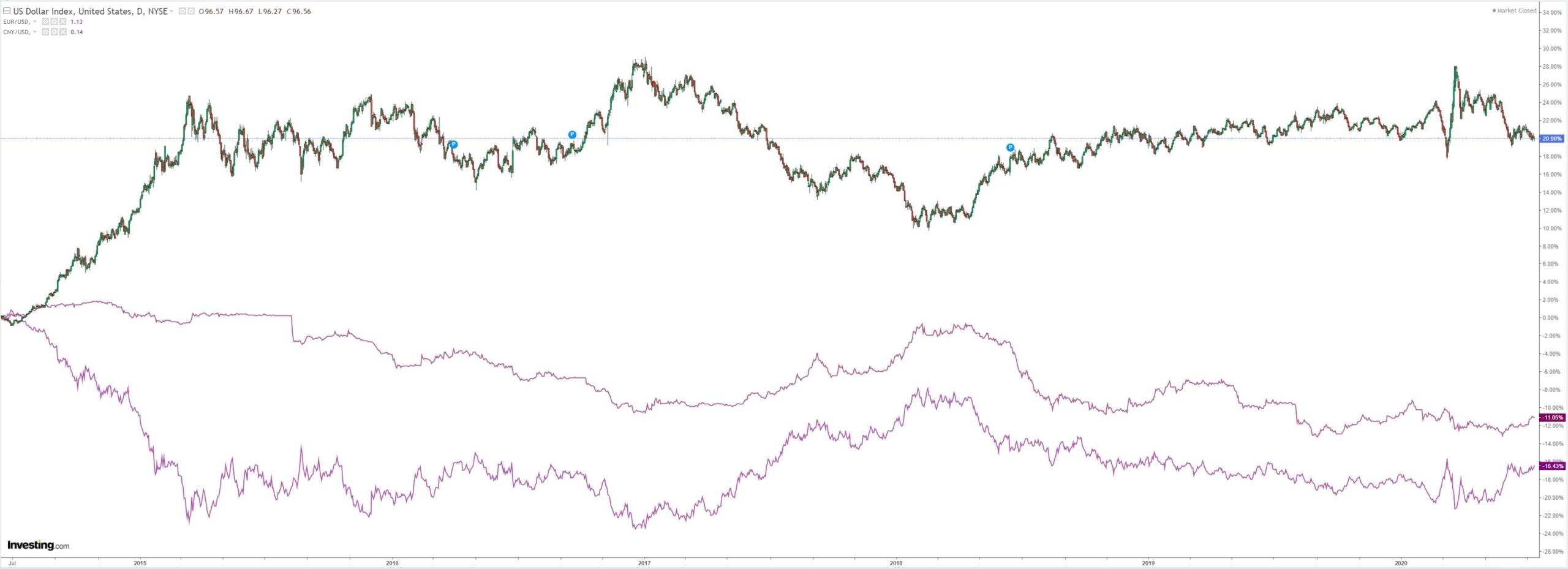

DXY was stable last night:

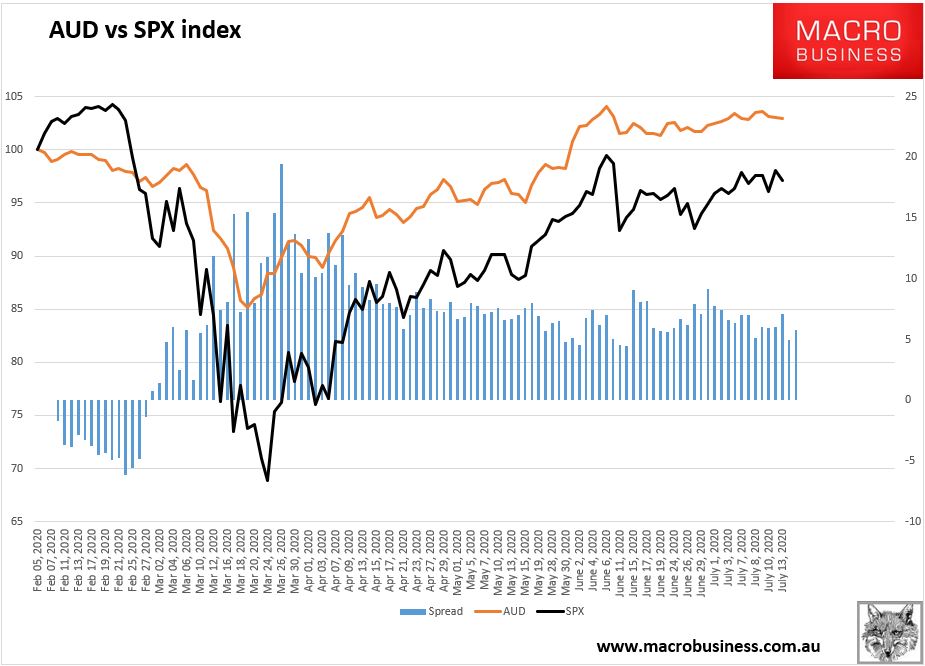

The Australian dollar fell against DMs:

Did better versus EMs:

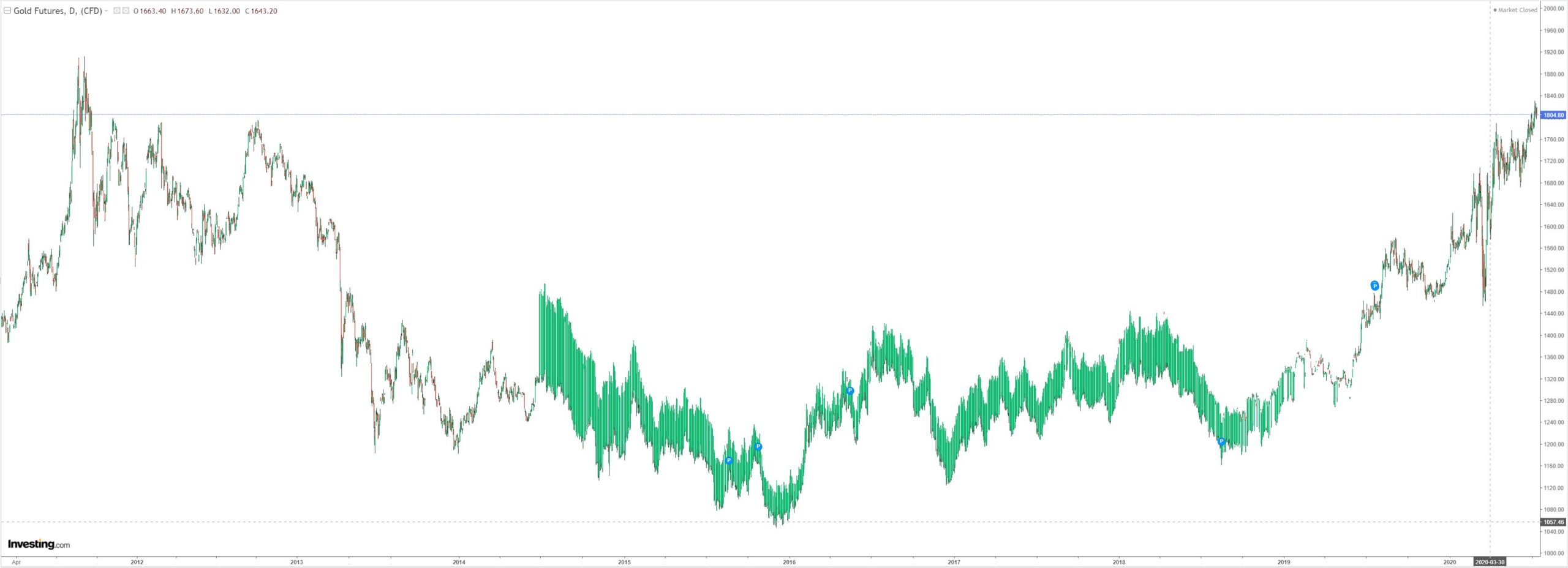

Gold held $1800:

Is oil rolling over?

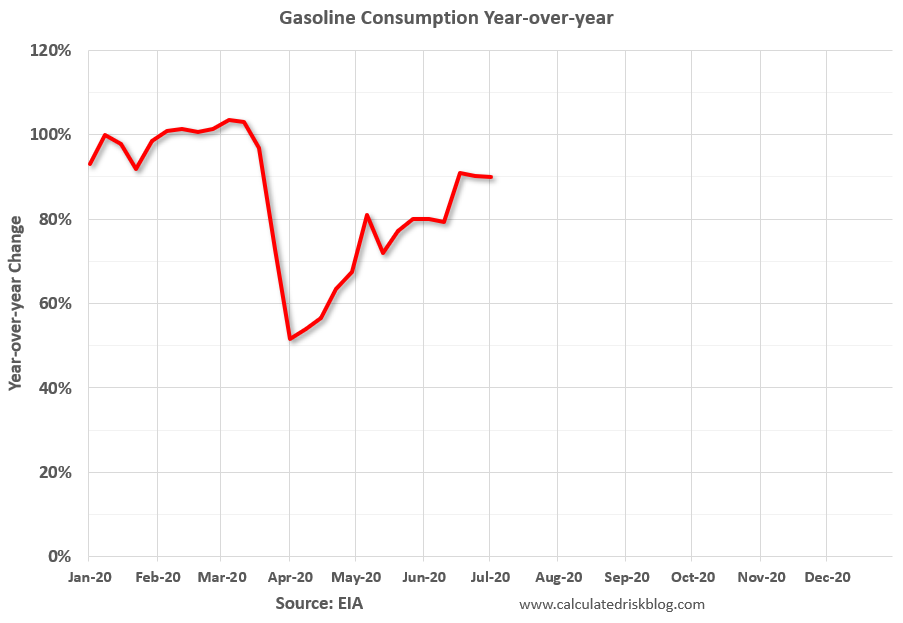

Dirt sure ain’t:

Miners were soft:

EM stocks were hit:

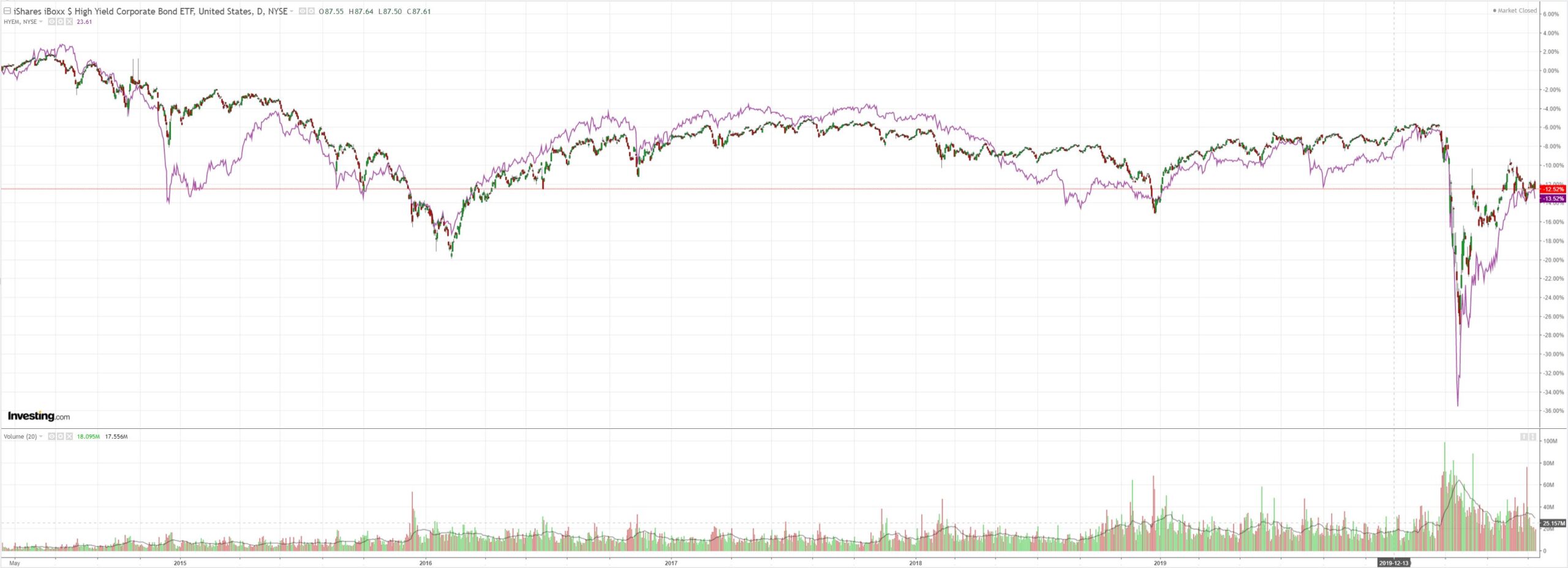

Junk too:

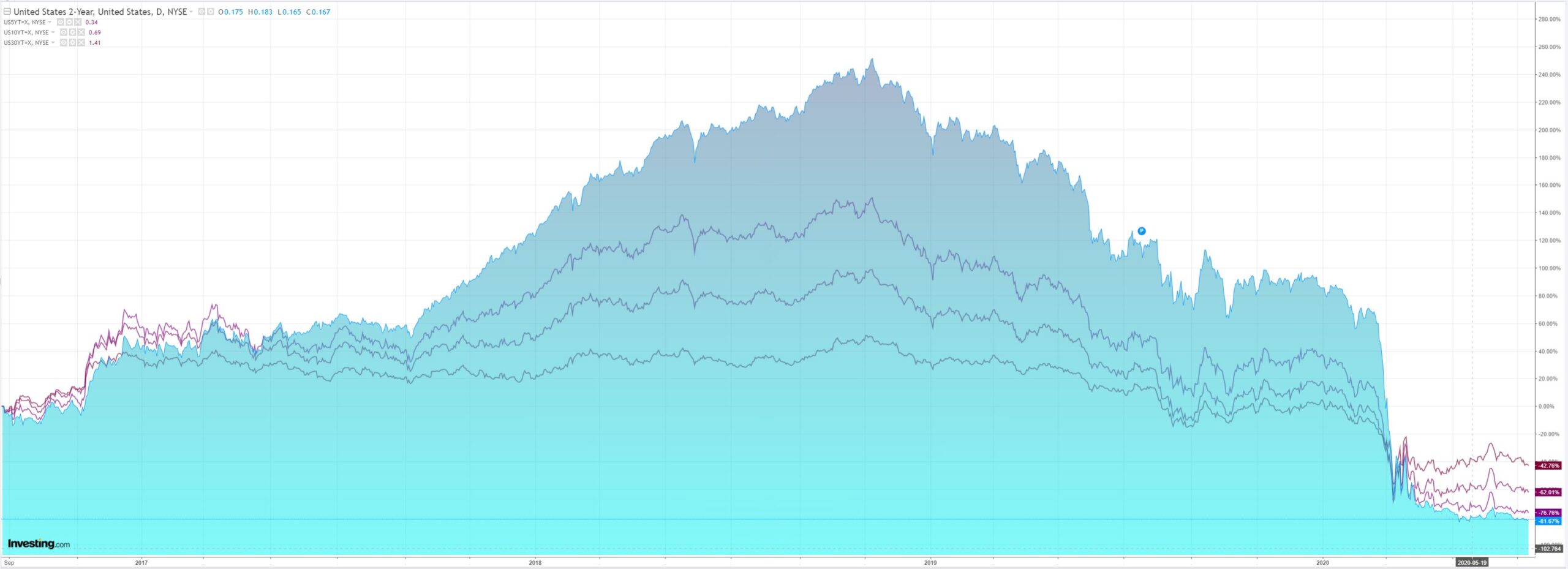

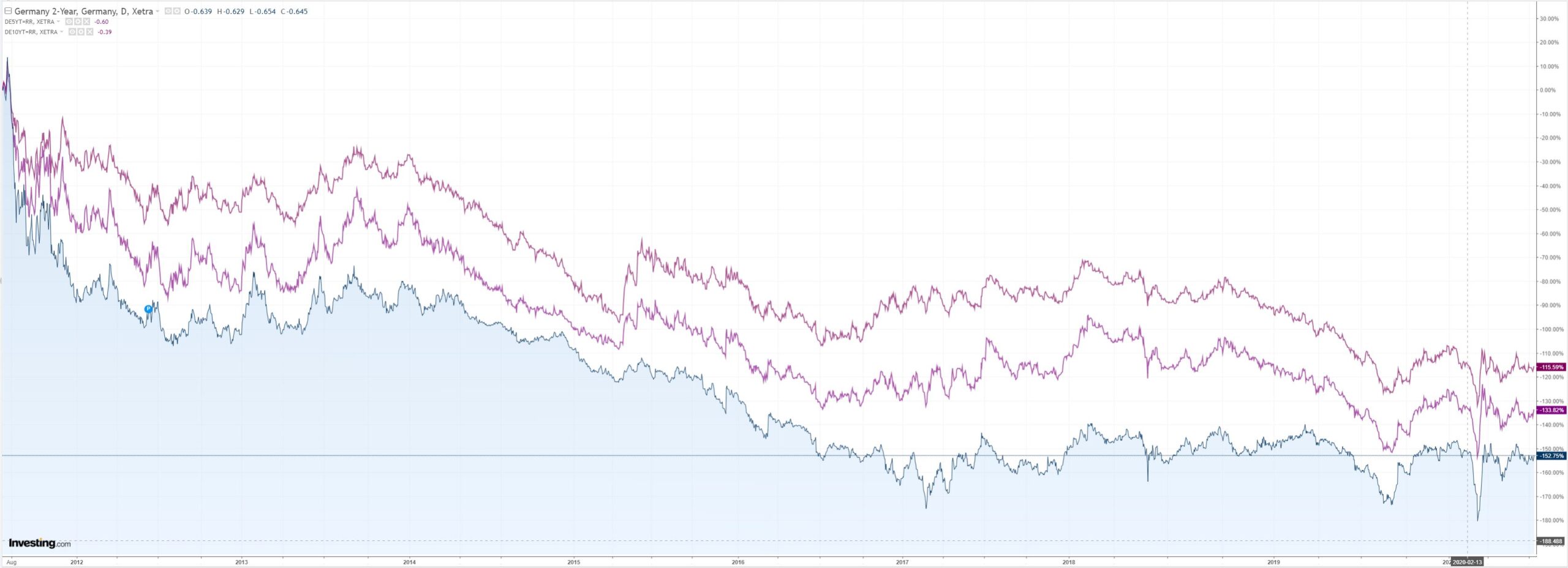

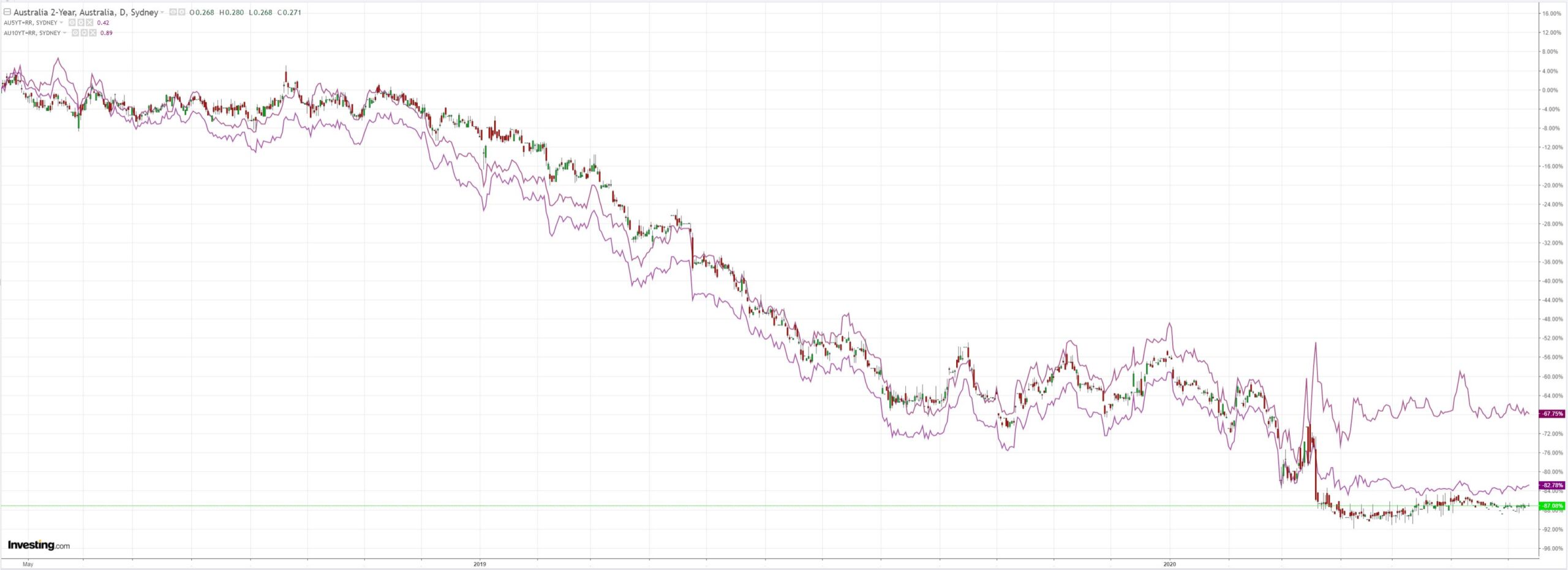

Bonds rallied. The US curve is flattening:

Stocks fell sharply:

The only chart that matters remained in control:

Westpac has the wrap:

Event Wrap

The US Treasury posted a $864.1bn deficit in June – a new monthly record. In June 2019 it was -$8.5 bn shortfall last year.

The FOMC’s Kaplan continued to argue for more fiscal support, and added the Fed may need to do more. He said the resurgence of the virus is muting the recovery in the economy this quarter, and he expects the economy to shrink -4.5% to -5.0% by the end of the year.

Merkel and Conte ended a pre-EC Summit meeting (starts Friday) stating how difficult it will be to gain agreement on the proposed Recovery Fund given the scale of differences .

Event Outlook

Australia: Following a 10pt improvement to -24 in May’s NAB business sentiment survey, the pace of decline is set to ease further in June. ATO/ABS weekly payroll data for the week ending 27 June has been stable in recent weeks, but is still down 6.4% from pre-COVID levels (prior: 0.0%).

New Zealand: June REINZ house sales and prices will edge higher as the lockdown ends, but low confidence will act as a material headwind going forward (prior: -46.6%yr and 7.9%yr, respectively). Net migration in May will reflect the influx of returning NZ citizens while international arrivals remain barred from entry for the time being (prior: 220).

China: The market expects the trade surplus to narrow slightly from $62.9bn to $57.4bn in June.

Europe: Industrial production is headed for a massive resurgence, from -17.1% in April to +15.0% in May. The June ZEW survey of expectations will reinforce the broader recovery trend (prior: 58.6).

Germany: The final estimate for June CPI inflation of 0.6% will confirm modest services inflation.

UK: The market expects a major reversal in the trade balance, from a surplus of GBP305m to a deficit -GBP635m.

US: The July NFIB small business optimism survey will capture rising sentiment and businesses kick starting the rehiring process (prior: 94.4, market f/c: 97.5). The market anticipates a rebound in core and headline CPI inflation in June of 0.5% on energy prices (prior: -0.1%). FOMC’s Brainard (04:00 AEST) and Bullard (04:30 AEST) will speak.

Not much of interest there.

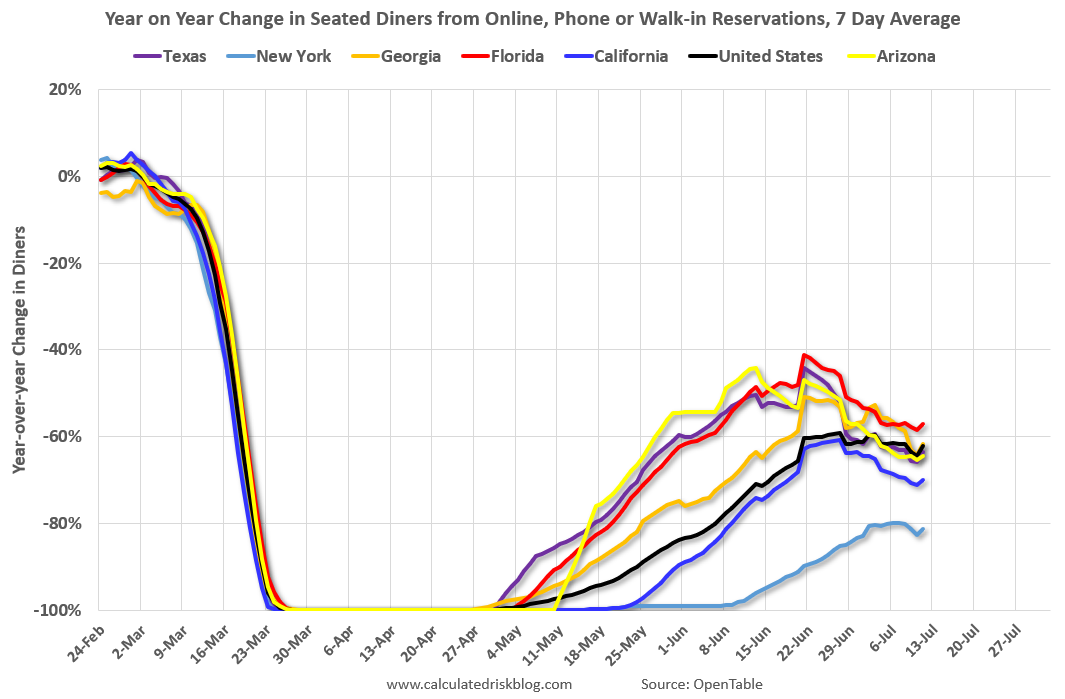

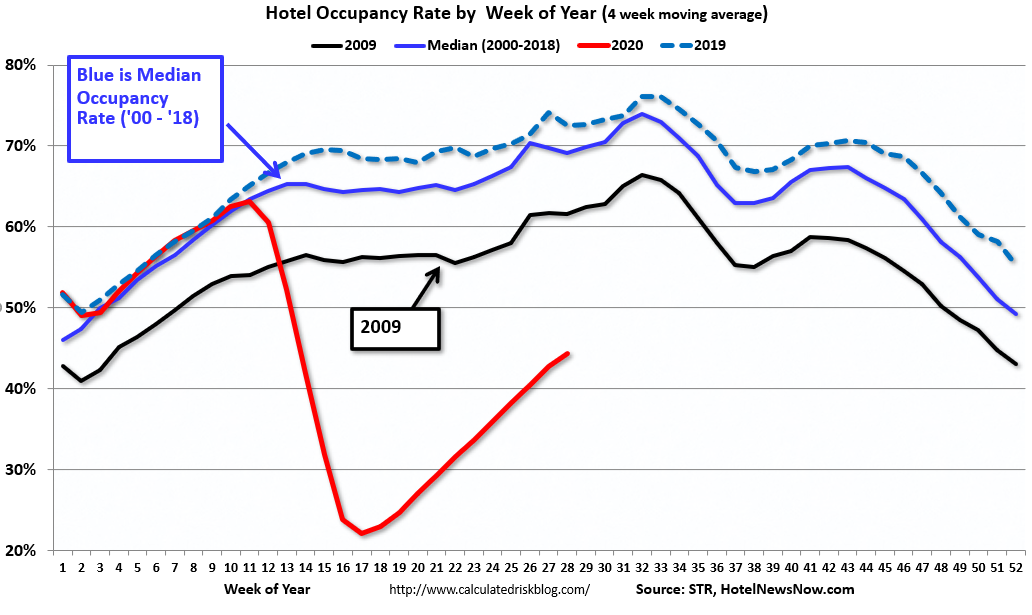

As US virus cases mount higher and deaths rise again too, California closed restaurants, wineries, theaters, family entertainment, zoos, museums and cardrooms. Oregon rolled back opening and Texas mulled the same. There is more to come and high-frequency indicators have well and truly rolled:

Or maybe it’s just this:

MOAR needed or stocks and the AUD are buggered!