From Gareth Aird, head of Australian economics at CBA:

Key Points:

The July Economic and Fiscal Update(JEFU)is scheduled for release at 9.30am (AEST) 23 July.

JEFU should contain a full suite of economic forecasts and the projected fiscal position for the next two years.

We expect clarity on what form JobKeeper and JobSeeker will take post September.

The Government may also bring forward the already legislated 2022 personal income tax cuts.

Our point estimate for the budget deficit in 2020/21is $A190bn (10% of GDP).

July Economic and Fiscal Update (JEFU) – CBA Preview

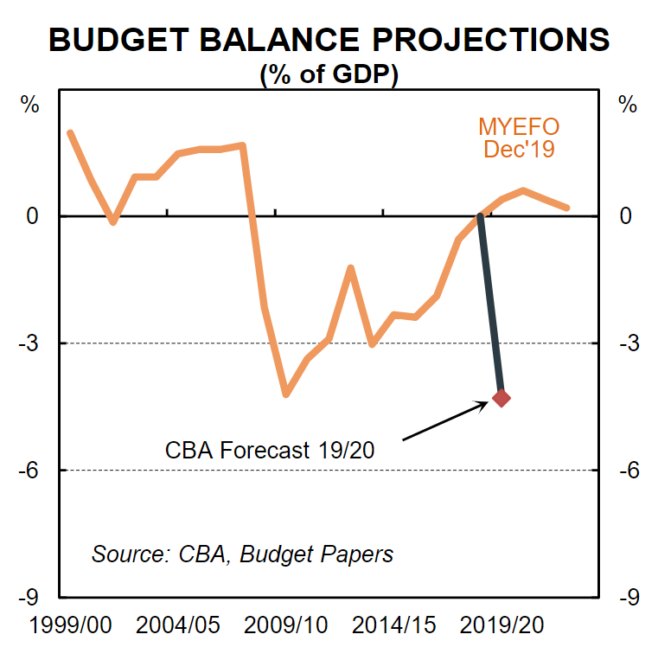

Back in March the Government took the decision to defer the originally scheduled May 2020/21 Budget to October 2020 due to the COVID-19 pandemic. As a result, we have not had any detailed economic or fiscal projections from the Government since the December 2019 Mid-Year Economic and Fiscal Update (MYEFO). We have received individual costings for each component of the Government’s economic response to the pandemic. And we have had the odd forecast for GDP or unemployment mentioned by the Government and Treasury Secretary. But in terms of official published forecasts there hasn’t been any since MYEFO in December 2019. What’s for certain is that the old forecasts can be put in the shredder as the world looks completely different due to the COVID-19 pandemic.

We’re not exactly sure what shape and form the JEFU will take. It’s clearly not going to be as detailed as the Budget that is tabled for October. But it should still be something substantial. To hazard at a guess we think the document will most closely resemble the MYEFO in style. It should contain new detailed economic forecasts and fiscal projections including the operating statement, balance sheet and cash flow statement. We suspect the fiscal projections will only go out two years rather than cover the usual four year forward estimates. These are likely to be saved for the October Budget. If nothing else, this gives the government some protection from the uncertainties in the economy that lay ahead.

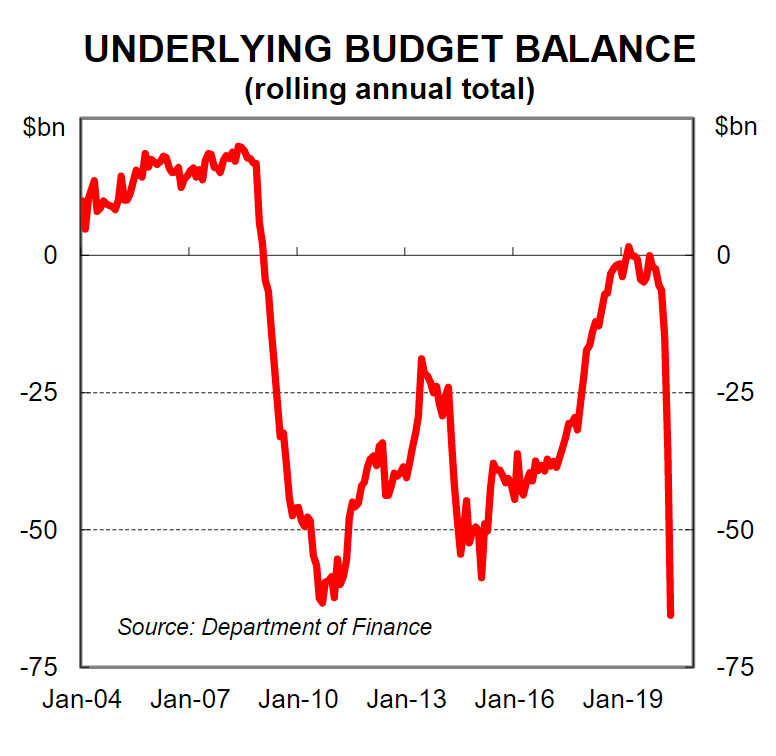

The Government will also publish the 2019/20 Budget outcome. As at May 2019 the year-to-date underlying cash balance was a deficit of $A65bn (compared with a MYEFO estimate of a $4bn deficit). We expect a further $A30bn deterioration over June vs MYEFO and are looking for the final budget outcome to be a deficit of around $A85bn or 4.3% of GDP (versus the $A5bn surplus forecast in MYEFO).The projected fiscal position in 2020/21 and 2021/22 will be a function of essentially two things:

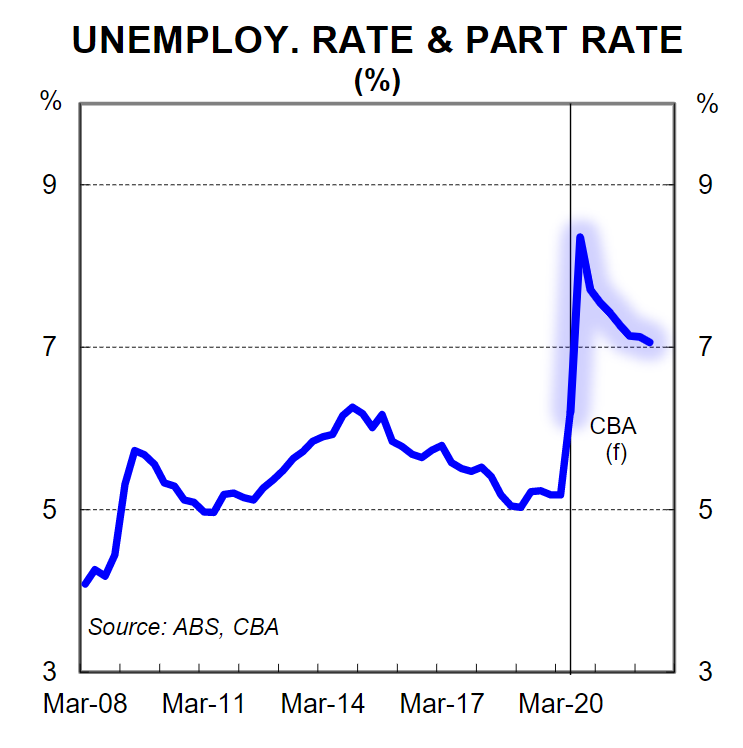

(i) economic forecasts, particularly nominal GDP which drives the revenue side of the equation as well as the level of unemployment which underpins welfare payment forecasts; and

(ii) new policy announcements.

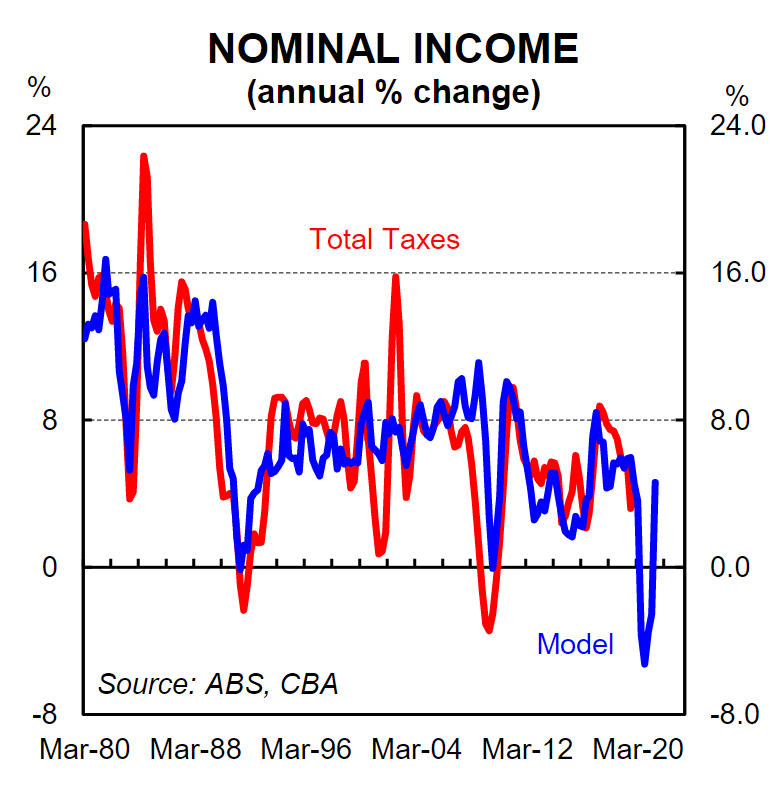

Our model for the future tax take based on our forecast for nominal GDP is suggesting that we are looking at a revenue downgrade of ~$A35bn in 2020/21 versus what was forecast in the MYEFO. That represents a 7% shortfall from the MYEFO estimate.

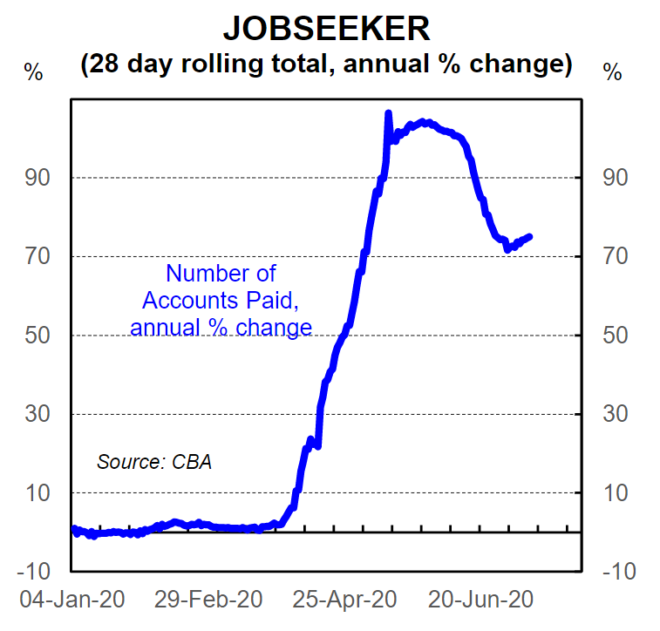

The more significant damage to the Government’s fiscal position is going to come from the expenditure side. Elevated unemployment will mean higher welfare payments. And the Government will continue to provide stimulus payments to the household and business sectors while restrictions on economic activity remain in play. This is where we are shooting in the dark in our forecasts as we do not yet know what the JobKeeper and JobSeeker programs in particular will look like at the end of September 2020.

Currently someone on JobSeeker receives $A1,162 per fortnight ($A612 JobSeeker payment plus the $A550 “coronavirus supplement”). We think the most probable outcome is for the time-limited coronavirus supplement to be retained, but at a reduced amount. For example if the coronavirus supplement was reduced to $A250a fortnight someone on JobSeeker from October 2020 would receive $A862 a fortnight. While that number is illustrative we wouldn’t be surprised to see a number within that ballpark. The Government needs to make sure the payment doesn’t serve as a disincentive for someone to work. Equally it cannot be too lowgiven the current state of the labour market. The right balance needs to be struck.

We are less sure on what may happen with JobKeeper. The recent six week stage 3 lockdown in metropolitan Melbourne raises the probability that JobKeeper is extended in one form or another at the end of September. But it may be that the eligibility criteria is tightened. That may mean that there are changes made to turnover requirements or it may be limited to certain industries. It could also mean that payments are made to employees based on how many hours they worked before the COVID-19 pandemic rather than the one-sized-fits-all approach we currently have.

The Treasurer has also flagged bringing forward the already legislated 1 July 2022 income tax cuts as a policy option to boost demand in the economy. They are estimated to “cost” around $A15bnper annum which is another way of saying the tax cuts would inject $A15bn into the economy. This would result in more spending, economic activity and therefore tax receipts so the true cost to the budget is lower. We are long time advocates of pulling forward the tax cuts and think it would be a good policy move.

In summary, it is impossible to estimate the size of the budget deficits over the next two years without knowing what the new round of policy announcements will be. That said, it we combine our expected revenue downgrade with previously announced stimulus ($A85bn) and another A$75bn of stimulus that might be announced in the JEFU (a reasonable assumption) we land on a budget deficit of $A190bn or 10% of GDP in 2020/21. Of course there is more than one way to skin a cat and our fixed income strategists have extrapolated out the existing patterns of Commonwealth debt issuance so far in 2020/21 and the recent AOFM announcements to find the AOFM currently on pace for a deficit of $A250bn in 2020/21. To be fair, it’s a small sample size to extrapolate over a year. There is also a strong chance that the Government deficit (and hence the AOFM borrowing) are front-loaded in 2020/21. But it’s consistent with our expectation that the deficit is going to be circa a couple of hundred billion dollars. The projected budget deficit will be smaller in 2021/22, but it will still be large. The economy is going to be operating below potential for a long time and that means budget deficits for many years.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Currently someone on JobSeeker receives $A1,162 per fortnight ($A612 JobSeeker payment plus the $A550 “coronavirus supplement”). We think the most probable outcome is for the time-limited coronavirus supplement to be retained, but at a reduced amount. For example if the coronavirus supplement was reduced to $A250a fortnight someone on JobSeeker from October 2020 would receive $A862 a fortnight. While that number is illustrative we wouldn’t be surprised to see a number within that ballpark. The Government needs to make sure the payment doesn’t serve as a disincentive for someone to work. Equally it cannot be too lowgiven the current state of the labour market. The right balance needs to be struck.We are less sure on what may happen with JobKeeper. The recent six week stage 3 lockdown in metropolitan Melbourne raises the probability that JobKeeper is extended in one form or another at the end of September. But it may be that the eligibility criteria is tightened. That may mean that there are changes made to turnover requirements or it may be limited to certain industries. It could also mean that payments are made to employees based on how many hours they worked before the COVID-19 pandemic rather than the one-sized-fits-all approach we currently have.The Treasurer has also flagged bringing forward the already legislated 1 July 2022 income tax cuts as a policy option to boost demand in the economy. They are estimated to “cost” around $A15bnper annum which is another way of saying the tax cuts would inject $A15bn into the economy. This would result in more spending, economic activity and therefore tax receipts so the true cost to the budget is lower. We are long time advocates of pulling forward the tax cuts and think it would be a good policy move.In summary, it is impossible to estimate the size of the budget deficits over the next two years without knowing what the new round of policy announcements will be. That said, it we combine our expected revenue downgrade with previously announced stimulus ($A85bn) and another A$75bn of stimulus that might be announced in the JEFU (a reasonable assumption) we land on a budget deficit of $A190bn or 10% of GDP in 2020/21. Of course there is more than one way to skin a cat and our fixed income strategists have extrapolated out the existing patterns of Commonwealth debt issuance so far in 2020/21 and the recent AOFM announcements to find the AOFM currently on pace for a deficit of $A250bn in 2020/21. To be fair, it’s a small sample size to extrapolate over a year. There is also a strong chance that the Government deficit (and hence the AOFM borrowing) are front-loaded in 2020/21. But it’s consistent with our expectation that the deficit is going to be circa a couple of hundred billion dollars. The projected budget deficit will be smaller in 2021/22, but it will still be large. The economy is going to be operating below potential for a long time and that means budget deficits for many years.

Currently someone on JobSeeker receives $A1,162 per fortnight ($A612 JobSeeker payment plus the $A550 “coronavirus supplement”). We think the most probable outcome is for the time-limited coronavirus supplement to be retained, but at a reduced amount. For example if the coronavirus supplement was reduced to $A250a fortnight someone on JobSeeker from October 2020 would receive $A862 a fortnight. While that number is illustrative we wouldn’t be surprised to see a number within that ballpark. The Government needs to make sure the payment doesn’t serve as a disincentive for someone to work. Equally it cannot be too lowgiven the current state of the labour market. The right balance needs to be struck.We are less sure on what may happen with JobKeeper. The recent six week stage 3 lockdown in metropolitan Melbourne raises the probability that JobKeeper is extended in one form or another at the end of September. But it may be that the eligibility criteria is tightened. That may mean that there are changes made to turnover requirements or it may be limited to certain industries. It could also mean that payments are made to employees based on how many hours they worked before the COVID-19 pandemic rather than the one-sized-fits-all approach we currently have.The Treasurer has also flagged bringing forward the already legislated 1 July 2022 income tax cuts as a policy option to boost demand in the economy. They are estimated to “cost” around $A15bnper annum which is another way of saying the tax cuts would inject $A15bn into the economy. This would result in more spending, economic activity and therefore tax receipts so the true cost to the budget is lower. We are long time advocates of pulling forward the tax cuts and think it would be a good policy move.In summary, it is impossible to estimate the size of the budget deficits over the next two years without knowing what the new round of policy announcements will be. That said, it we combine our expected revenue downgrade with previously announced stimulus ($A85bn) and another A$75bn of stimulus that might be announced in the JEFU (a reasonable assumption) we land on a budget deficit of $A190bn or 10% of GDP in 2020/21. Of course there is more than one way to skin a cat and our fixed income strategists have extrapolated out the existing patterns of Commonwealth debt issuance so far in 2020/21 and the recent AOFM announcements to find the AOFM currently on pace for a deficit of $A250bn in 2020/21. To be fair, it’s a small sample size to extrapolate over a year. There is also a strong chance that the Government deficit (and hence the AOFM borrowing) are front-loaded in 2020/21. But it’s consistent with our expectation that the deficit is going to be circa a couple of hundred billion dollars. The projected budget deficit will be smaller in 2021/22, but it will still be large. The economy is going to be operating below potential for a long time and that means budget deficits for many years.