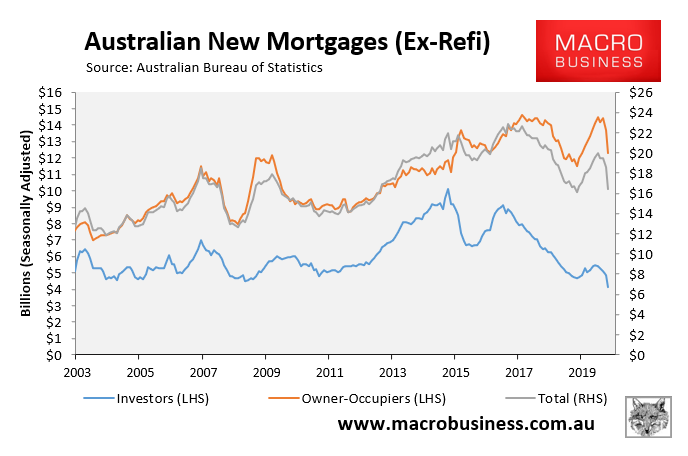

As reported yesterday, the value of new mortgages issued collapsed by nearly 12% May, driven by a sharp 16% fall in investor mortgages:

This was the sharpest monthly decline in new mortgage commitments in the 18 year history of the series.

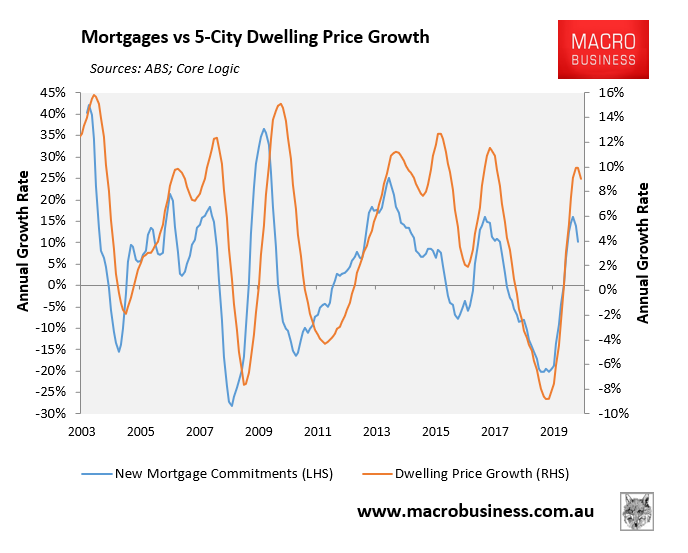

Given historical experience, the decline in new mortgage commitments points to Australian dwelling values declining:

Advertisement

As you can see, there is a very strong correlation between mortgage growth and dwelling value growth, with mortgages typically leading prices.

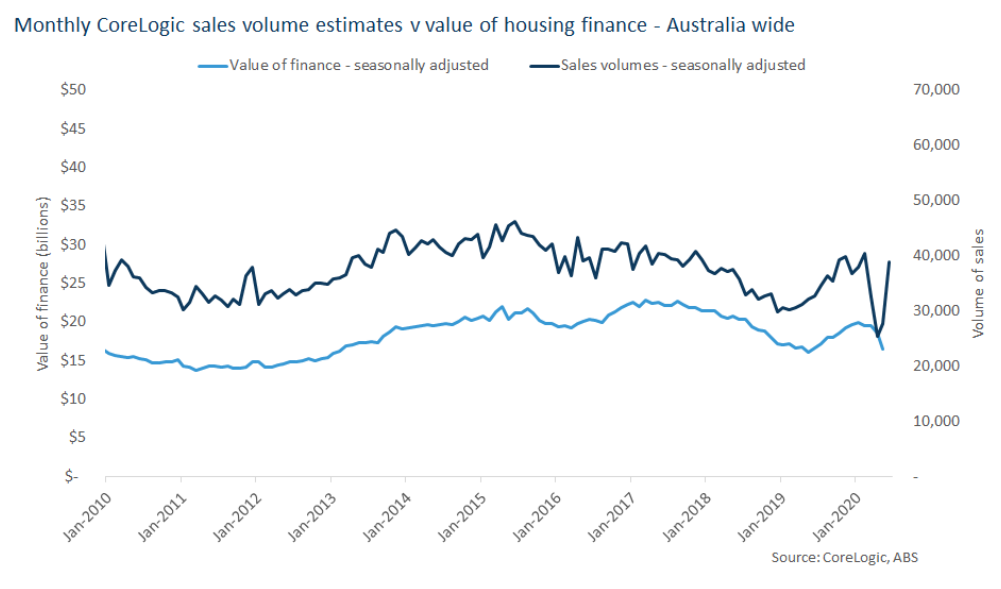

However, CoreLogic’s head of research, Eliza Owen, has released data suggesting that mortgage growth would likely have picked-up in June, given the strong rebound in property sales:

Advertisement

The chart below shows the monthly value of new finance for housing from the ABS, against the number of property transactions estimated by CoreLogic. The two metrics have moved quite closely together historically. This suggests that when more money is lent for the purpose of buying property, we will typically also see a rise in the number of transactions.

While this is intuitive, there is something curious about the relationship. In some instances, shifts in the direction of sales volume estimates produced by CoreLogic are a month ahead of changes in the direction of new housing finance. The correlation coefficient between the two series is slightly strengthened when the sales volumes are lagged by one month.

The lagging of finance data has been particularly evident in the dramatic disruption that has played out amid COVID-19. CoreLogic sales volumes started rebounding over May, while housing finance saw a record decline.

This could be because of the way sales volumes and finance commitments are dated. CoreLogic sales volumes generally date sales from the sale’s contract date. But housing finance commitments, according to the ABS, are only counted when the following three criteria are met:

1) A home loan application has been approved;

2) a loan contract or letter of offer has been issued to a borrower; and

3) the borrower has accepted the offer.

This means that a housing finance commitment could occur in the month after property is purchased…

Understanding this detail of the data could help us understand whether housing finance numbers will have fallen further in June, or if they would start to recover.

Based on the fact that CoreLogic sales estimates rebounded 29.5% over June, housing finance values may actually have bottomed out in May…

The number of advertised listings provides another signal for higher sales. While the number of new capital city listings has increased by more than 40% since early May, while the total listings count has reduced by close to 3% over the same period. This implies a new listings to sales ratio of around 1.3. In other words, more homes are being sold than what is being added to the market.

Despite signs of rising transaction activity and finance volumes recently, significant headwinds lie ahead for sales activity. With the re-introduction of the stage 3 lockdown across Melbourne, the impact on sales volumes is two-fold. There is the physical limitation on selling homes that come with social distancing, as well as a more general fall in consumer confidence. The ANZ-Roy Morgan Consumer Confidence index has declined in the past two weeks of measurement. Declines in consumer sentiment are associated with falls in property tractions.

This means that while finance volumes could bottom out in May for the 2019-20 financial year, the potential for another significant fall exists while social distancing policies are required.

This analysis makes sense. Almost all properties are purchased using finance. Therefore, a pick-up in sales volumes should equate to a lift in mortgage commitments.

However, as noted by Eliza Owen, the anticipated rebound in mortgages is likely to be short-lived, given the reintroduced hard lockdown in Melbourne, growing COVID-19 community transmission in Sydney, and shattered consumer confidence.

Advertisement

As such, mortgage commitments look set to experience another downturn.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.