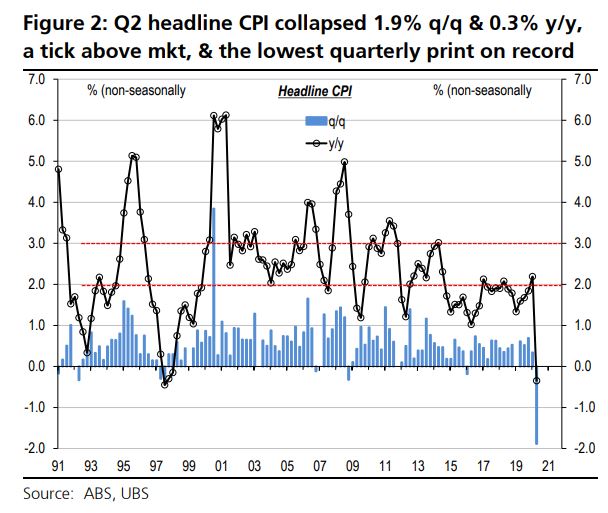

He pretty much only has one task. Keeping inflation in the 2-3% band. Yet he has failed utterly for four straight years. On headline inflation:

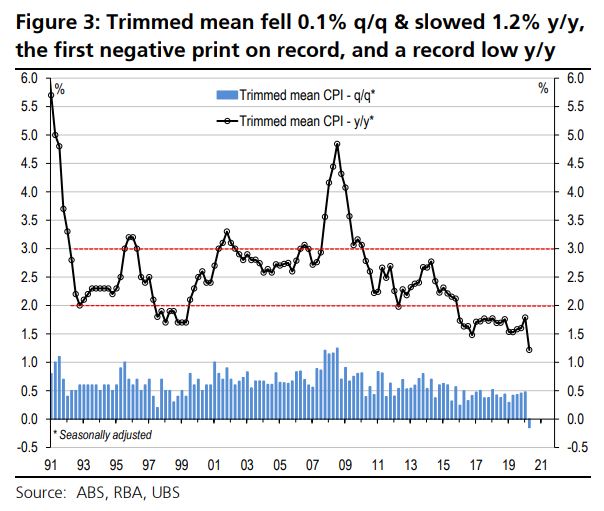

Trimmed mean:

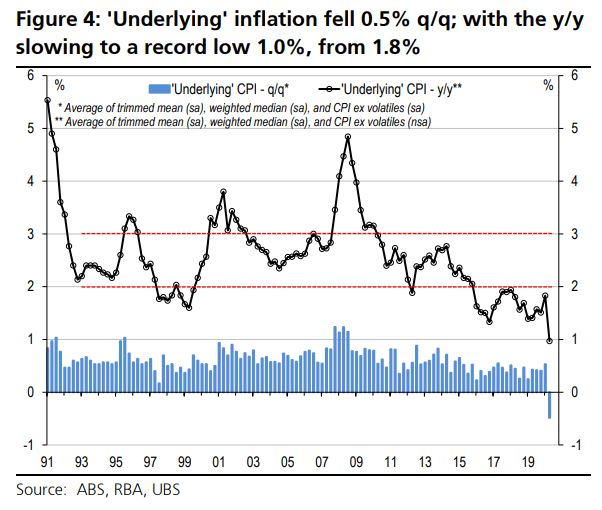

Core:

Advertisement

He pretty much only has one task. Keeping inflation in the 2-3% band. Yet he has failed utterly for four straight years. On headline inflation:

Trimmed mean:

Core:

The full text of this article is available to MacroBusiness subscribers