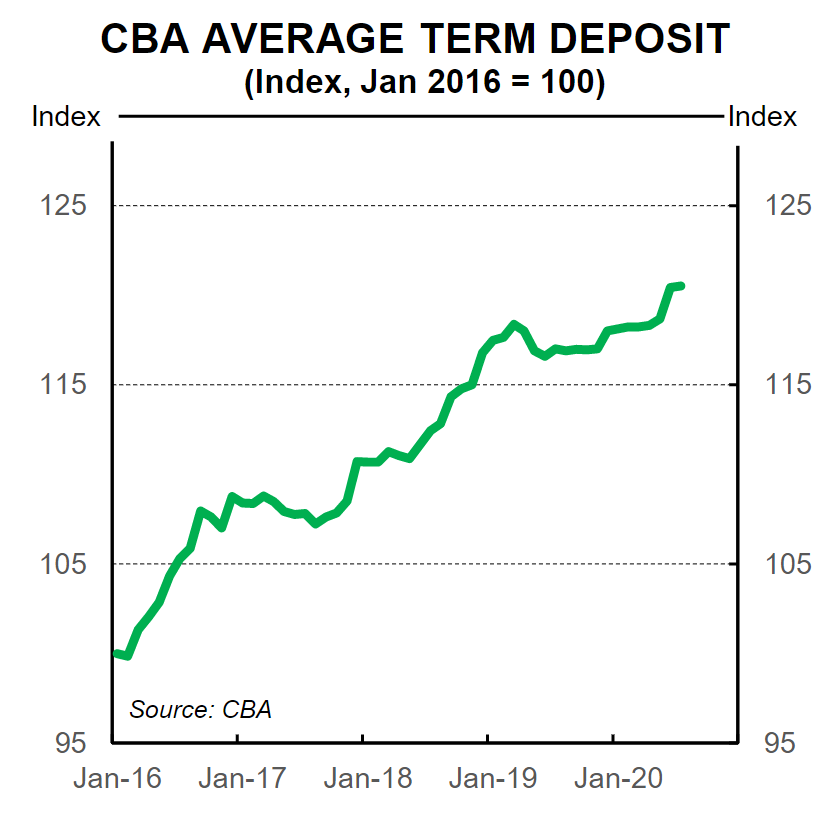

The CBA average term deposit balance per household has risen steadily over the past few years. The average term deposit was up by 3%/yr at July 2020 and is up by 7% over the past two years. A pronounced uptrend in the average term deposit has occurred despite interest rates coming down.

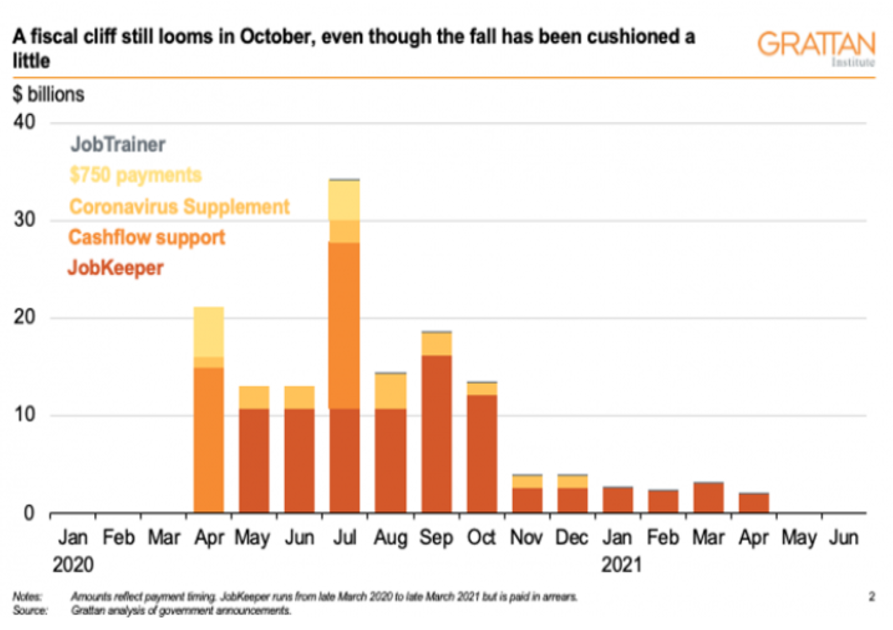

Amazing data. Household income will obviously fall once emergency income support is wound back from October:

JobKeeper reduced from $1500 to $1200 ($750 part-time); and

JobSeeker reduced from $1100 to $815.

Advertisement

The Grattan Institute estimates this tapering will reduce income support from $18 billion a month (10.7% of monthly GDP) to $3 billion a month (1.9% of GDP) for the six months beyond:

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.