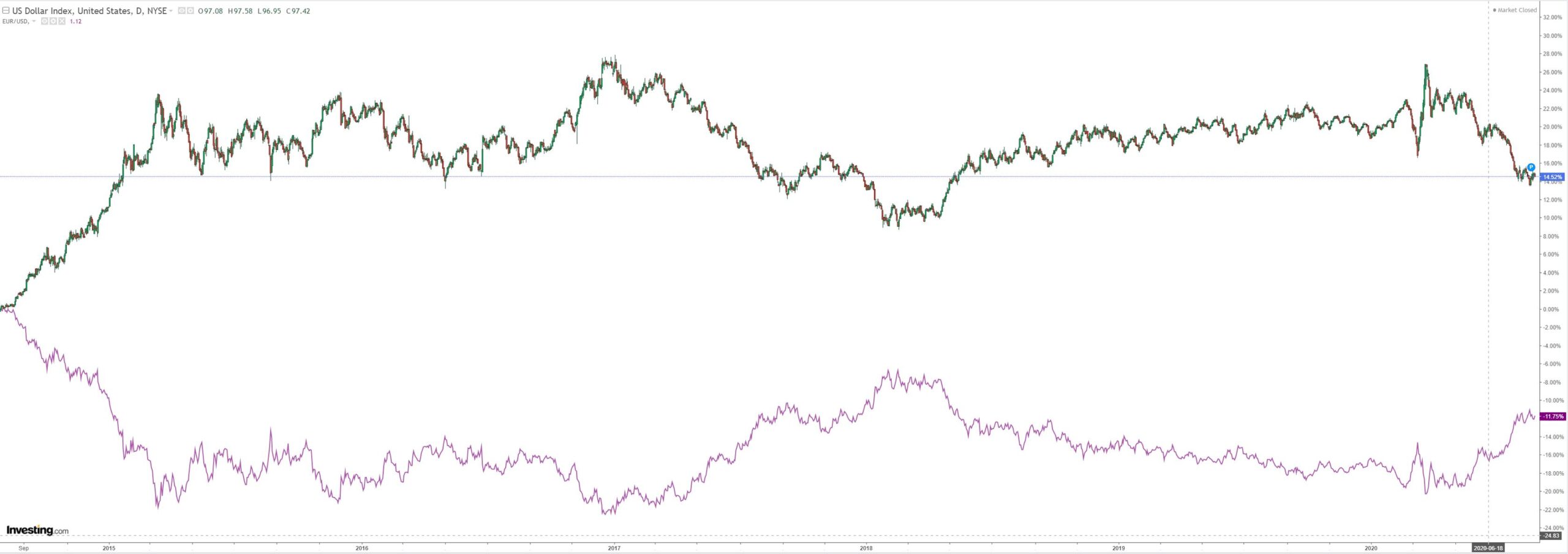

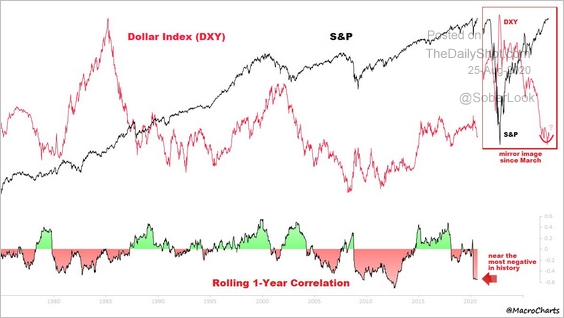

DXY was down again last night EUR rallied:

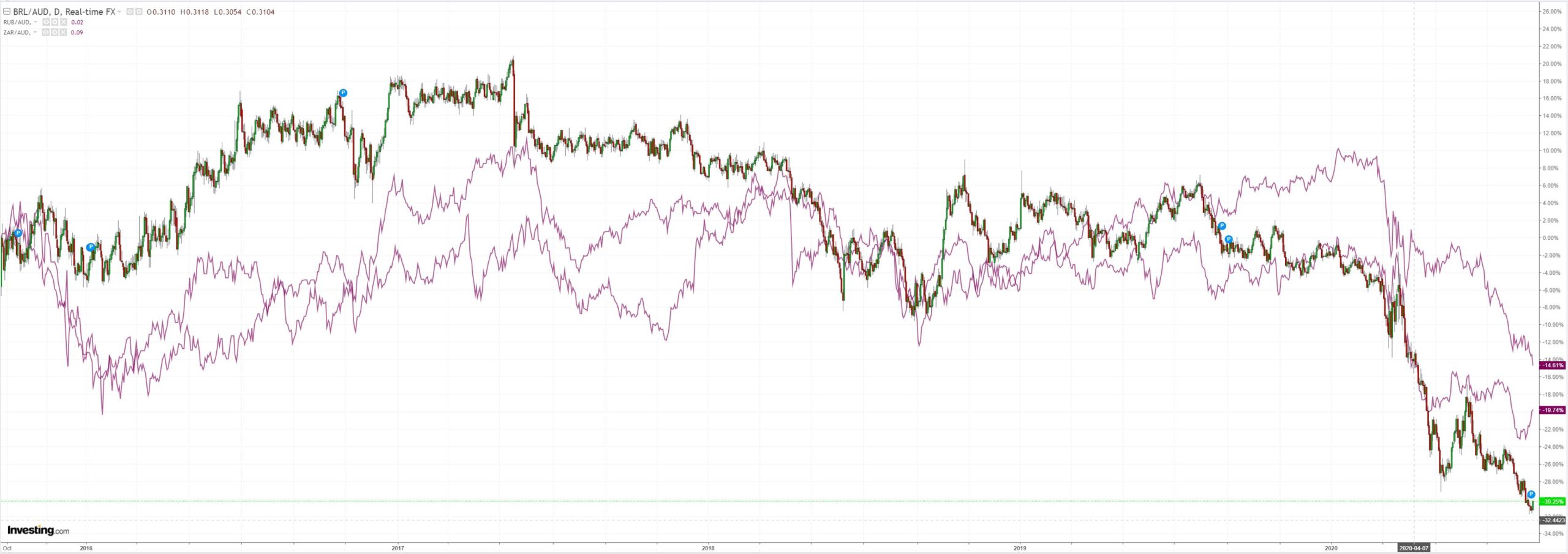

The Australian dollar followed the script of firming:

Though EMs were stronger:

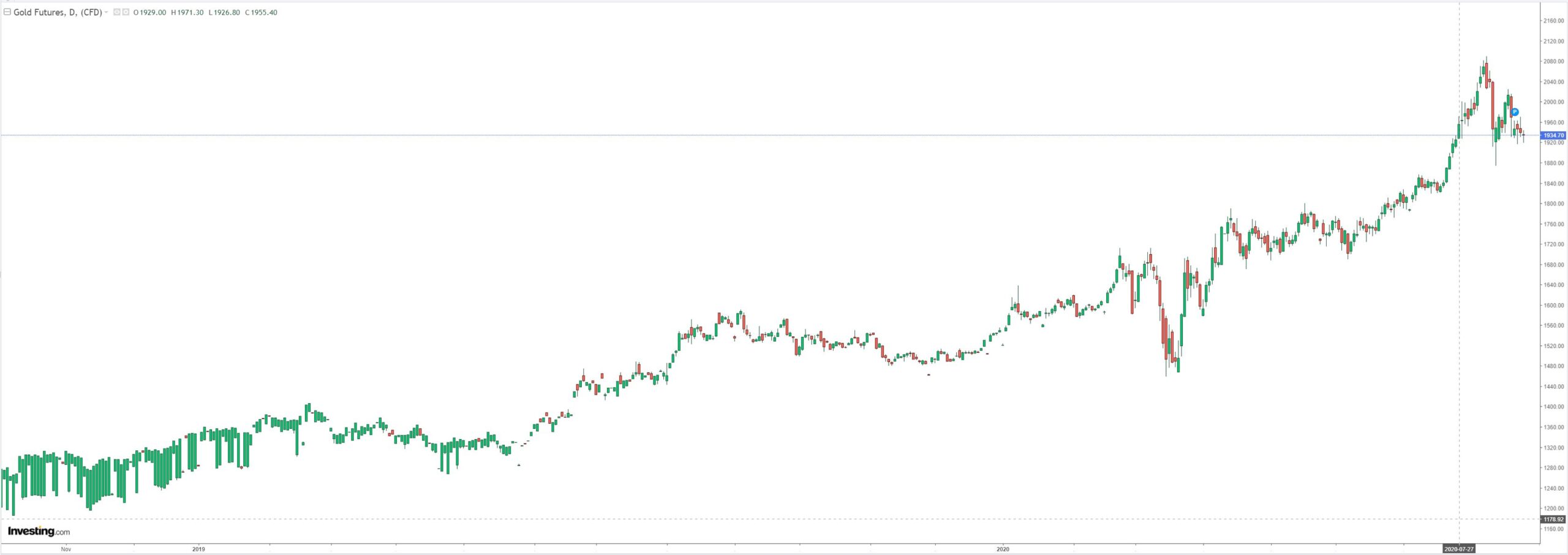

Gold is still shaking out weak hands:

Oil caught a bid:

Metals too:

But not miners as iron ore deflates:

EM stocks were up:

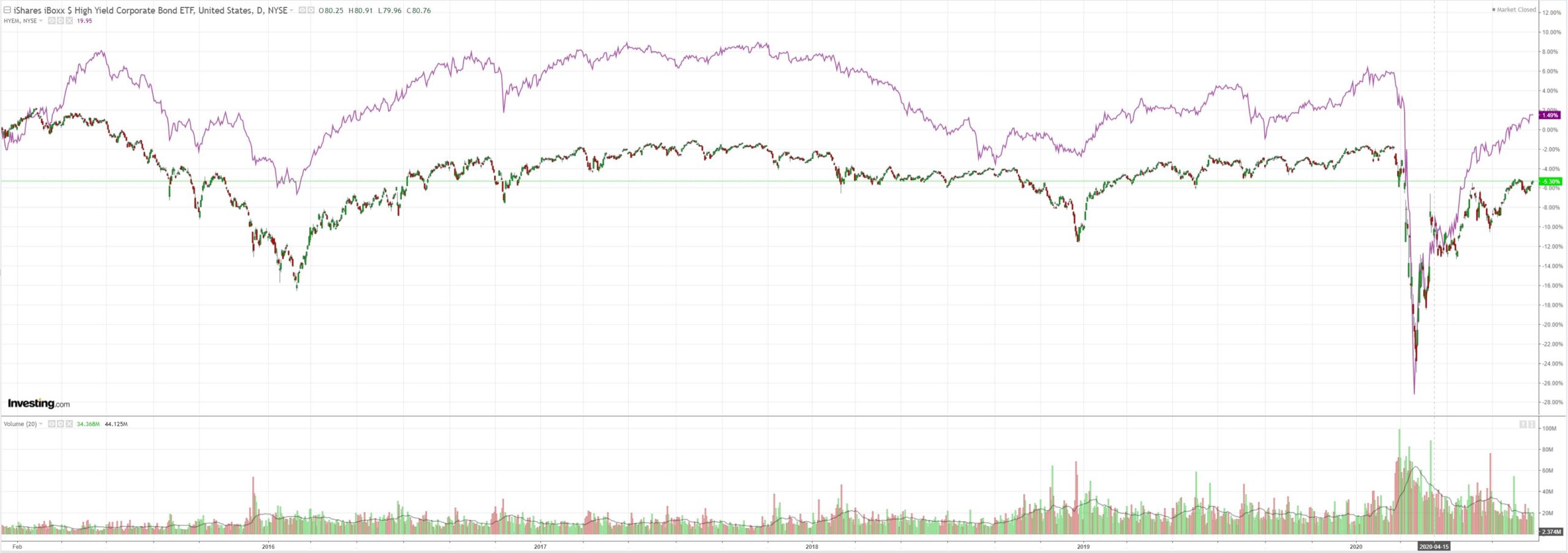

Junk too:

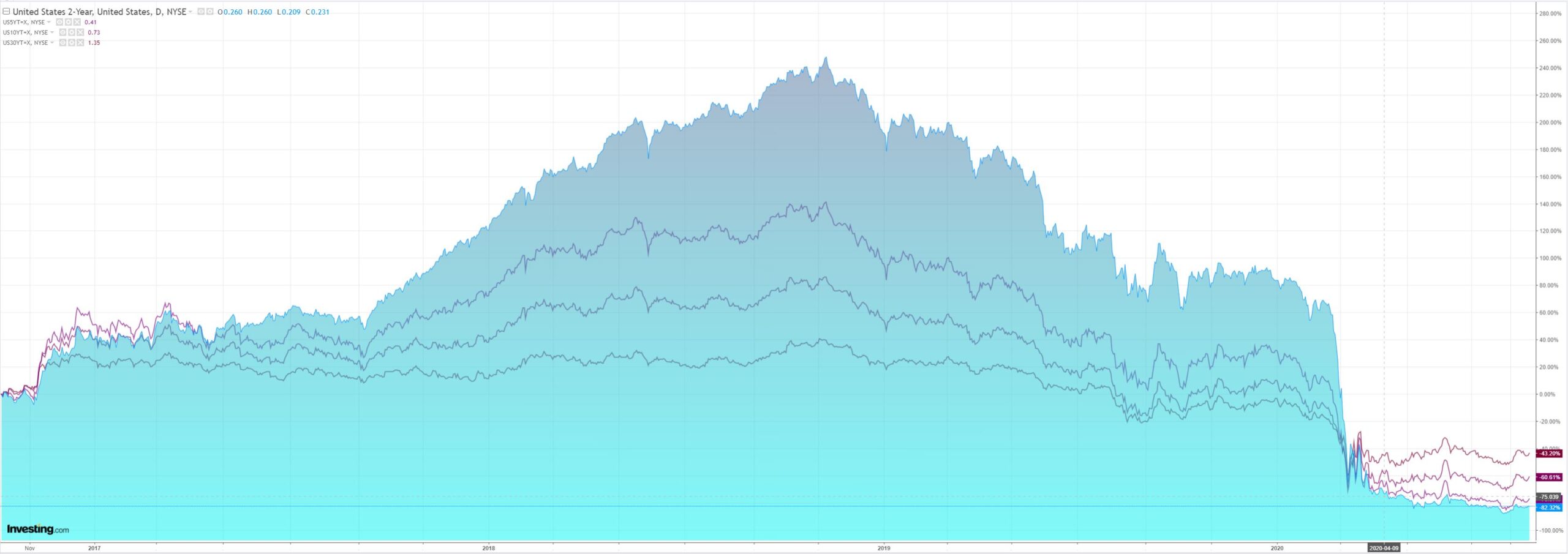

Despite US yields copping it:

US stocks only go up. European never do. We follow the latter:

Westpac has the wrap:

Event Wrap

US home sales rose +13.9% in July to 901k (est. 790k, prior revised to 791k from 776k) – the highest level since late 2006. Average prices rose to a mid-2019 high at US$391k. The August Richmond Fed manufacturing survey index beat expectations at 18 (est. unchanged at 10), most key components higher, with gains in employment and work week and a sharp drop in the availability of skilled workers. The August Conference Board consumer confidence survey index slumped to 84.8 (est. 93.0) from 91.7 (revised from 92.6) in July, as concerns about the outlook and financial well-being exceeded the uplift in spending. The expectations component fell to 85 (prior 88.9, revised from 91.5) and current conditions fell to 84.2 (prior revised to 95.9 from initial 94.2). CoreLogic/Case-Shiller house prices were unchanged in June (vs. est. +0.1%, prior -0.03%).

Germany’s August IFO survey was solid and close to market estimates. The climate index of 92.6 beat estimates of 92.1 (prior 90.4). Expectations rose to 97.5 (est. 98.0, prior 96.7) and current assessment rose to 87.9 (est. 86.2, prior 84.5). IFO’s President said the survey showed that the “recovery is more or less on track” even if not back to normal. The final reading of Germany’s 2Q GDP was slightly less weak than initial updates. Activity fell 9.7%q/q (revised from -10.1%q/q), capital investment fell -7.9%q/q (from 12.2%q/q), but private consumption was weaker at-10.9%q/q (from -9.8%q/q).

UK August CBI retail activity reflected the recent shedding of retail workers with the reported sales index falling to -6 (prior +4, est. +6), and a warning of worse outcomes to come, despite some improvement in expectations for the next quarter.

Event Outlook

Australia: Westpac and the market expect construction work in Q2 to exhibit broad-based weakness across the private sector, respectively forecasting declines of -3.4% and -7.0% after Q1’s -1.0%.

New Zealand: The trade balance is expected to have returned to surplus in July as import demand remained weak (prior: $426m, market f/c: $293m, Westpac f/c: $280m).

Singapore: Industrial production is set to rebound after an unexpected slump in May. The market expects a 3.7% gain in July following June’s 0.2%.

US: Durable goods orders rose in June on increased demand for transportation equipment. Momentum is set to persist in July (prior: 7.6%, market f/c: 4.5%).

Some pent-up demand coming through in US housing but consumers are still under the pump.

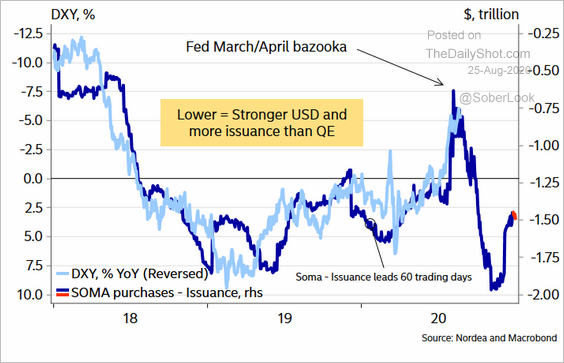

DXY and EUR are still extended. US stocks need the dollar to fall:

But the Fed pump may no longer be strong enough to deliver it:

And one of either US stocks will likely fall or yields rise:

Into 2021, I still AUD higher as the Fed keeps the pedal to the metal. But markets are still very unbalanced and working it off plus US political risk is rising so the near term remains much more volatile.

More from the Fed Thursday at Jackson Hole.