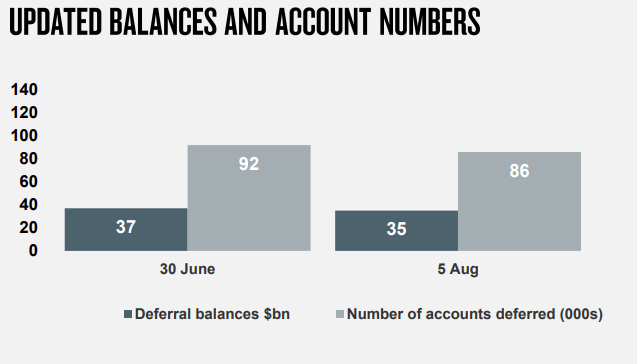

NABs third quarter results were released on Friday, which revealed that 86,000 mortgages have been deferred totalling some $35 billion:

According to NAB:

- 7.4% of people have an LVR over 80% of which 4.5% don’t have LMI.

- 2.6% of people have an LVR over 90% of which 1.5% don’t have LMI.

Compared with the total mortgage book, deferral customers had lower average savings in transaction accounts and higher average use of credit cards prior to the pandemic:

- ~30% of mortgage deferral customers have no redraw / offsets available.

- ~70% of mortgage deferral customers are <3 months ahead on repayments.

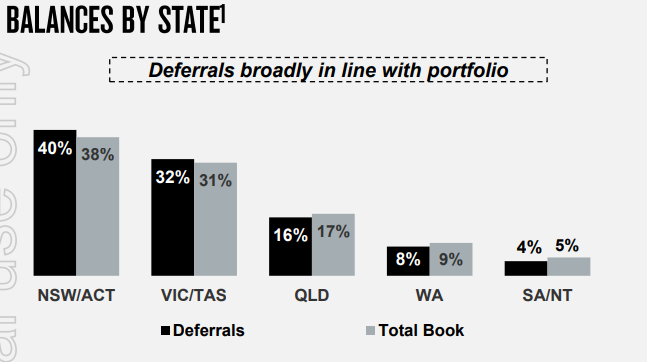

NSW has around 40% of mortgage deferrals and VIC has 32%:

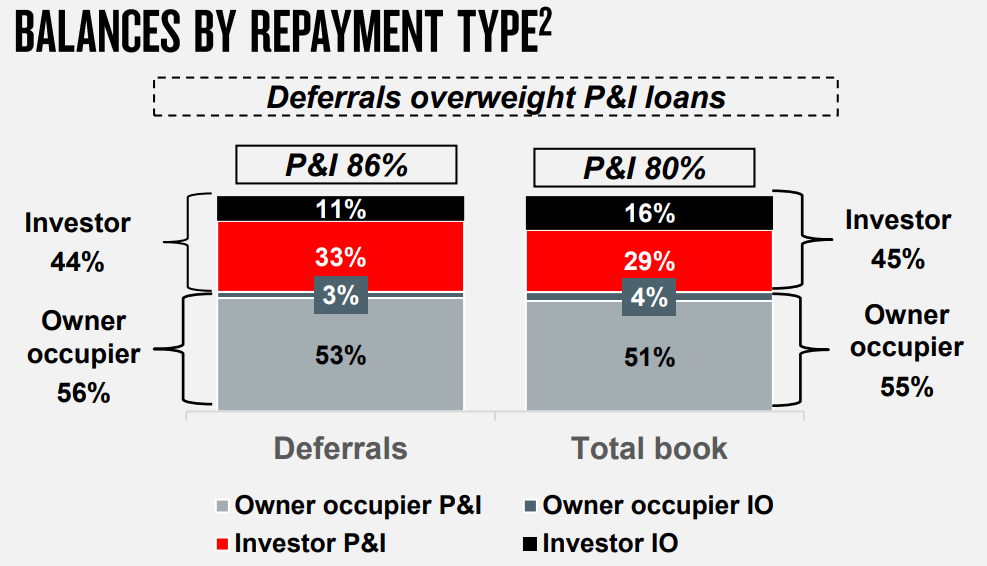

Finally, around 44% of deferrals are investors:

NAB CEO, Ross McEwan, told a media conference on Friday that he is not confident that the mortgage deferrers will easily recover:

“It’s very clear that there will be a large number of people that will need support of some shape or form at the end of this and that could be through restructuring of loans, be that business or home loans, going onto interest only for a period of time but there are a number of things that we can do to be helpful here”.

CBA CEO, Matt Comyn, made similar observations last week, noting that 12% of its 135,000 mortgage deferrers will not be able to go back to business as usual:

Commonwealth Bank says it considers 16,200 of its 135,000 home loan customers with paused repayments are at “higher risk” of defaulting and will urge them to shift onto interest-only terms when the coronavirus grace period ends in October…

“Deferrals have provided obviously significant support and flexibility for customers,” he said. “Clearly the test is going to be how effectively we can make the orderly transition away from repayment deferrals.”

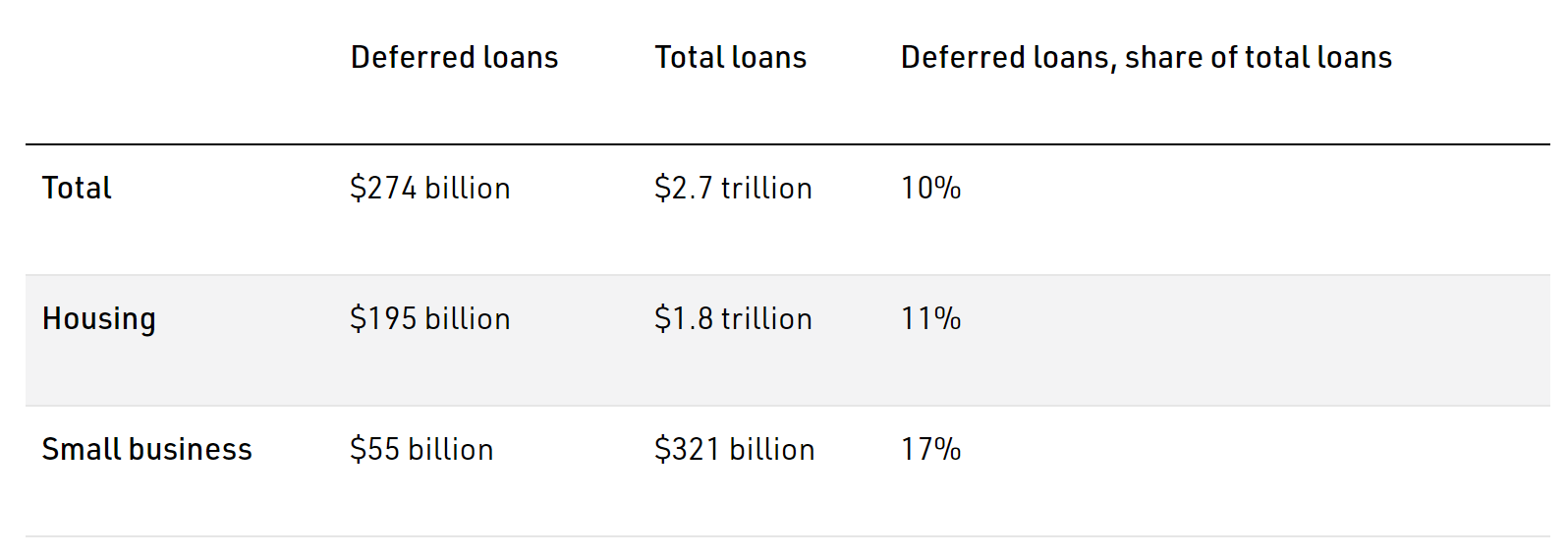

According to APRA, a total of around 500,000 mortgages have been deferred valued at $195 billion, comprising some 11% of Australia’s total mortgage book:

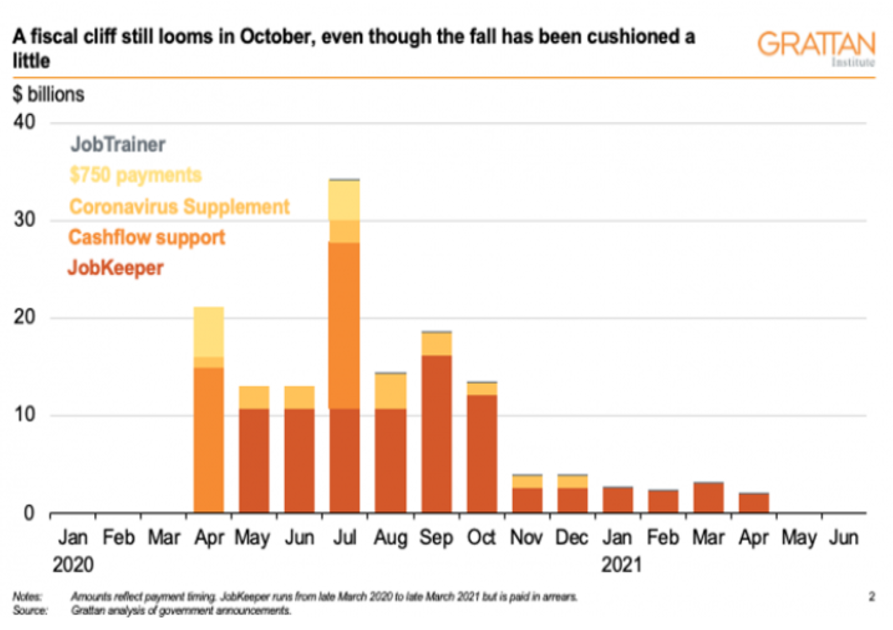

The Australian economy and property market are currently existing in an artificial bubble, propped up by mortgage repayment holidays and emergency income support.

Both of these will taper down from October, with the Grattan Institute estimating that income support alone will be reduced from $18 billion a month (10.7% of monthly GDP) to $3 billion a month (1.9% of GDP) for the six months beyond:

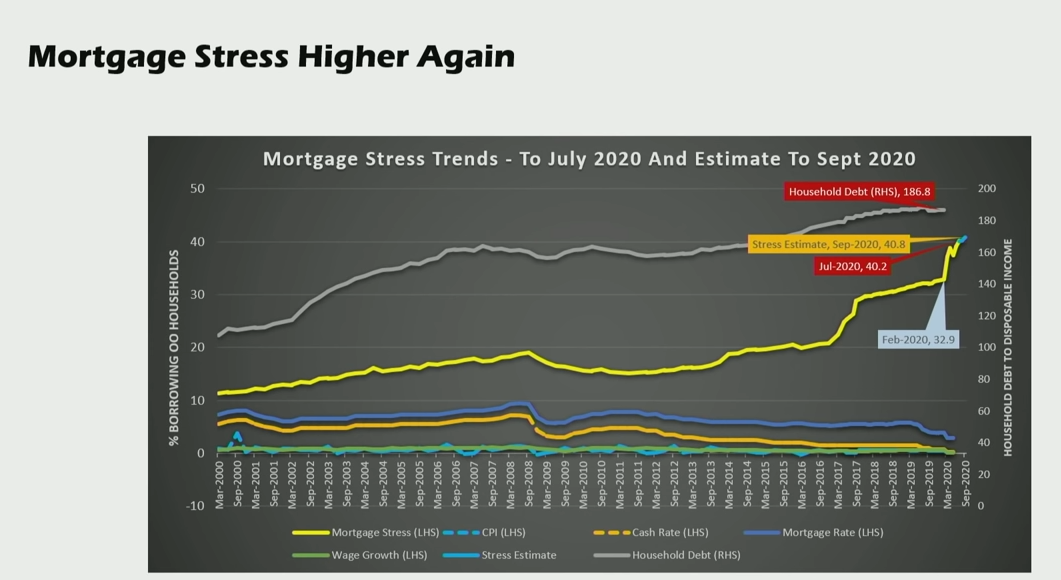

Even with these supports in play, “more than 1.5 million households [are] in mortgage stress, rental stress is up, and property investor stress is up”, according to Digital Finance Analytics:

Thus, the Australian property market, banks and mortgage holders must eventually face the music. And when that happens, there will likely be significant selling pressure that pushes property prices lower.