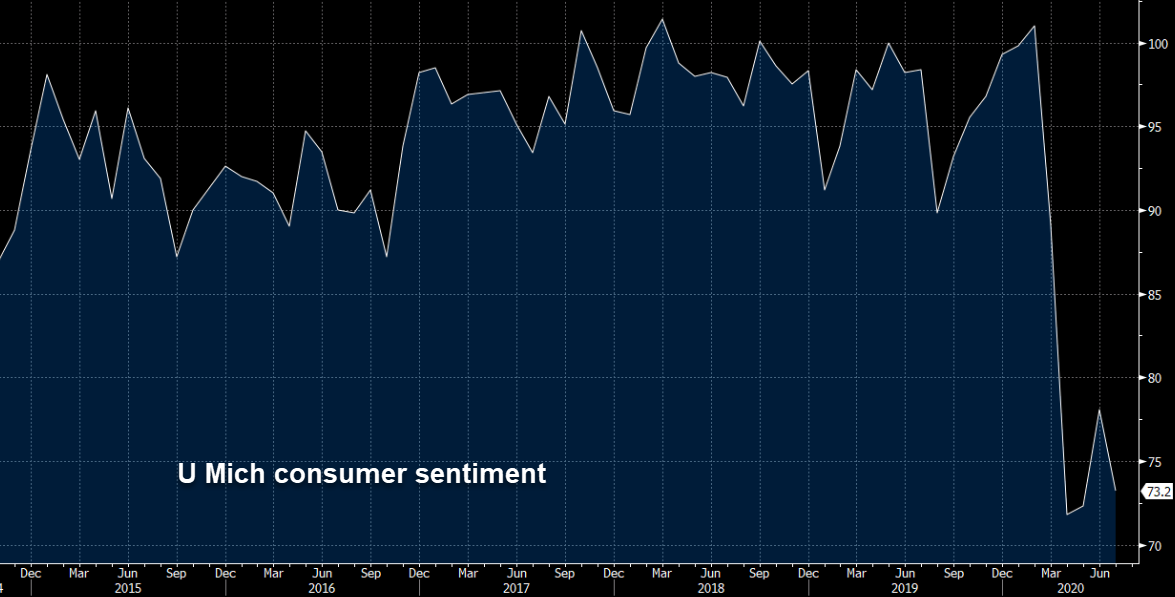

The US consumer has choked. Michigan Consumer Confidence:

Consumer sentiment retreated in the first half of July due to the widespread resurgence of the coronavirus. The promising gain recorded in June was reversed, leaving the Sentiment Index in early July insignificantly above the April low (+1.4 points). Following the steepest two-month decline on record, it is not surprising that consumers need some time to reassess the likely economic impact from the coronavirus on their personal finances and on the overall economy. Unfortunately, declines are more likely in the months ahead as the coronavirus spreads and causes continued economic harm, social disruptions, and permanent scarring. Another aggressive fiscal response is urgently needed that focuses on financial relief for households as well as state and local governments. While financial relief is clearly needed for the most vulnerable households, that relief will not stimulate the extent of renewed consumer spending necessary to restore employment and income to pre-crisis levels anytime soon. No single policy could provide financial relief and stimulate economic growth, and without both, neither one could be ultimately successful. Unfortunately, there is little time left on the political calendar for Congress to act as the election season is about to begin in earnest. Without action, another plunge in confidence and a longer recession is likely to occur.

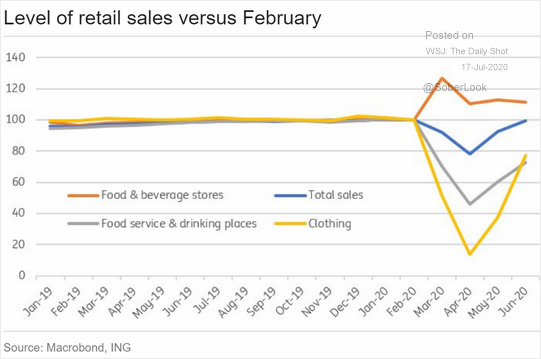

Some retail was good in June but will sink ahead:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.