New data from the Australian Prudential Regulatory Authority (APRA) reveals that the number of Aussies taking out private health insurance has crashed to its lowest level since 2006.

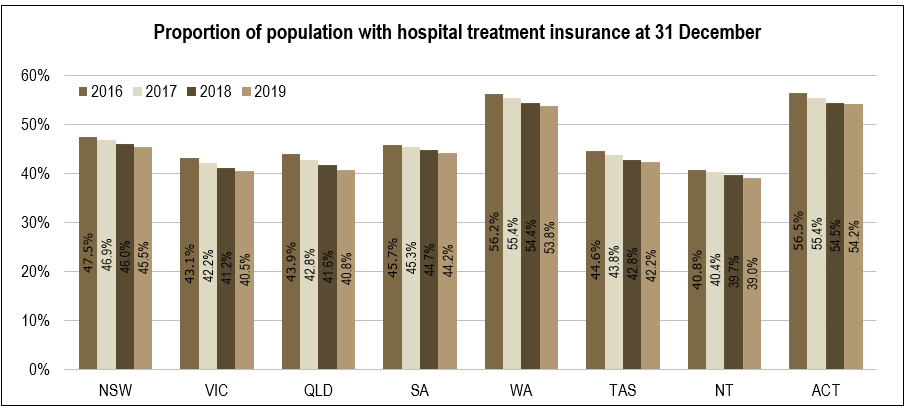

According to APRA, private health hospital coverage of adults fell from 44.7% in 2018 to 44% last year, with losses experienced across all jurisdictions:

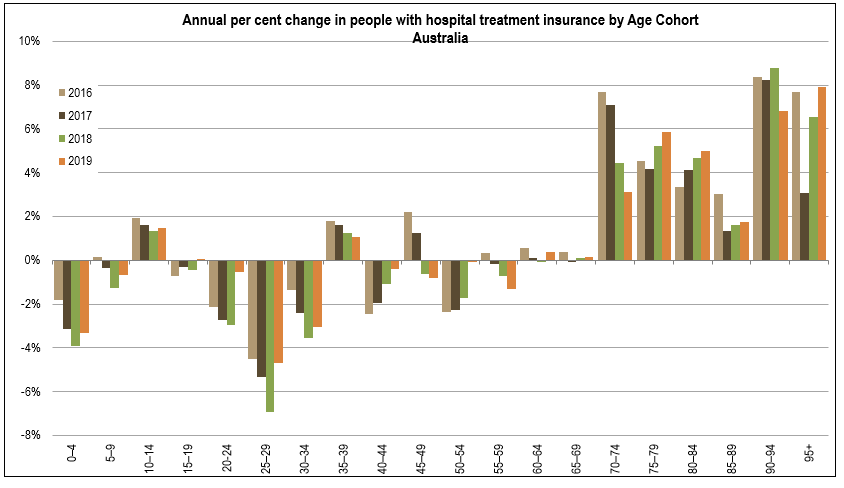

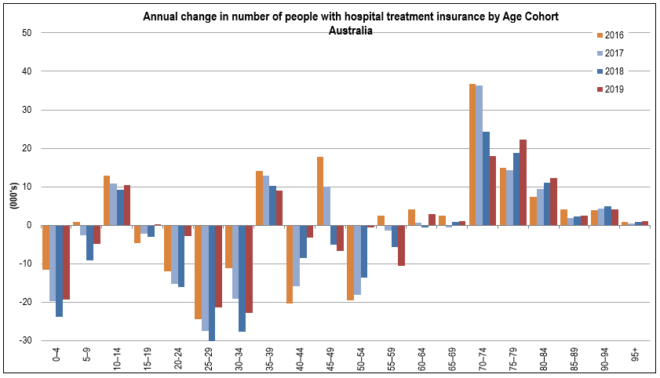

More worryingly, coverage has collapsed amongst healthy young cohorts while rising among the elderly:

The above charts add weight to the claim that Australia’s private health insurance industry is facing a ‘death spiral’. Young and healthy people (the so-called “invincibles”) continue to leave system, thus leaving a larger proportion of unhealthier, older, expensive users.

If this process continues, it will force premium up further, leading to a further exodus of the invicibles, and so on.

Australia’s private health insurance sector can only remain solvent if enough young and healthy people agree to sign-up, since they are the ones who are likely to pay more into the system than they take out.

In the absence of risk-based pricing, the only incentive for these young people to sign up is to avoid penalty – i.e. the Medicare Levy and the lifetime health cover surcharges.

Clearly, these young, healthy cohort perceive that it is cheaper to simply pay the penalties than hold private health insurance, thus helping to explain the clear exodus from the system.

Perhaps policy makers should take this opportunity to investigate whether the private health insurance industry should continue to be supported by taxpayers.

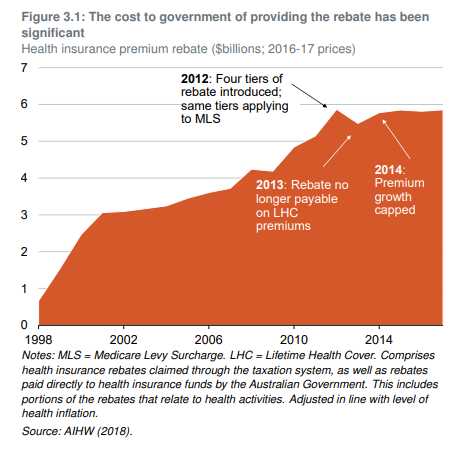

Australians are subsidising private health insurance to the tune of about $9 billion every year: $6 billion for the private health insurance rebate and $3 billion on private medical services for inpatients:

The rebate alone is projected to grow to $7.1 billion by 2022-23, according to the budget papers.

This $9 billion (and growing) of private health subsidies may very well produce more benefits to taxpayers if it was diverted into the public system.

After all, there is no evidence that private health insurance buys patients extra quality and safety. The Productivity Commission (PC) found that the larger, most comparable public and private hospitals had similar adjusted premature death ratios. Further, the PC found that the team-based care in large public hospitals also leads itself to better coordination of care.

Instead of hosing more taxpayer funds to prop-up the private system, maybe it is time to abandon private health insurance subsidies altogether, with the savings instead redirected into the public system?

The system is headed for collapse anyway.