Currently, the US economy finds itself between fiercely opposing forces. On the one hand is the rapid surge in jobs seen during May and June and the consequent swelling of recovery expectations. Opposing these forces however is the dramatic increase in the COVID-19 new case count this month to worrying new highs. While equity markets continue to focus on the positives, looming downside risks seem likely to assert.

The May and June employment reports were unequivocally strong, with a cumulative 7.5 million new jobs created on a nonfarm payrolls basis and a 3.6ppt decline in the unemployment rate also reported — the latter despite a 1.3 percentage point increase in the participation rate over the period. Though questions remain over the quality of survey responses, it seems likely that slack missed by the survey is also diminishing. For June, the BLS reported that those misclassified as employed rather than unemployed was down to around 1% of the labour force, from 3% in May.

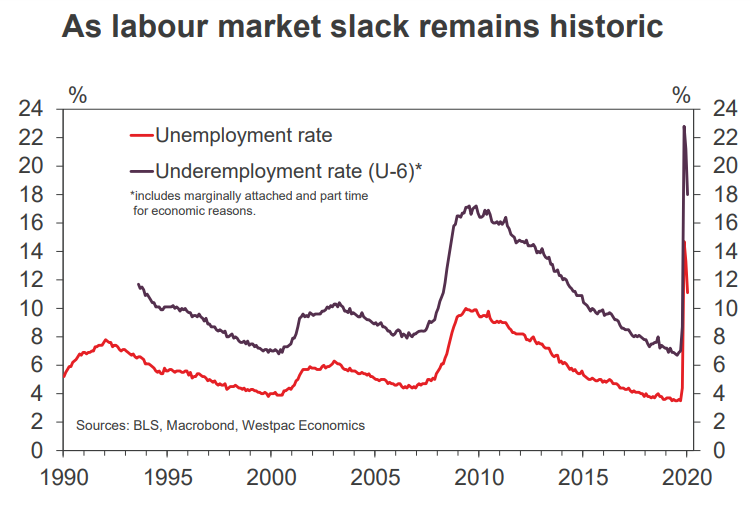

Despite this job swoon, US labour market slack remains immense. The unemployment rate (excluding the potential misclassification of workers) currently sits at 11.1%, above prior recession peaks. At 18%, the broader U6 measure of labour underutilisation is similarly concerning, being more than 10ppts above its pre-COVID level. To see the full effect of COVID-19 reversed, the gains of May and June would have to be repeated twice over. This seems highly unlikely.

The reason this is the case is multi-faceted. First of all, the starting point for this recovery is abnormally weak given the savage nature of the shock. Secondly, despite all the headlines reporting an increase in leisure activities as summer begins, restrictions against COVID-19 remain in force across the economy, limiting the capacity of activity to pick up. Third, this situation seems very unlikely to change for the better anytime soon. Instead, with the daily new case count having reached 59,000 this week, a tightening of restrictions seems more likely than not.

To give a sense of the scale of the impact this recent acceleration in the case count could have on economic activity, this month we have revised down our 2020 year-average growth forecast by a percentage point, from -5.5% to -6.6%. Primarily this stems from the recovery being delayed until the December quarter, the growth previously factored in for the three months to September essentially foregone. Our profile still includes a robust recovery from the December quarter and sustained gains through 2021, but clearly there are considerable risks around this view.

Apart from the immediate threat from COVID-19 to lives and the economy, the other major risk the US faces is political. Specifically: the end of existing fiscal stimulus; a sharp deterioration in revenue at the state and local level; and a seeming inability for politicians to give this crisis the urgent and considered attention it needs.

On policy itself, the primary direct support to household incomes from the US Congress’ CARES Act will progressively be wound back from 31 July absent an extension. The $600 a fortnight supplement paid to recipients by the Federal Government, which more than doubled the average unemployment benefit across the states pre-COVID, will expire on that date. The additional 13 weeks of benefit access also approved will subsequently expire at year end.

This is not the only support that will disappear however. The Paycheck Protection Program, which has provided over $500bn in forgivable loans to small and medium sized businesses in the US (primarily to pay wages and entitlements) is also being running down. While loans can still be approved until early August, only about a fifth of the funds available under the program remain uncommitted. Further, loans already granted must be used within 24 weeks to be eligible for forgiveness. With the bulk of loans having been approved in April/May, this indirect government support for household incomes will also fall away quickly in the final three months of 2020.

When considering the potential shocks before the US, we also have to factor in the health of state and local governments as the new fiscal year begins. These entities cannot borrow to fund ordinary expenses and so, in the absence of Federal support, must aggressively cut their spending on essential services as their revenue (principally from income, sales and property taxes) falls away.

Between February and June, approximately 1.5 million jobs were cut by these public authorities. A third of this loss was seen in May and June even as private jobs surged back. The more stringent and persistent lockdown measures have to become to combat the virus, the worse this job loss will be.

We need to note that, as we write, President Trump seems much more interested in continuing to push for the quick re-opening of the economy than victory over the virus. Highlighting this, he has threatened to withdraw funding for schools that do not re-open in the fall. Doing so could make a very difficult situation for municipalities disastrous, causing rapid and sustained job loss in critical sectors of the US economy such as primary education.

The above also speaks to our broader concern regarding politics currently. Ahead of November’s election, there is a high risk of political decisions/ indecision creating adverse outcomes at a particularly inopportune time. These concerns bear careful monitoring.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.