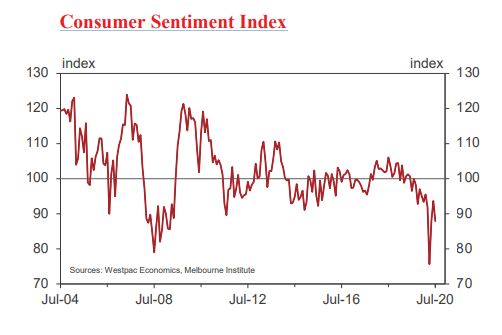

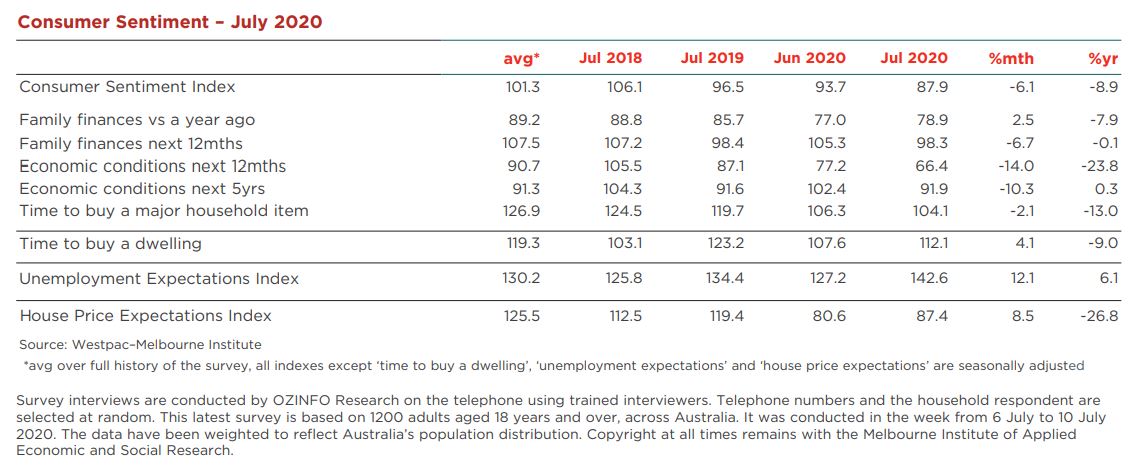

• The Westpac-Melbourne Institute Index of Consumer Sentiment fell 6.1% to 87.9 in July from 93.7 in June.

The drop in confidence reverses all of last month’s impressive gain, taking the Index back to the weak levels seen in May but still leaving it 16% above April’s extreme low of 75.

The timing of the survey is relevant. It covered the week in which the lock down was announced for Melbourne but the survey closed before the news of a significant cluster was reported for Sydney.

Sentiment has been rocked by the resurgence in Coronavirus cases over the last month. After averaging about ten a day through late May and early June, new cases have lifted significantly, running at close to 200 a day in the July survey week. These increases have been almost exclusively in Melbourne prompting the state government to reinstate lockdowns for the city and several regional areas, and the closure of Victoria’s state borders – measures that were announced in the first half of the survey week. Daily responses suggest these announcements were followed by a slight firming in sentiment in the second half of the week.

It is of some concern that the survey pre-dates the news of a significant cluster of cases in Sydney which emerged last weekend – a day after the end of the survey.

State readings underscore the importance of virus-related developments: Victoria’s sentiment index plunged 10.4% in July but sentiment across the rest of the nation showed much milder declines (down 4.5% on a combined basis).

While milder, the weakness in other states is also likely to be linked to the outbreak in Victoria, reflecting concerns about the virus spreading interstate and spill-over effects on the wider economy.

The component detail shows the renewed COVID threat hit consumer expectations for the year ahead hard but also significantly undermined medium-term expectations for the economy.

The ‘economy, next 12mths’ sub-index recorded the biggest decline, slumping 14% in July to be 25% below pre-COVID levels – that compares to the 40% drop during the ‘first wave’ of the virus in March-April.

The ‘economy, next 5yrs’ sub-index recorded a sharp 10.3% fall. This is disconcerting as medium- term expectations for the economy held up reasonably well during the initial COVID shock – only falling 5.1% in March–April – and were slightly above pre-COVID levels in June.

Our read is that whereas previously respondents were confident that the damage from the virus would be shortlived, the set-back over the last month raises significant questions. The looks to have been a substantial loss of confidence around the ability to contain the virus permanently, limiting the extent to which the economy can return to business as usual.

Certainly, the renewed outbreak points to a slower and more difficult path ahead for the foreign education, hospitality and tourism sectors all of which may see longer lasting restrictions even if the latest outbreak is successfully contained.

Employees of businesses that are indirectly affected by these likely extensions to the disruptions will also be unnerved.

The hit to sentiment around family finances was much milder. The ‘finances, next 12mths’ sub-index fell 6.7%, consistent with the more difficult path ahead.

However, the ‘finances vs a year ago’ sub-index ticked up slightly, rising 2.5%. This reflects significant ‘reopening boosts’ in other states and government income support packages that more than offset the negative impact of Melbourne’s renewed lockdown. This point is clearly borne out by the 6.5% fall in this component in Victoria in contrast with the increase in the national index.

The pull back in buyer sentiment was also mild, the ‘time to buy a major item’ sub-index dipped just 2.1% to 104.1.

That said, the index reads are significantly softer in Victoria (99.6) compared to other states (averaging 105.6). In both cases, the sub-index is still well below the long run average of 127, reflecting a mix of ongoing social restrictions, health concerns about entering potentially crowded shopping spaces, pressure on family finances and a reluctance to make big ticket spending commitments while there is a heightened threat of job loss.

Job loss concerns escalated sharply in July. The WestpacMelbourne Institute Unemployment Expectations Index surged 12.1%, reversing much of the surprisingly strong 19.5% improvement in May-June (recall that higher readings indicate that more consumers expect unemployment to rise in the year ahead). At 142.6, the index is now well above its long run average of 130, consistent with consumers expecting a further rise in the unemployment rate over the next year.

Consumer expectations for unemployment have tracked closely in line with their medium- term expectations for the economy in recent months – the latest deterioration reflecting a reassessment of ongoing COVID disruptions and a slower reopening. For jobs, this may also be combining with concerns about the imminent winddown of the Federal government’s JobKeeper Payments scheme, which is due to expire at the end of September.

In effect, employees that might previously have expected a reopening of the domestic economy to ensure they retained their jobs beyond September may be getting much more concerned about their work prospects.

Housing-related sentiment bucked the wider trend in sentiment in July, posting a moderate improvement, albeit with an uneven pattern across states and while price expectations remain deeply negative.

There were significant differences across the states in the ‘time to buy a dwelling’ index. Nationally it rose by 4.1% to 112.1, a six- month high but still well below the long run average of 120. State index moves varied materially: up 3.8% in Victoria; steady in NSW; but surging in Queensland (16.6%); South Australia (14.6%) and Western Australia (7.2%). Index levels tell a similar story with Victoria (103.8)

and NSW (106.9) lagging well behind Western Australia (124), Queensland (122) and South Australia (120). Clearly, affordability is a key driver of this discrepancy but developments this month also point to a significant COVID effect emerging for housing across the nation.

Consumer expectations for house prices also posted a solid gain, the Westpac-Melbourne Institute House Price Expectations Index rising 8.5%. However, at 87.4, the index remains in deeply pessimistic territory, 42% below the optimistic readings immediately prior to the COVID shock in March-April. Expectations lifted across all states including Victoria which rose by 6% although the state index is still 50% below its pre COVID high.

The Reserve Bank Board next meets on August 4. The Board will maintain its current highly stimulatory stance and continue to commit to steady policy for the foreseeable future.

The interest around the RBA will be the release of its latest economic forecasts on August 7. The most significant revision is likely to be the forecast that the economy will grow by 6% in 2021. That is twice the pace expected by Westpac, which is more in line with the messages around today’s survey.

More immediately, the government is scheduled to announce a fiscal update on July 23. While the government is likely to release some revised economic forecasts most attention will be on its policy intentions for the December quarter and beyond. Before the news of the Melbourne closures, Westpac had revised its budget deficit estimate for 2020/21 to $240b from the $170b which we released in May. That revised estimate incorporated around $50b including extensions to JobKeeper ($24b); JobSeeker ($11b) and further stimulus in the October Budget ($15b).

With this sharp relapse in Consumer Confidence stemming from the latest news on the closures in Melbourne the policy response is likely to be even greater.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.