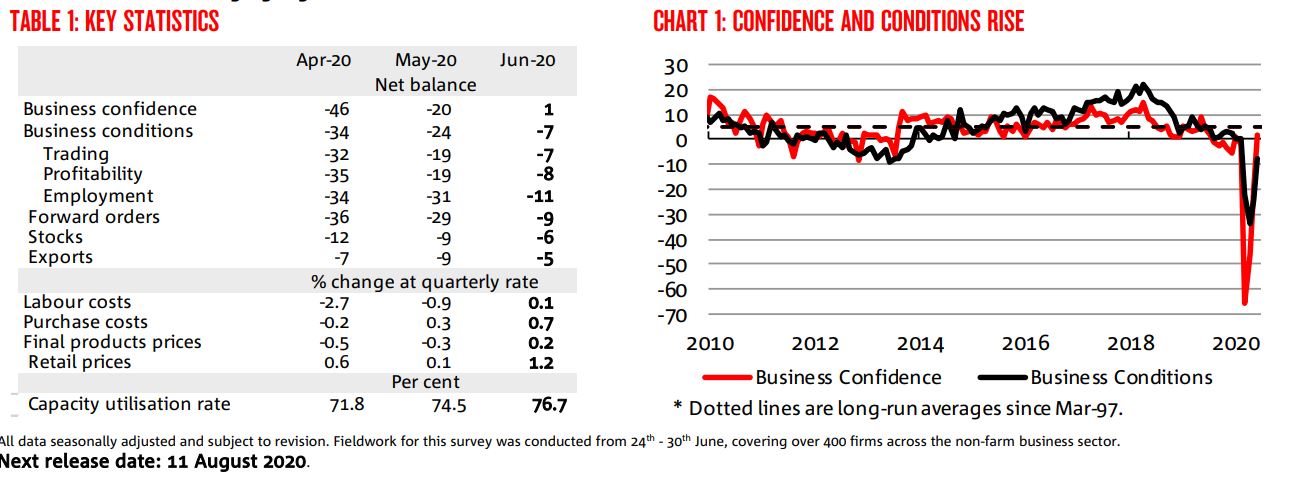

• How confident are businesses? Confidence rose by 21pts to +1 index points in the month – a third consecutive large increase in confidence.

• How did business conditions fare? Conditions rose 17pts to -7 index points – but remain very weak.

• What components contributed to the result? All three subcomponents saw significant improvements – led by a 20pt increase in the employment index. Trading conditions and profitability rose 12 and 11pts respectively.

• What is the survey signalling for jobs growth? The employment index has improved substantially over the past two months but remains negative implying some ongoing job shedding but that this has likely slowed.

• Which industries are driving conditions? Conditions rose across all industries – with mining and retail seeing the biggest increases. Outside of mining, retail now sees the best conditions followed by transport & utilities. The remaining industries remain notably weaker, with the services sectors still weakest. Manufacturing and construction also remain negative, highlighting an ongoing risk in these sectors from secondary spill-overs from the slowdown in economic activity.

• Which industries are most confident? Confidence increased everywhere except retail and is now positive in all industries except retail and construction. Mining is now the most optimistic across industries, while construction is weakest.

• Where are we seeing the best conditions by state? Conditions improved in all states in the month, with WA seeing the largest improvement. It is now the only state to see positive conditions while SA and Tas are now the weakest. Vic remains the weakest of the east coast states – but Qld and NSW still see negative conditions.

• What is confidence like across the states? Confidence rose in all states with NSW, WA and QLD leading gains on the mainland. Confidence is now positive in NSW, Tas, and WA and negative in Vic and SA. QLD lies at 0 index points.

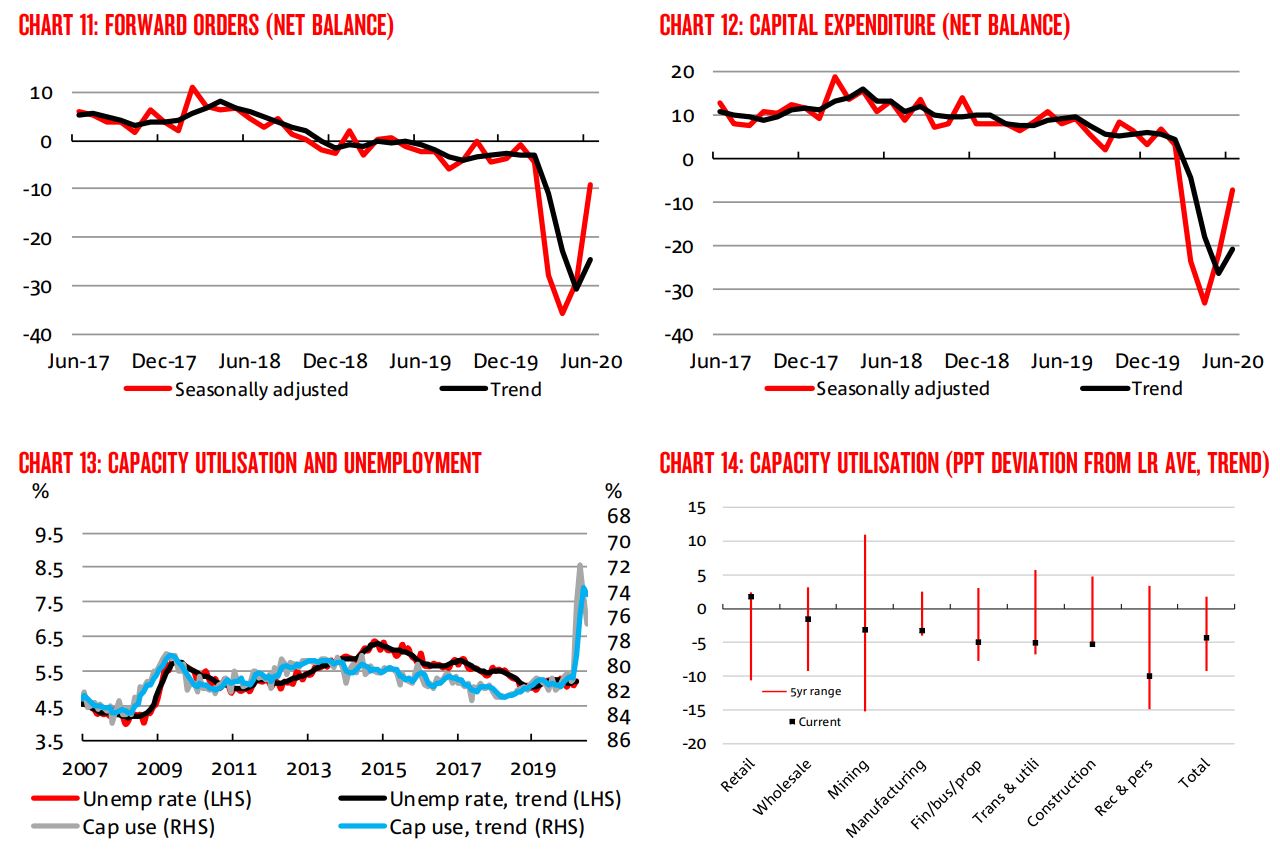

• Are leading indicators suggesting further improvement? Forward orders saw a large improvement in the month but remain significantly negative and well below average. Capacity utilisation continued to recover but remains very low. Overall, there has been a notable improvement in leading indicators in the past two months but they remain weak.

• What does the survey suggest about inflation and wages? Retail price inflation picked up in the month, while final products prices also rose, following weakness last month. The decline in labour costs (a wage bill measure) appears to have abated with costs edging higher in the month.

Capacity utilisation still disastrous:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.