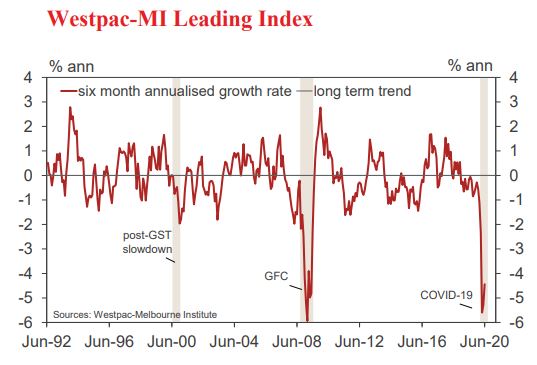

• The six- month annualised growth rate in the Westpac– Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, rose from –5.29% in May to –4.44% in June.

Despite another modest improvement this month, the Index growth rate remains in deep negative territory consistent with recession.

Easing social restrictions have allowed for some lift in activity in June. This is best captured by the increase in contribution to the growth rate in June from US industrial production (added 1.1ppts) and hours worked (added 0.6ppts).

The lift in hours worked in June (ABS estimate showing a 4% rise) is particularly encouraging and means that the contraction in hours worked through the whole of the June quarter was ‘only’ 6.9% compared to the 20% contraction originally expected by the official sector.

That puts some upside risk to Westpac’s current forecast of a 7% contraction in the economy in the June quarter.

However, the developments in July, including the renewed shutdown in Melbourne and the associated 6.1% fall in the Westpac-Melbourne Institute Index of Consumer Sentiment suggest that the profile of the recovery will not be smooth.

Westpac is forecasting the economy to grow by 3.5% in the second half of 2020 but we have recently moved more of that recovery from the September quarter to the December quarter.

Needless to say, the first half of 2020 has seen a dramatic weakening with the Leading Index growth rate dropping nearly 4ppts between January and June – the three months to April marking the sharpest decline in the 60 year history of the measure. Looking over the full six months, two components account for the bulk of the slump: US industrial production (–2.2ppts) and aggregate monthly hours worked

(–1.2ppts). Both recorded exceptionally large contractions as shutdowns impacted through April-May, posting gains in June as economies started to reopen but with activity still well down on pre-COVID levels (10.8% in the case of US industrial production and 6.9% for aggregate hours worked).

Other components have had a more mixed contribution over the first half. Equity markets have provided an additional 0.5ppt drag, with a further 0.4ppt drag from dwelling approvals which posted a particularly sharp 16.9% fall in the May month. However, this has been partially offset by more supportive reads on commodity prices (+0.3ppts) and the yield spread (+0.3ppts).

Sentiment-based components have also had a mixed impact over the first six months but, as noted, showed a sharp decline in early July as the return to lockdown conditions in Victoria impacted. The Westpac-Melbourne Institute Consumer Sentiment Expectations Index fell 10% in the month while the Westpac-Melbourne Institute Unemployment Expectations Index jumped 12.1%, indicating a significant worsening in the outlook for the labour market.

Overall, the component mix points to downside risks near term with the drivers behind the weak July readings on sentiment likely to impact on other, less timely, components that track real activity in coming months.

Yesterday the government released its extensions for the JobKeeper and JobSeeker packages. The JobKeeper extensions only run to March and JobSeeker to December.

The near-term extensions are broadly in line with the estimates underlying our forecast for a $240 billion budget deficit for 2020/21.

However, our forecast assumes additional stimulus of $15 billion to be announced in the Federal Budget in October and a further $15 billion to extend both JobKeeper and JobSeeker through to the end of the fiscal year.

Consequently, if the government’s estimate of the budget deficit in tomorrow’s economic statement includes no more policy adjustments, we would expect an official forecast in the order of $210 billion, ($30 billion less than the $240 billion).

What is clearer after yesterday is the likely financial injection from government policies into the economy in the December quarter. We had expected around $15.6 billion but that now appears to be lower at $13.5 billion.

The challenge for the economy, given that the stimulus in the June quarter was an estimated $65 billion with a further $95 billion for the September quarter, is to adjust to such a sudden reduction in the size of government support.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.