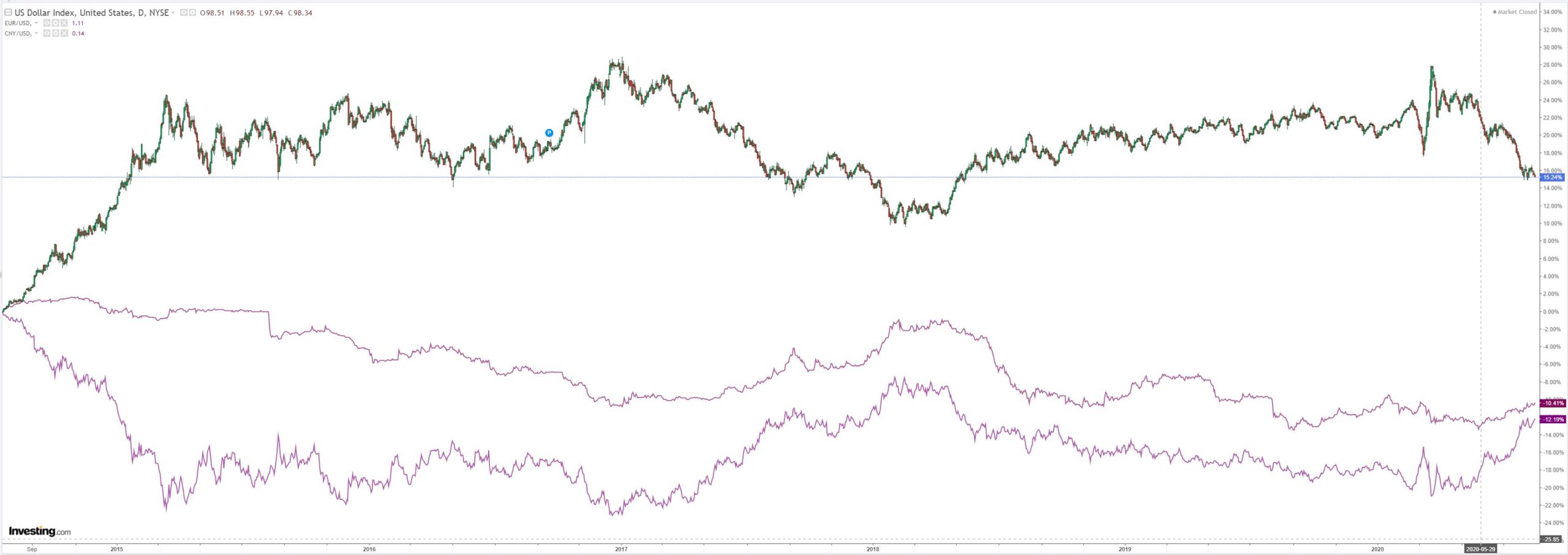

DXY is back to the lows as EUR heads back to the highs:

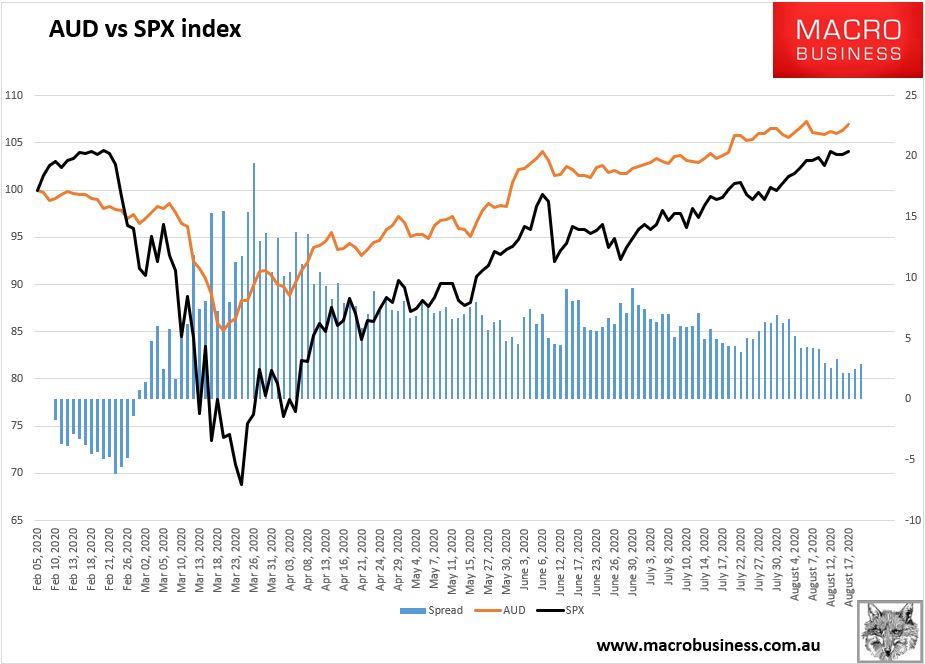

The Australian dollar took off:

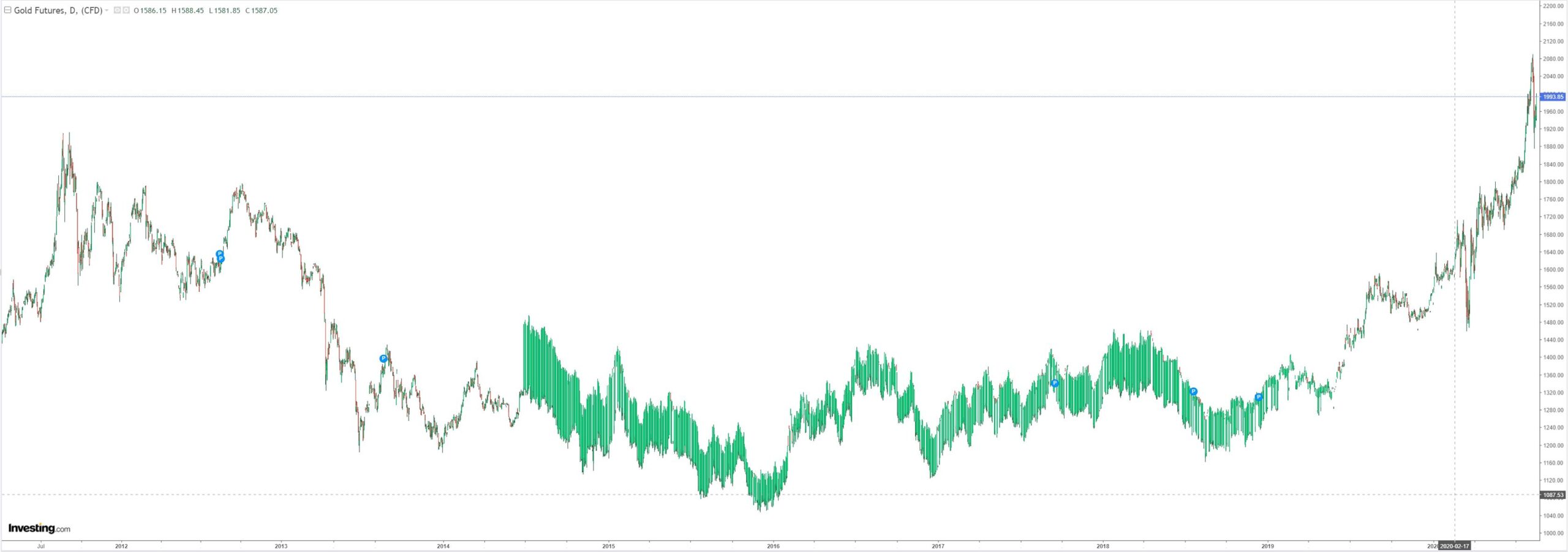

With gold:

Advertisement

Brent is paralysed while WTI catches up:

Metals are melting up:

Miners did better:

Advertisement

EM stocks are free and clear:

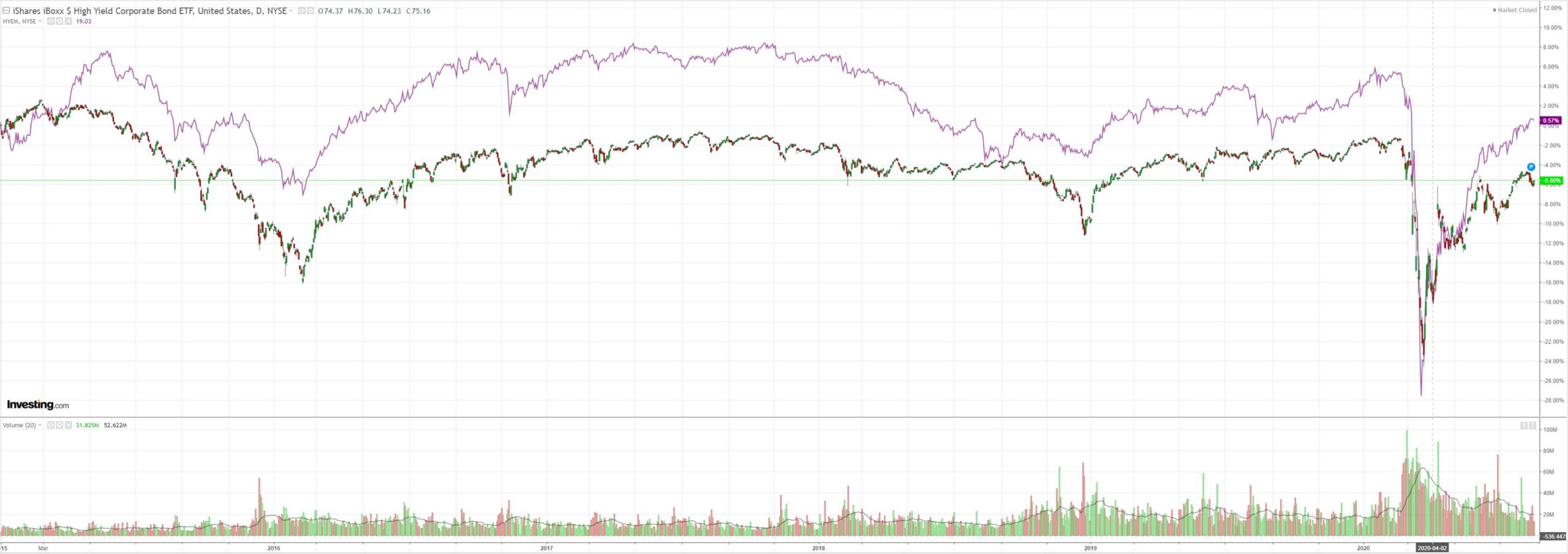

Junk firmed:

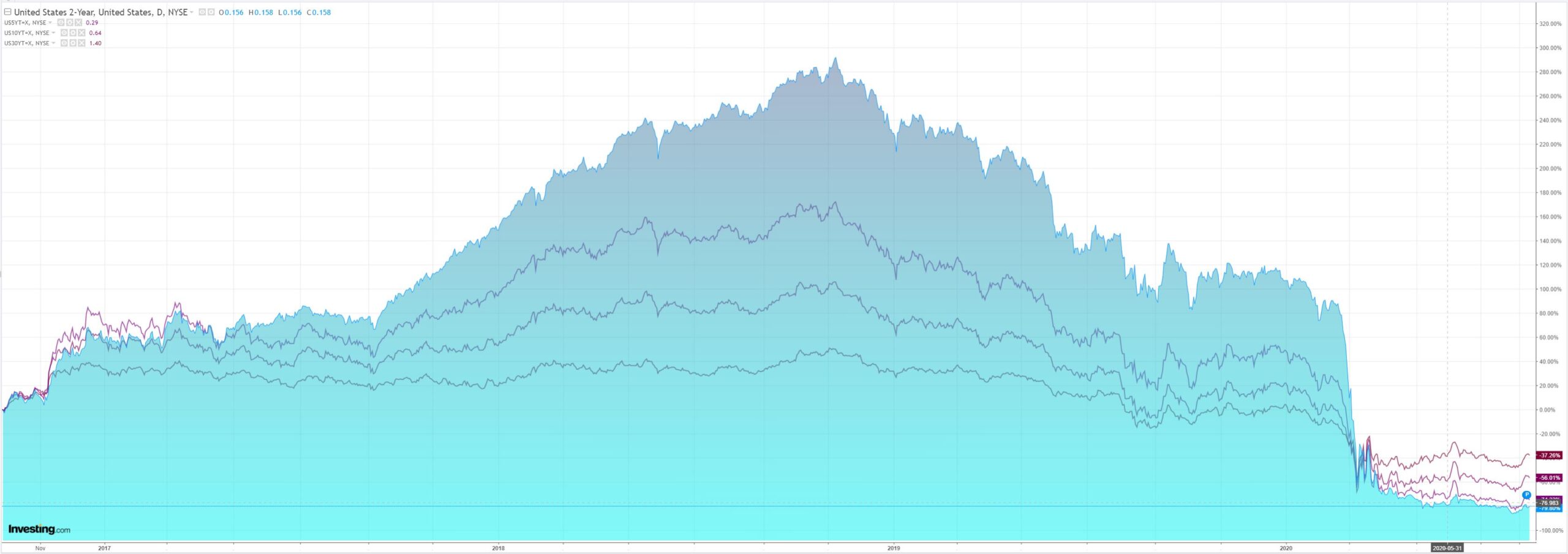

As US yields fell:

Advertisement

US stocks took off as European were crushed by the EUR (hello ASX):

The only chart that matters is still trending down in importance as the runaway AUD crushes any recovery at home:

Advertisement

Westpac has the wrap:

Event Wrap

US NAHB Aug. homebuilder confidence survey beat estimates with a retest of its all-time high at 78 (vs est. 74, prior 72), on record activity and low interest rates, with a notable rise in demand for single suburban homes. The subsequent demand for stud-lumber (prices have doubled since mid-April) is cited as a factor which may dampen activity.

Empire NY Fed Aug. manufacturing survey remained positive but disappointed with a reading of 3.7 (vs est. 15, prior 17.2). The “miss” was led by falling new orders (-1.7, prior +13.9). Extracting a minor positive was a rise in employees (+2.4, prior +0.4), although hours worked fell.

US Speaker Pelosi recalled the House from its recess to deal with funding the Postal Service. House Democrats plan to add $25 billion post office funding to legislation being voted on Saturday which would prohibit cutbacks in the service ahead of the November election, when millions of ballots are expected to be mailed. The mail service has become a flashpoint between the two parties ahead of the election.

Event Outlook

Australia: The RBA August meeting minutes will be released today, providing additional colour on the Board’s policy discussions.

US: Following June’s rapid 17.3% gain, momentum in housing starts is expected to moderate to a more sustainable pace, circa 3.7%. Growth in building permits is meanwhile expected to accelerate from 2.1% in June to 6.0% in July.

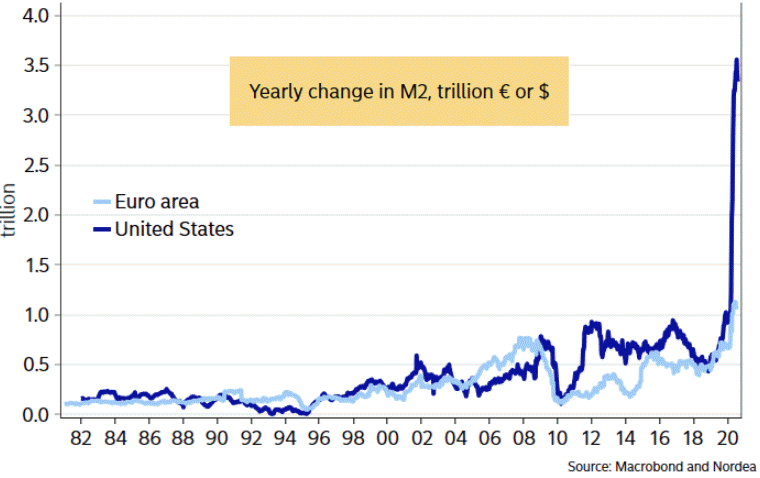

Not much to add beyond a reiteration of yesterday’s points. DXY is oversold but the Fed pump is outrageous:

Advertisement

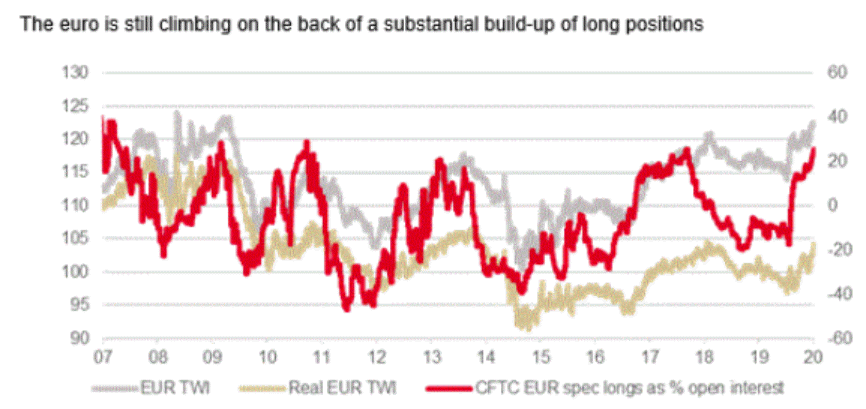

And EUR massively overbought, via SocGen:

The chart shows the trade-weighted euro in real and nominal terms, against CFTC positioning, showing net speculative longs as a percentage of open interest. It just gets more extreme. The ‘real;’ euro isn’t nearly as stretched as the nominal one suggests but the market is very long.

The Recovery Fund was a significant step in the right direction for Europe, and we have a very non-consensus view of Europa/US growth differentials that underpins a long-term bullish euro view. But as Covid spreads along the summer vacation hotspots in Europe, we still think this move has gone too far, much too fast.

Traditionally, this would make it more difficult for markets to persist with the rising EUR, falling DXY/commodities reflation trade. But given it’s all fakeflation anyway, and other markets have waltzed straight through similar unbalanced conditions, it might just keep running.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.