We have now revised our estimates of the Federal budget deficits for 2019/20 and 2020/21 to $95bn (4.8% of GDP) and $230bn (11.7% of GDP) respectively, amended from $80bn and $170bn.

The lift in the estimated deficit for 2019/20 is due to an upward revision to the cyclical deficit.

The 2020/21 budget deficit is comprised of: a cyclical deficit of $100bn (5% of GDP); around $90bn in fiscal stimulus – as already announced; as well as about $50bn of new spending – which includes approximately $35bn to extend and modify the JobKeeper (JKP) and JobSeeker packages (JSP) plus a $15bn stimulus package to be unveiled on budget day in October.

Details behind our thinking on these issues appear below. We have endeavoured to set out a framework for considering this highly complex issue and providing some rational basis for what is certain to turn out to be a staggering deficit (11.7% of GDP) in 2020/21, if only by Australian standards.

The Treasurer is scheduled to provide an economic and fiscal outlook on July 23 when some official estimates of these fiscal forecasts will be available although it is unlikely that the policy implications which we are considering in this document will be available. The annual budget will be delivered in October.

1. The Cyclical Deficits

The Australian Federal budget moves sharply into deficit during economic recessions. The marked contraction in activity associated with economic shocks or recession leads to the jaws of death for the budget: falling revenues and rising expenditures.

On March 31, when we wrote on the budget outlook in the context of the COVID global pandemic, we noted that history suggests we could expect the cyclical budget deficit to potentially be around 2% of GDP in the initial year of the shock, 2019/20, rising to 4% in the second year. Any additional government spending measures – policy stimulus – would add to the deficit over and above the cyclical deterioration.

It now appears that the cyclical deficit for 2019/20 will be more than 2% of GDP, closer to 2.75% of GDP, or around $55bn.

Monthly financial statements are available to May. These show that the deficit for the year to date, the eleven months to May, is some $64.9bn. This includes a deficit of $24.9bn for the month of May. Revenues for May were down on the same month a year ago by close to 19%. Expenditures have exploded to be almost 50% higher than the same month a year ago. Based on these trends, we estimate that the deficit for June will be approaching $30bn. For the 2019/20 financial year, that has the annual deficit at $95bn.

Of the $95bn deficit for 2019/20, about $40bn is due to new policy measures introduced in response to the pandemic. Recall that to date the government has announced around $140bn in fiscal policy measures, with around $40bn in the initial year, rising to almost $90bn for 2020/21, as well as $6bn for 2021/22.

The remaining $55bn of the $95bn budget deficit for 2019/20 is the cyclical component, which has jumped from a balanced position in 2018/19. In this pandemic recession the deterioration in economic conditions was particularly compressed – rather than being spread over a number of quarters as is typically the case.

This feature was evident in the labour market, with employment contracting by a dramatic 6.4% and hours worked by around 10% in the space of only two months, during April and May.

The unemployment rate jumped from 5.2% to 7.1% over the period and would have been 11.4% if the participation rate had remained unchanged. With this rapid deterioration in conditions the cyclical deficit has surprised to the high side in 2019/20 – coming in at around 2.75% of GDP, rather than the 2% which we had originally estimated.

For the 2020/21 financial year we had anticipated a cyclical deficit of 4% of GDP. The 4% was comprised of a 2% base effect from 2019/20, the initial year of the shock, plus a further 2% deterioration in the 2020/21 year. We have revised the 2020/21 cyclical deficit to 5.0%, taking on board the weaker starting position for 2019/20 (2.75% vs 2.0%) and allowing for a slightly larger deterioration in 2020/21 than originally anticipated (2.25% vs 2%) mindful of the deep damage to the labour market from the current crisis. Given the highly compressed shock to activity in April/May 2020 we do not expect the additional deterioration to the cyclical deficit in 2020/21 to be as severe.

2. The Scaled Unwinding of JobKeeper

The government is faced with a challenge to balance the need to ease back on the JobKeeper Payments (which are scheduled to expire in September) and the requirement to maintain support for the economy particularly for those employers who will continue to have their businesses affected by the ongoing restrictions which will be necessary to maintain control of the virus.

These key restrictions will include social distancing requirements and the closure of Australia’s international borders. We expect that by end September all domestic borders will have reopened.

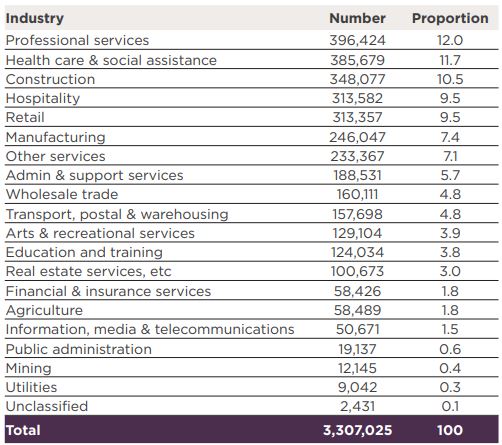

Senate Estimates report the following industry concentration of the individual recipients of JKP:

Recall that an employer qualified for JKP by documenting through the Business Activity Statement a 30% (GST turnover below $1 billion) or 50% (GST turnover above $1 billion) reduction in turnover in the month compared to the same period one year earlier. Importantly, applicants are able to determine projected turnover for the current month, which has typically

mainly been for the month of April.

While we expect that the beneficiaries of the extension of JKP will be mainly determined by the exposure an employer has to the ongoing restrictions there will be cases where the government will see the need, based on the original criteria, to extend support for other employers.

It is also reasonable that those employers in the directly affected industries who cannot continue to meet the earlier criteria will not receive an extension.

Based on the above table we would expect that employers covering significant parts of: arts and recreation (129,104 employees receiving JKP); hospitality (313,582); education and training (124,034); and transport postal and warehousing (157,698) would still be in need of support. These industries currently represent 22% of the current workers receiving JKP.

However, not all employers in these categories will continue to be affected.

The main transport worker effect will be around air travel. The education impact will be centred on foreign students, although the numbers above are unlikely to include universities which are required to include Commonwealth grants and apply the criteria over a six month period, effectively excluding them from the program.

In addition there will be employers in other industries who will be able to make credible cases for ongoing support potentially based on their indirect exposure to the ongoing restrictions.

These industries may include retail; manufacturing; media; and construction.

For example, construction firms engaged in residential accommodation for foreign students or hotel construction may have a strong case.

In that regard, another useful update was recently released by the ABS which reported survey results from June where 53% of respondents in hospitality were recording a revenue reduction of more than 50%. Other badly affected industries were arts and recreation (46%); media and telecommunications (42%); and education (25%).

On the other hand: retail (19%); construction (15%); professional services (16%) and real estate (9%) were showing promising signs of recovery, albeit with some employers still facing tremendous difficulties.

The decision on how to extend JKP will come down to some qualitative judgements from the government and clear evidence that the business is still qualifying under the original turnover conditions.

We have factored in a further three month extension for employers covering around 33% of the current 3.3 million employees, with half of that number, representing those employers directly impacted by the ongoing restrictions, gaining a further six month extension – taking them through to the end of the 2020/21 financial year.

This longer term group would represent around 500,000 employees, which, based on the numbers currently receiving JKP would cover arts; hospitality and air travel.

Indeed we cannot rule out the possibility of some firms gaining even longer term support specifically in the absence of a vaccine or affordable anti- viral drugs as border and distancing rules continue to inhibit their businesses.

That extension is estimated to add around $24bn to the estimated cost of JobKeeper in the 2020/21 fiscal year.

Before the introduction of JobKeeper the government announced a number of policy responses to boost the cash flow of employers. Payments are in two stages – one from April 2020 ( estimated cost of $14.9 billion) and one from July 2020 (estimated cost of $17 billion). These payments which are equal to the salary withheld for tax purposes of employees up to a maximum of $50,000 for each payment are assumed not to be extended.

3. The Downscaling of JobSeeker.

Under our assessment employers covering 2.2 million employees will lose the JKP payments in September.

Current large users of JKP (see above table) are the professional services; health care; construction; retail and manufacturing.

The ABS report indicates that as at mid-June there were still many firms in those industries facing extreme difficulties (revenue down 50% in June year on year). We estimate that there will be some scope in the transition package to accommodate those firms but most of those firms will lose the JKP.

Inevitably, some employees will have to transition from JKP to unemployment benefits. On the other hand, given the uneven nature of this recession, there will be other employees who will transition off unemployment benefits into the workforce. We are currently forecasting a lift in GDP in the December quarter of 2% as further confidence returns to the economy. On balance we are factoring in a steady unemployment rate of 8% across the December quarter.

We are estimating that the government will lift the original Newstart payment by around $230, effectively reducing the JobSeeker Payment (JSP) from about $1150 to around $850 per fortnight. That will be around 60% of the minimum wage – striking that difficult balance between providing a “living wage” and ensuring incentive and competitiveness for the unemployed.

It will represent a 25% reduction in the JSP but a permanent near 40% increase in the original Newstart.

That adjustment is estimated to add around $11bn to the budget deficit for fiscal 2020/21.

4. The October Federal Budget

The “theme” of the October Budget – which was delayed from the usual timing of May – is likely to be around policies that will increase the fiscal stimulus while not embedding ongoing costs into the Budget as will happen with the permanent lift in Newstart.

That can be achieved by: bringing forward the personal income tax cuts that are already legislated to begin in July 2022 (annual cost of around $14 billion); providing a “one off” payment to lower income recipients to supplement the benefit of the tax cuts; and some targeted lift in infrastructure expenditure. (Recall that the government has already committed to a $750 payment in July to social security; veteran and other income support recipients including pensioners, costing $3.9 billion following a similar payment in April costing $4.9 billion.)

The initial two measures in the package would act to boost household incomes, which in turn will act to lift consume spending. We are not expecting any changes to the corporate tax rate. While business investment outside the mining sector has been near decade lows as a proportion of GDP the motivations behind a sustained lift in investment are likely to be around expectations of stronger demand and the benefits to productivity from reform rather than a lower tax rate.

The third measure would act to directly boost activity through construction activity, with the nation still facing an infrastructure deficit after years of brisk population growth. The choice of infrastructure should also be influenced by the expected boost to productivity.

There may be other initiatives as well, some of which could focus on boosting health spending, or dealing with other aspects of the current health crisis.

The October fiscal package may be in the order of around $15bn. Of this almost half would be income tax cuts ($7bn over six months), with the remainder split between the one-off cash payment and additional infrastructure work.

5. Government Debt

On our figuring, the cumulative budget deficit for the years 2019/20 and 2020/21 is $325bn. That compares with the government’s pre crisis forecasts for a cumulative surplus of $11.1bn.

This budget deterioration will boost debt levels by $336bn.

Net debt will rise to a still manageable $715bn in mid-2021, 36% of GDP. That is up from $374bn, 19% of GDP at mid-2019. Gross debt on issue will climb to about $895bn in mid-2021, 45% of GDP. That is up from $542bn, 28% of GDP at mid-2019.

Importantly, the 10 year government bond yield is trading at less than 1% currently, well below Australia’s medium-term growth potential. That suggests that a temporary increase in government debt levels is not a concern for now.

Furthermore, international agencies are generally projecting fiscal slippages of around 15% of GDP over the two years for most developed economies not out of line with the estimates we are making for Australia in this note.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.