From Gareth Aird, Head of Australian economics at CBA:

Key Points:

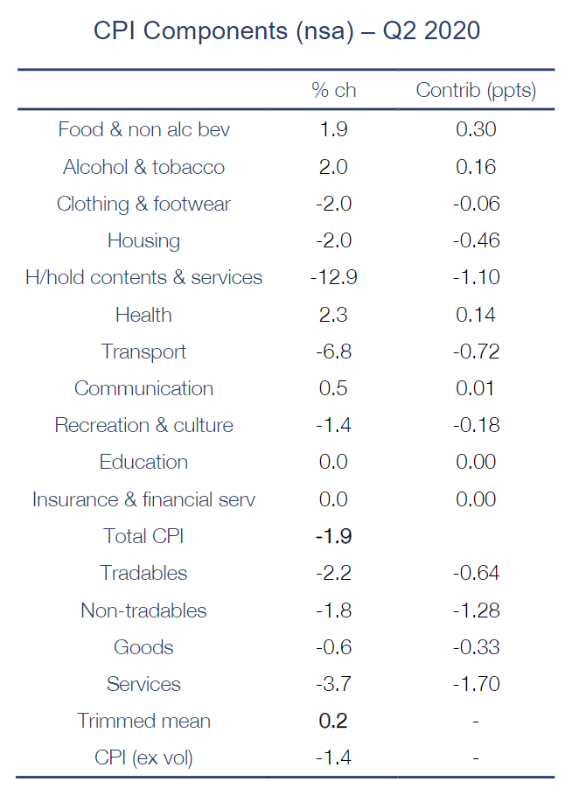

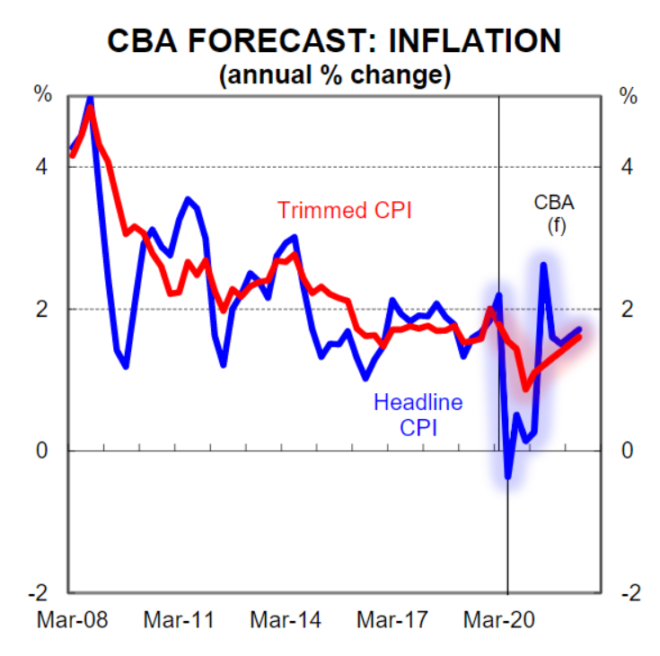

We expect the headline CPI to fall by 1.9% in Q2(-0.4%/yr).

The Trimmed Mean CPI on our forecasts will print at 0.2% (1.5%/yr).

We expect disinflationary forces to persist over the next year given the huge negative shock to the economy.

On Wednesday 29 July the ABS will publish the Q2 CPI. Given all of the ‘crazy’ economic data that has printed over the past three months due to the COVID-19 pandemic the oddities in the Q2 CPI will be taken in their stride. But it’s worth having a closer look at some of the quite irregular dynamics in play that will have a large bearing on the headline outcome in particular. More specifically:

Child care services were free for families from 6 April to 28 June(62 out of 65 business days). This will result in a 95% fall in the CPI child care expenditure class and will shave 1.1ppts from the headline CPI.

Significant changes in the rental property market will result in a large price fall in rents. We estimate that the fall in rents will subtract 0.6ppts from the headline CPI.

13% of the CPI will be missing reflecting unavailable goods and services due to COVID-19 restrictions which means a decent chunk of the CPI will be imputed.

Petrol prices plunged ~20% which is expected to take 0.7ppt from the headline CPI.

Combining all of the above forces with our expectations for the rest of the CPI basked leaves us anticipating a fall in Q2 CPI of 1.9%. Such an outcome would be the biggest quarterly fall on ABS records which date back to 1948. The annual rate is forecast to be -0.4% at Q2 20. It will be the first time annual headline inflation has been negative since 1997.

Underlying inflation is forecast to decelerate but not turn negative. We expect the trimmed mean to rise by 0.2% in Q2 and for the annual rate to ease to 1.5%.

In the grand scheme of things the RBA forecasts in the May Statement on Monetary Policy are broadly in line with our forecasts(RBA -2.5%/qtr headline and +0.2%/qtr trimmed mean –the difference on the headline is probably reconciled by petrol prices which rebounded late in Q2). This means that there aren’t any near term implications for monetary policy. Headline inflation will bounce back in Q3 20 but remain low. And core inflation is expected to sit below the RBA’s target for the next couple of years. This means that the cash rate will sit at its record low of 0.25% for many years and QE will remain part of the landscape.

That all said, we think we will see some greater than usual volatility within the CPI basket itself as restrictions on activity and by extension the supply of some goods and services has an impact on their prices.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.