Mortgage offset accounts flooded with early super money

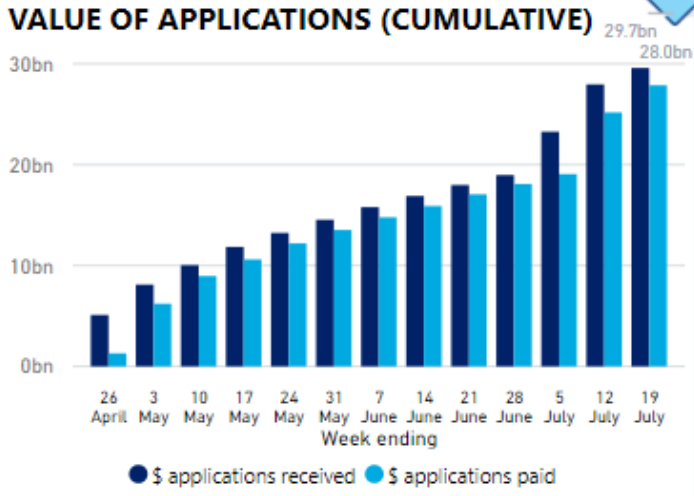

As we know, early withdrawals from superannuation ballooned to $28.0 billion in the week ended 19 July:

The Australian Treasury now expects about $41.9 billion in total to be withdrawn from super funds, compared with its previous forecast of $29.5 billion.

Analysis of banking data shows that most of this money is being saved, used to reduce debts or placed in mortgage offset accounts:

Government analysis of banking sector data has indicated the “vast majority” of the early release payments are being saved, placed in offset accounts to reduce mortgage interest payments or put towards debt repayment.

About 58 per cent of early release payments are classified as “saved/unspent” and remain in workers’ accounts…

“We know almost 60 per cent of those accessing their super early have used it or plan to use it to meet essential day-to-day expenses, including paying down debts, with another 36 per cent adding the money to their savings,” the Treasurer said…

Separate Australian Bureau of Statistics survey data has suggested that 60 per cent of those accessing their superannuation early had used it to meet essential day-to-day expenses — including debt repayment – while a further 36 per cent had added the money to their savings.

Paying down one’s mortgage is a good use of savings. The interest saved is pre-tax, so based on an average discount mortgage interest rate of 3.65% and a marginal tax rate of 30%, implies an after-tax return of 4.7%.

Most Australians would also value keeping a roof over their heads above a bit of additional retirement income in 30-plus years.