by Chris Becker

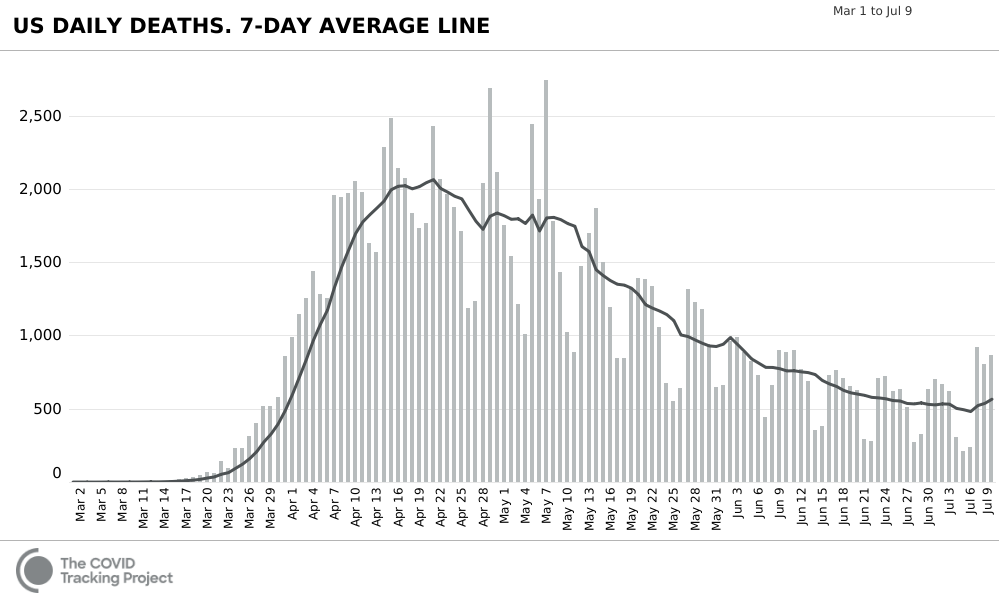

There was an unusual blip in the amount of Americans who died from COVID-19 reported on Tuesday, that could have been written off (as sick as that sounds) as the usual weekend anomaly, whereby deaths over the weekend – in this case a 3 day weekend due to 4th of July holiday – are reported on the first working day of the week.

But with three consecutive days of nearly 1000 deaths recorded each day? That’s a new trend: