10,000 more Australians will be able to buy their first home from today with a deposit as little as 5% thanks to our First Home Loan Deposit Scheme. We’re proud to have already helped 10,000 Australians into their first home in the first year of the new scheme. https://t.co/QjDMGJyvLJ

— Scott Morrison (@ScottMorrisonMP) July 1, 2020

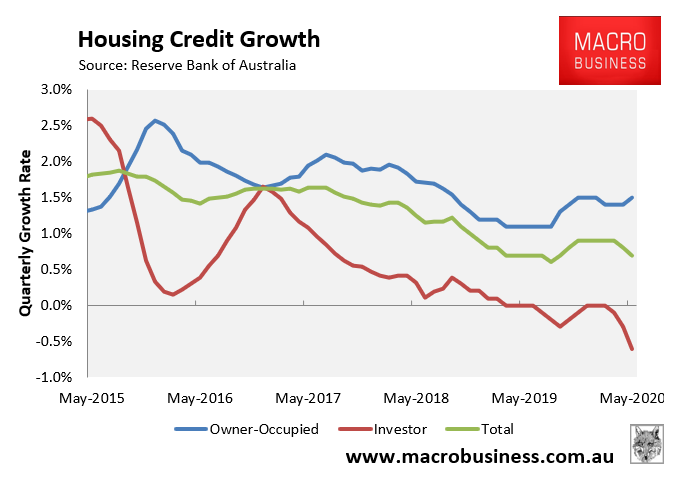

A great time to celebrate as property investors handoff losing assets to 1ok extra FHB patsies: