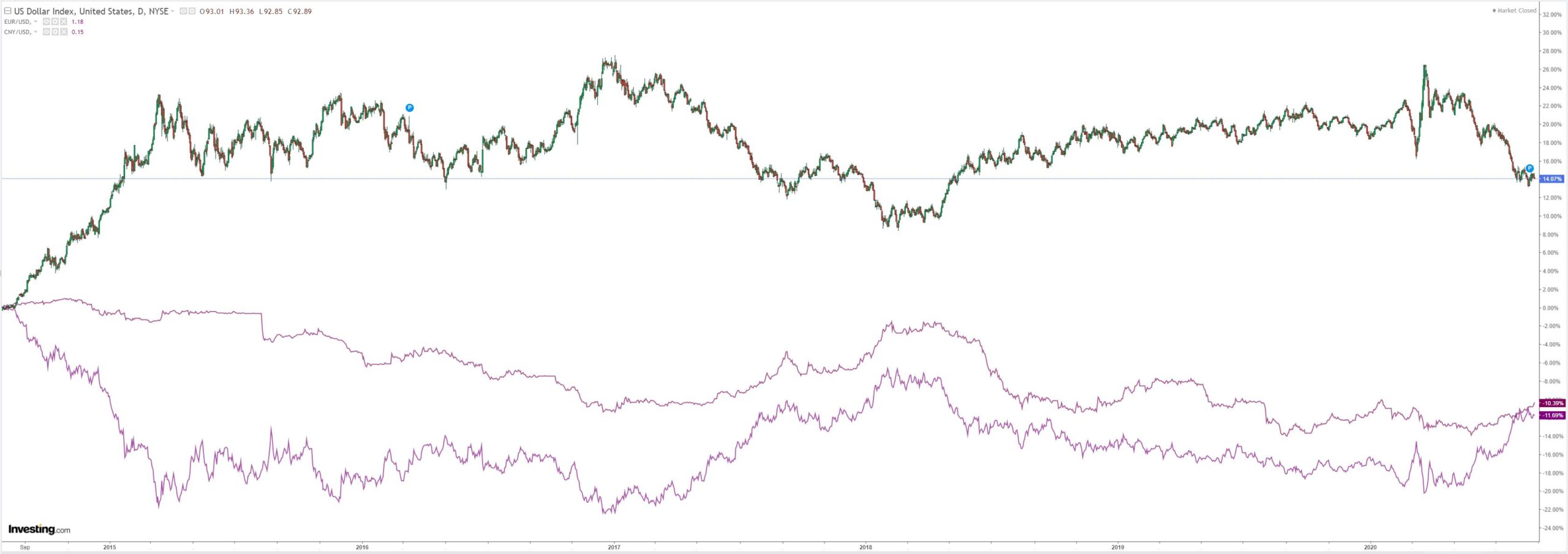

Did somebody leak tomorrow’s Powell speech? DXY was hit:

The Australian went bananas:

Gold jumped:

Oil was firm, hurricane assisted:

Metals were mixed:

Miners are underperforming in the circumstances:

EM stocks to the moon:

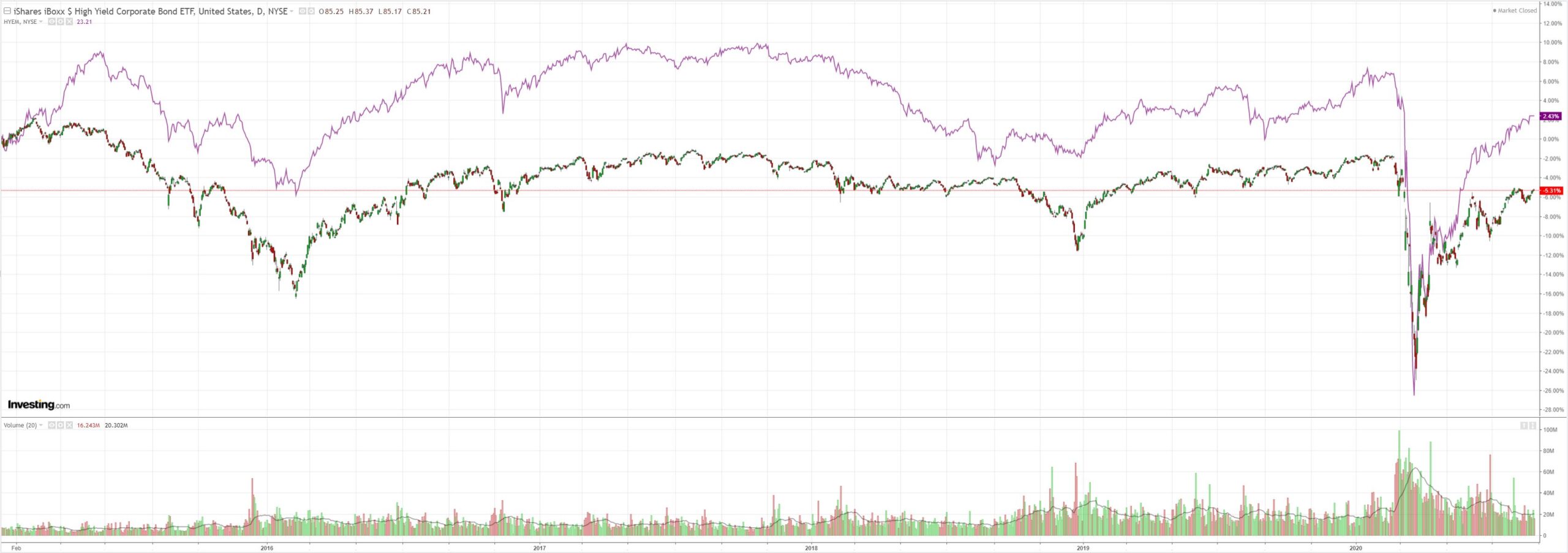

Junk bid:

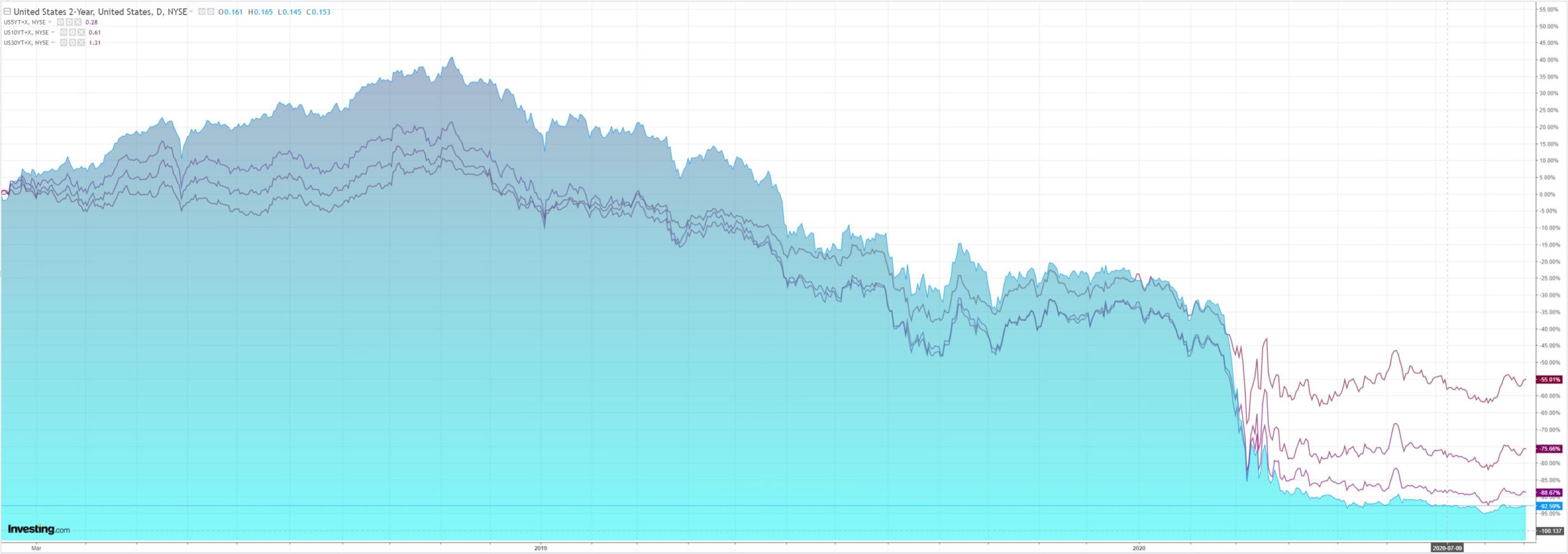

But US yields rose:

As US stocks go full melt-up:

Westpac has the data wrap:

Event Wrap

US durable goods orders rose +11.2% in July (est. +4.7%m.m, prior 7.7%m/m), although the ex-transport rise measure more subdued at +2.4%m/m (est. +2.0%m/m, prior revised to +4.0%m/m from initial +3.6%m/m). A sharper than expected lift in demand for vehicles boosted the headline figure.

Comments from the FOMC’s George and Barkin underscored the focus on disinflationary pressures, and uncertainty over the path of COVID-19 and the recovery, while avoiding being drawn into discussions on the review of Fed’s policy framework which is due to be the core of Powell’s keynote Symposium speech tomorrow.

Germany announced that it would extend wage support schemes into the end of the year at an estimated cost of EUR10bn, but also stated that it would tap EU funds (EUR15bn in grants) over the next two years in order to meet certain measures, such as exiting coal, without further blowing out their Budget deficit.

Event Outlook

Australia: Westpac and the market expect a sharp slump in equipment spending to drag private new capital expenditure down in Q2 (prior: -1.6%, market f/c: -8.2%, Westpac f/c: -8.2%). The third estimate for 2020/21 capex spending is also expected to show that plans have been ‘downgraded’ in response to the recession. Westpac predicts a capex expectation of $95bn, 16% below Estimate 3 a year ago. The latest report from the ABS of business impacts of COVID will reflect the combined effects of lower business revenue and the Melbourne lockdown’s hit to activity.

Korea: The Bank of Korea is expected to keep their policy rate on hold for the time being at 0.5%.

China: The pick-up in industrial profits to June was driven by government-led infrastructure investment. Momentum is broadening across the economy (prior: 11.5%yr).

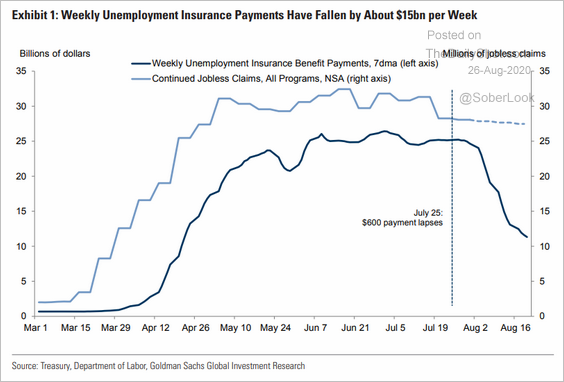

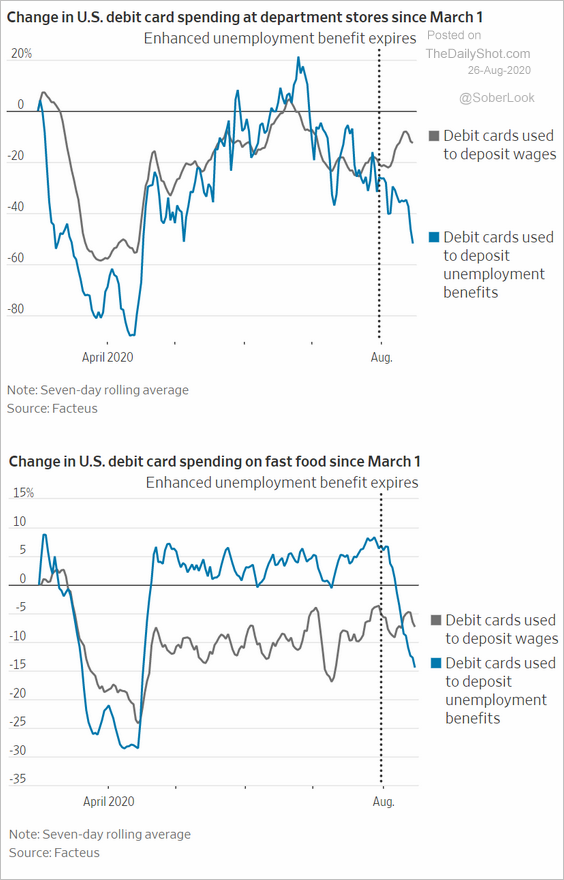

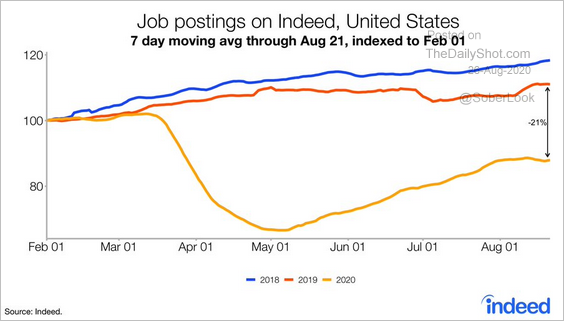

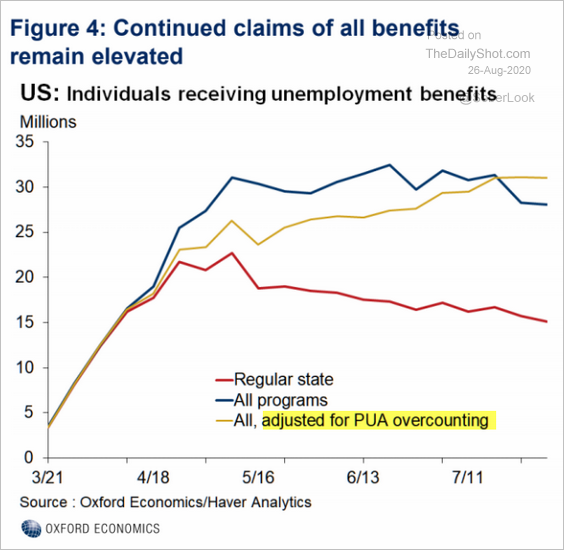

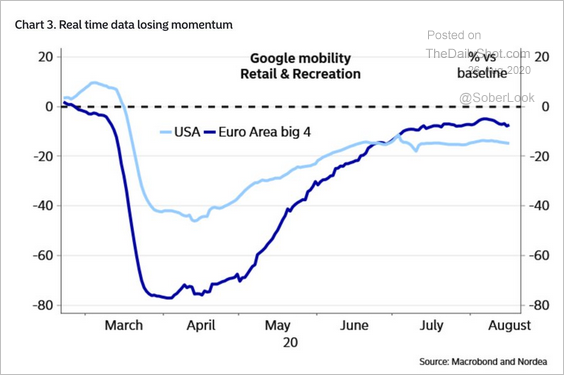

The good news driving stocks is that the underlying economy is sagging again as a steepening fiscal cliff takes its toll:

Europe remains better so there is still pressure for a stronger EUR bid:

But:

The US recovery is a mess of virus-smashed activity driving asset prices wild given bad news is good. But the crazed risk-on bid is still knocking up against very unbalanced market positions as well.

The Australian dollar is a cork riding a rising storm of greed and fear capable of anything.