Adam Creighton has penned another thought provoking article questioning Australia’s compulsory superannuation system, which he claims has turned “rotten” and needs major overhaul:

I remember where I was a decade ago when I read the section of the Henry tax review that dealt with retirement income policy. It was a shock. “An increase in the superannuation guarantee would also have a net cost to government revenue even over the long term (that is, the loss of income tax revenue would not be replaced fully by an increase in superannuation tax collections or a reduction in age pension costs)”…

Excuse me? I reread it. It’s true. Increasing the compulsory rate of superannuation from 9 per cent to 12 per cent doesn’t save taxpayers money.

Indeed, it’s worse than that. The vast, artificial, highly complex edifice of compulsory super costs taxpayers a fortune. That, in turn, requires other taxes to be higher than necessary…

“The $32bn a year in fees and the $36bn fiscal cost of superannuation should be taken into account when calculating the overall success of the system,” [Senator Andrew] Bragg notes.

Together, that’s more than the cost of the Age Pension, the federal government’s biggest single expense — about $50bn this financial year. Those fees are money that could be spent by workers on goods and services. And the forgone tax revenue from taxing super contributions and earnings at concessional rates is money that could slash income tax, boosting incentives to work and save. The entire revenue “cost” of the government’s legislated tax cuts over the four years from last July is $5.7bn. Imagine what you could do with $36bn every year…

Despite offering a superannuation fund via our partners at Nucleus Wealth, MB has consistently argued against Australia’s compulsory superannuation system (in turn against our own financial interests).

There are six critical flaws in this system.

First, superannuation is voluntary for those that are self-employed or homemakers, thus missing millions of people.

Second, superannuation can be spent many years before the official retirement age of 66 (rising to 67). Indeed, at age 60, superannuants can remove all their superannuation balance and spend it on consumption goods immediately before falling back on the Aged Pension.

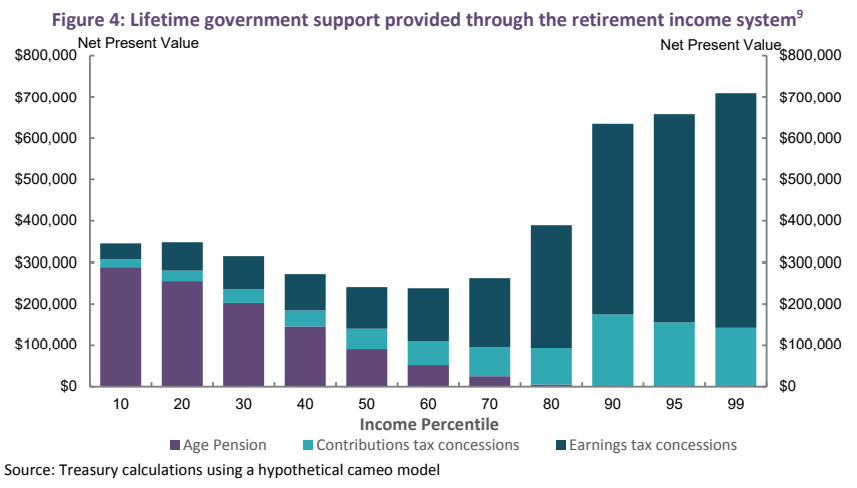

Third, the bulk of superannuation concessions go to where they are not needed (i.e. high income earners), costing the federal budget far more than it saves in Aged Pension costs:

Fourth, superannuation balances at retirement depend on how long one works and how much they earn. This inevitably means that it misses lower income earners and those with broken work patterns.

Fifth, superannuation nest eggs are subject to market risks, meaning one sharp correction in the share market can wipe out a large chunk of retirement balances.

Finally, Australia’s superannuation system is highly inefficient. Management fees are among the highest in the world with Australian households spending twice as much each year on superannuation fees as they do on electricity.

The number of people employed in Australia’s superannuation industry is also wasteful, dwarfing Australia’s entire welfare system and on par with our entire defence force and its bureaucracy.

By contrast, the Aged Pension suffers none of these flaws and should be considered Australia’s genuine retirement pillar.

The Aged Pension is universally available and subject to means testing, meaning it is targeted at those most in need. It is not based upon how much one works or earns prior to retirement. And the Aged Pension is not subject to market risk.

Given the obscene cost, inefficiency and poor targeting of superannuation concessions, optimal public policy dictates unwinding these concessions and using the money saved to boost the Aged Pension.