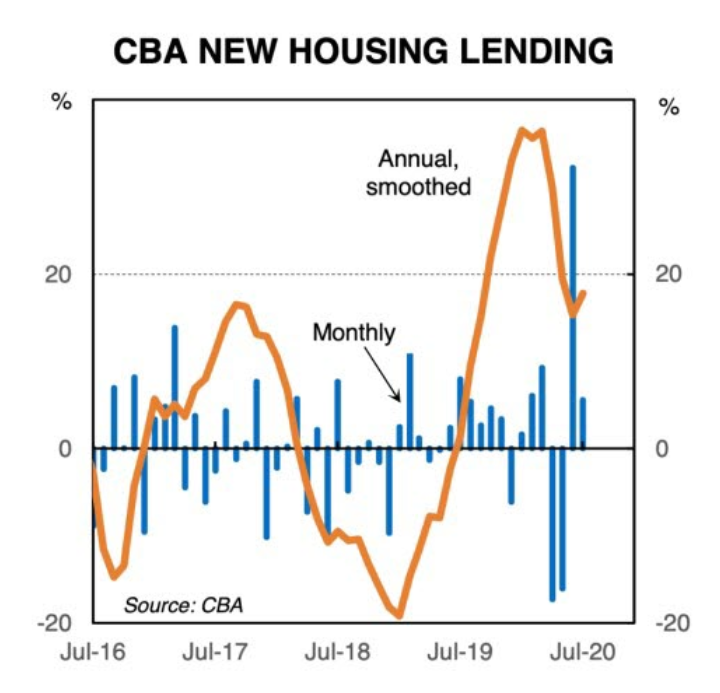

That’s the view of Crikey’s Jason Murphy, who believes that Australian housing “like a cockroach… appears capable of withstanding anything”. This is based on internal mortgage lending data from the CBA showing that mortgage demand has rebounded strongly:

Apparently amid the mayhem of death and economic destruction wrought by 2020, housing lending is continuing apace.

In fact, as the next graph shows, despite a dip in April and May, new lending is still almost 20% higher than last year.

Australia’s love for home ownership apparently continues to burn fiercely.

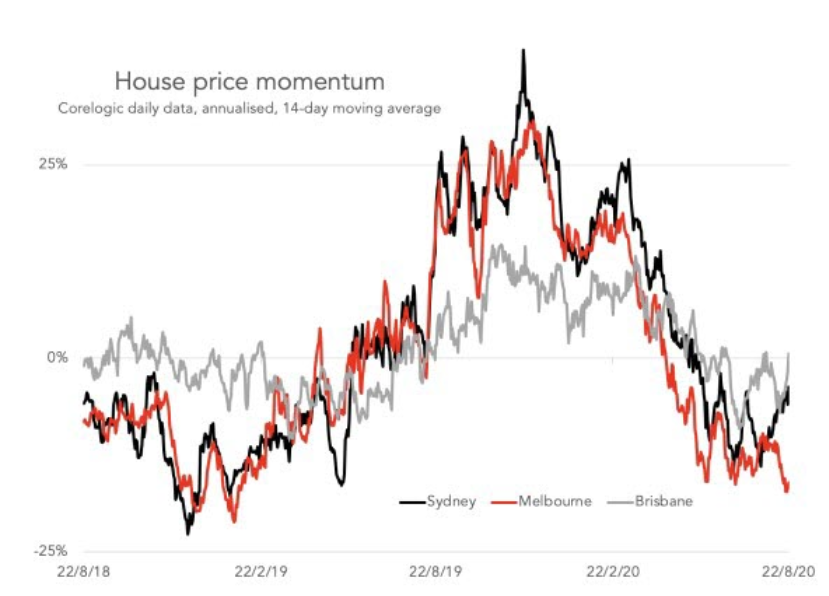

As the next graph shows, house price movements remain quite negative in Victoria. But in NSW and Queensland they appear to be clawing their way back up to positive territory. The effect of the lockdowns is wearing off…

Whether you seek to assign credit or blame for this miraculous stability in the housing market, you must turn to one place. The Reserve Bank of Australia. Its interest rate cuts have been the balm the housing market wanted. By slashing the official interest rate to just 0.25%, fixed mortgage rates have fallen to as low as 2.3%…

These low rates mean borrowers can service far higher loans. And so they are borrowing more. Average loan size is also up on last year, according to CBA data.

With the RBA pledging to leave rates at low levels for years to come, you have to wonder if big new loans will be enough to compensate for the many factors that would otherwise be pushing the housing market down.

The CBA’s lending data is certainly eyebrow raising. But it must also be noted that CBA’s mortgage book is growing faster than the system, so there’s some market share impact at play.

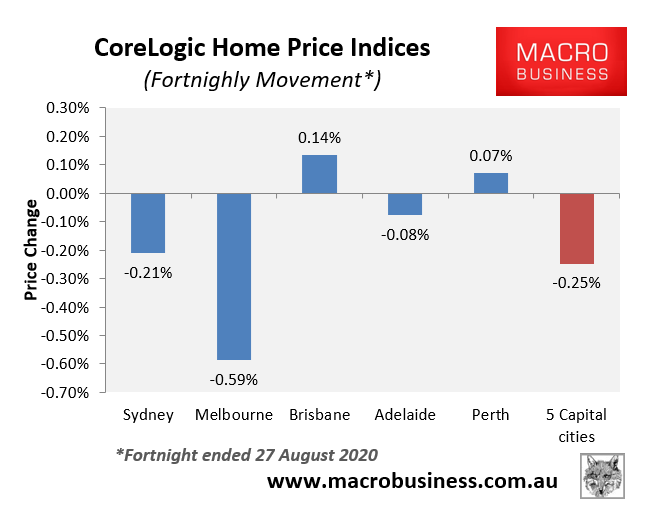

Moreover, Jason Murphy’s claim that NSW and Queensland “appear to be clawing their way back up to positive territory” is only half right. The next chart shows that in the fortnight to 27 August, Sydney dwelling values fell by 0.21%, but rose by 0.14% in Brisbane:

Advertisement

Let me outline the alternative “bear” case for the Australian property market.

Let’s begin with mortgage rates, which are already at rock bottom and have little room further to fall. Thus, the 30-year tailwind of falling mortgage rates will soon be over for Australian property.

Advertisement

This means that future price growth will need to come from rising household incomes. On this front, the news is poor given Australia is facing a prolonged period of high unemployment and anaemic income growth.

Indeed, this income growth will take a sharp hit in October when emergency income support – JobKeeper and the JobSeeker supplement – are reduced as follows:

JobKeeper reduced from $1500 to $1200.

JobSeeker reduced from $1100 to $815.

Advertisement

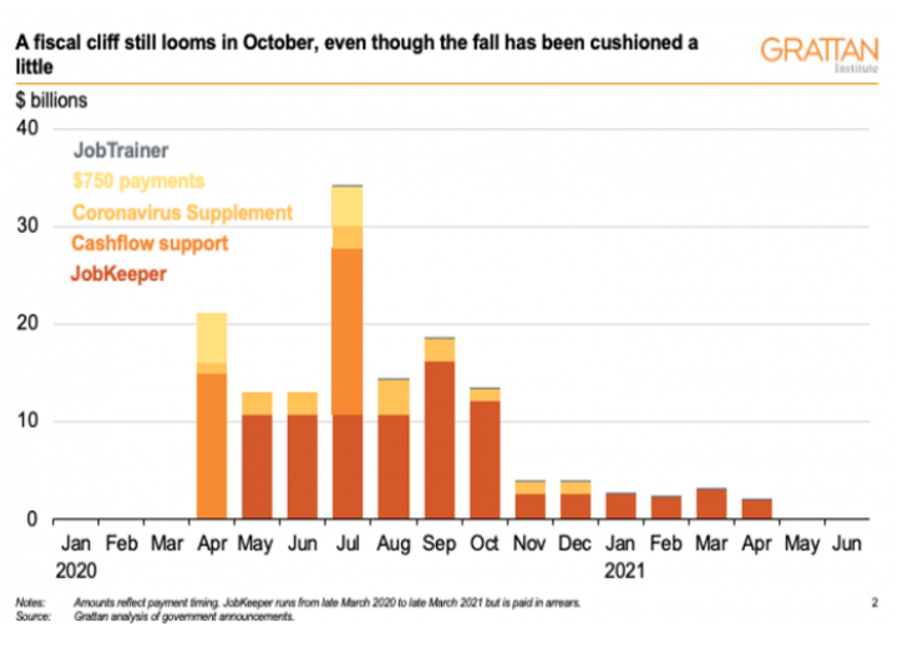

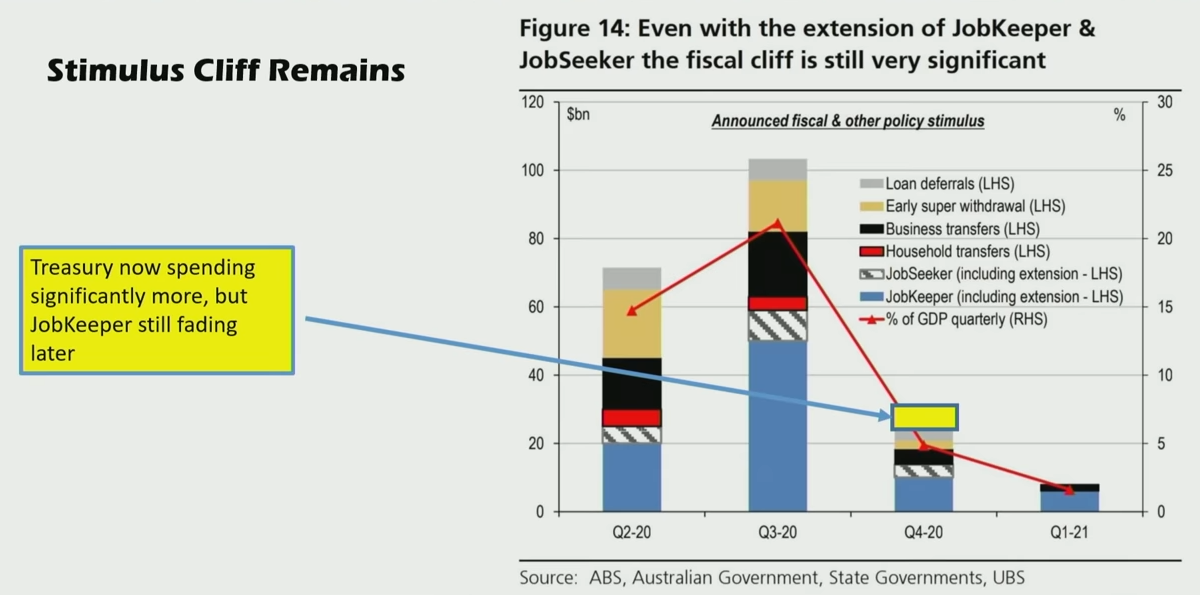

The Grattan Institute estimates that this tapering will reduce income support from $18 billion a month (10.7% of monthly GDP) to $3 billion a month (1.9% of GDP) for the six months beyond:

UBS has come up with similar estimates for the collapse in household disposable income:

Advertisement

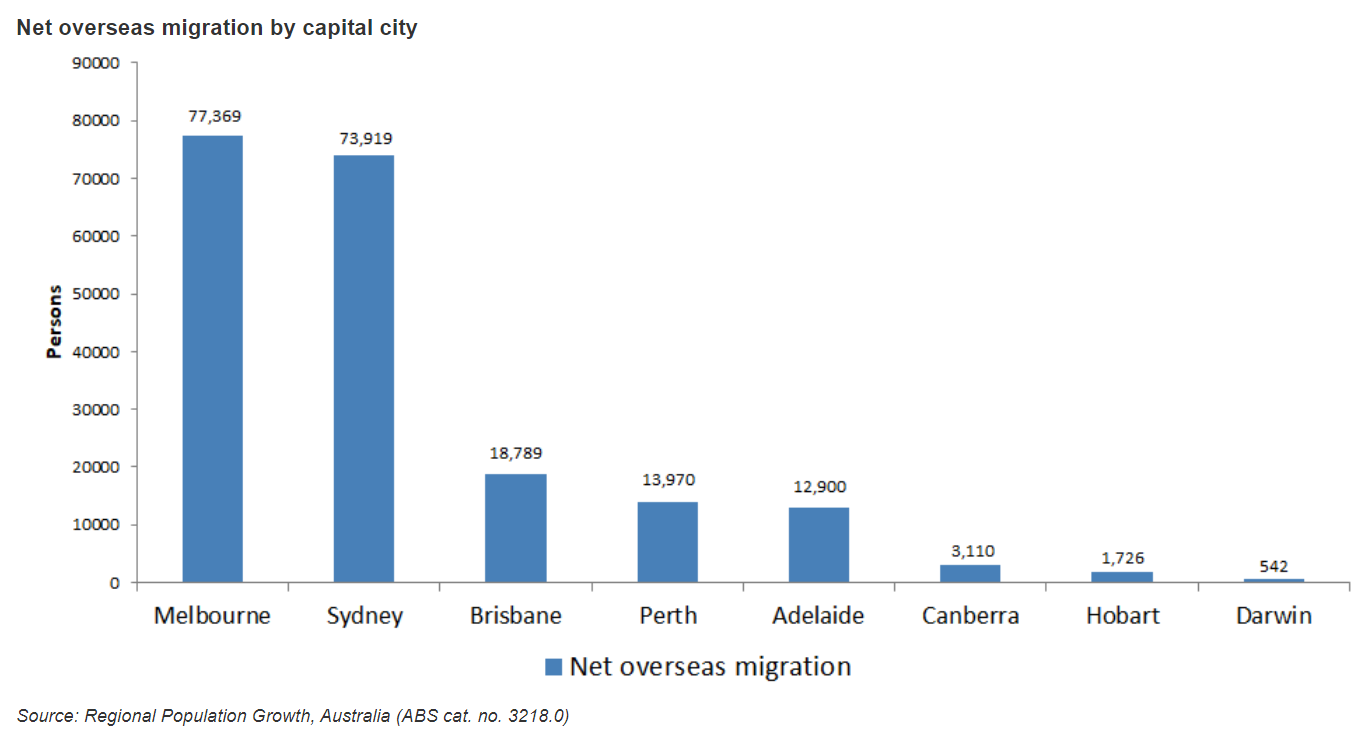

Next, immigration is projected to collapse by 85% over 2020-21 and then remain lower in the decade ahead. This will hammer Melbourne and Sydney property especially hard given they are the most migrant dependent, as illustrated below:

Advertisement

According to CBA head of Australian economics, Gareth Aird:

Net overseas migration (NOM) and in turn population growth will decline significantly over the short run due to the COVID-19 pandemic. The Australian Government expects NOM to have fallen by ~30% in 2019/20 and to fall by ~85% in 2021/22. This means that there is an expected shortfall of around ~310k in NOM over the next 18 months compared to original estimates..

Australia’s population grew by ~380k per annum over the two years prior to the pandemic. That meant underlying demand for new housing had been running at ~185k dwellings per year (i.e. based on the assumption of 2.1 persons per dwelling and the demolition rate). But with population growth set to drop to ~180k in 2020/21 the underlying demand for new housing plummets to 95k.

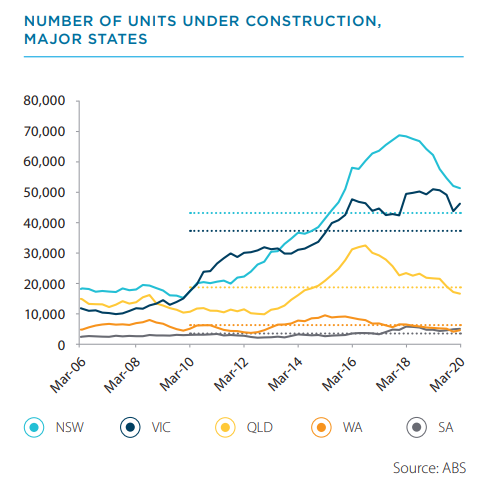

While demand (immigration) has collapsed, these two jurisdictions are still furiously adding supply, with apartment construction rates above the decade average as at March 2020:

Advertisement

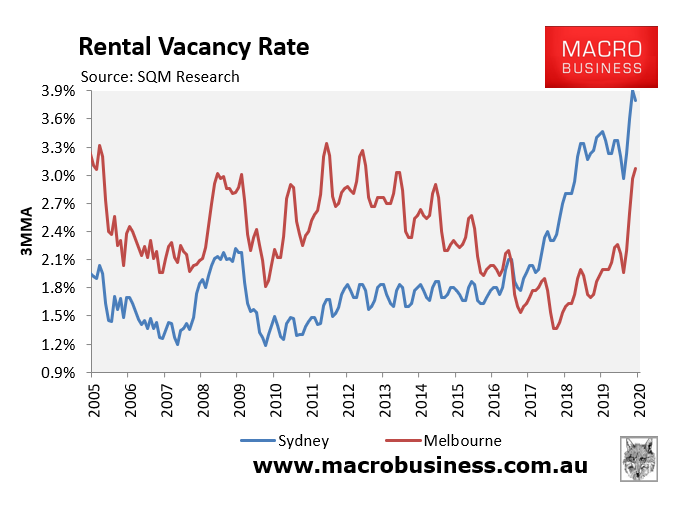

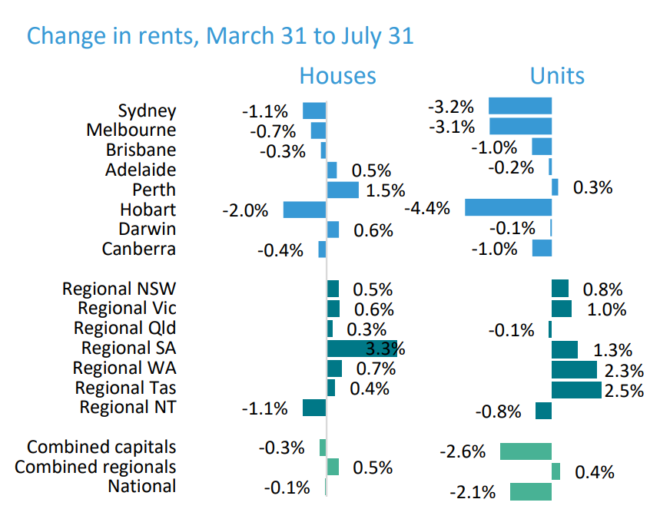

The upshot is that rental vacancy rates have ballooned and rents are falling in both cities:

Any objective analysis of the facts would conclude that the Australian housing market faces significant downside risks. These are being masked by unprecedented emergency income support, mortgage repayment holidays, and early superannuation release, all of which are scheduled to end within six months.

Advertisement

The key risk is that Australia’s army of loss-making landlords, wedged between falling values and rents, will be forced to sell in significant numbers, causing a feedback loop of falling property prices.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.