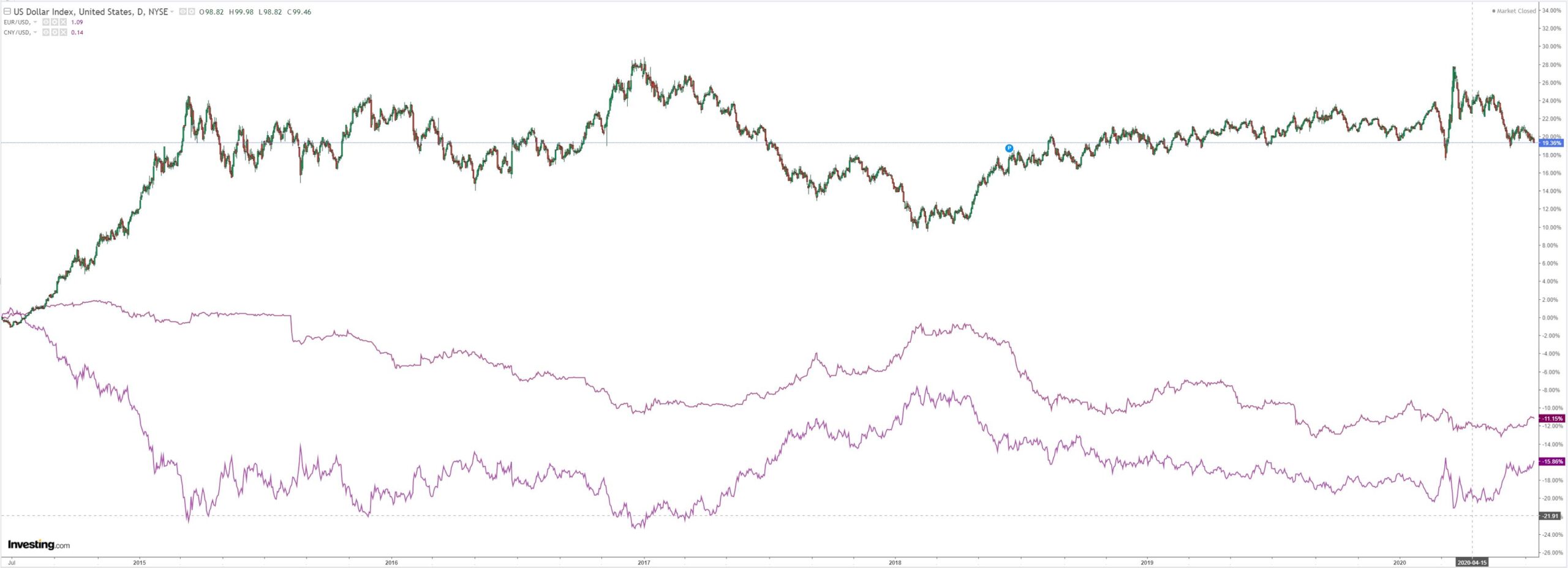

DXY was soft again last night:

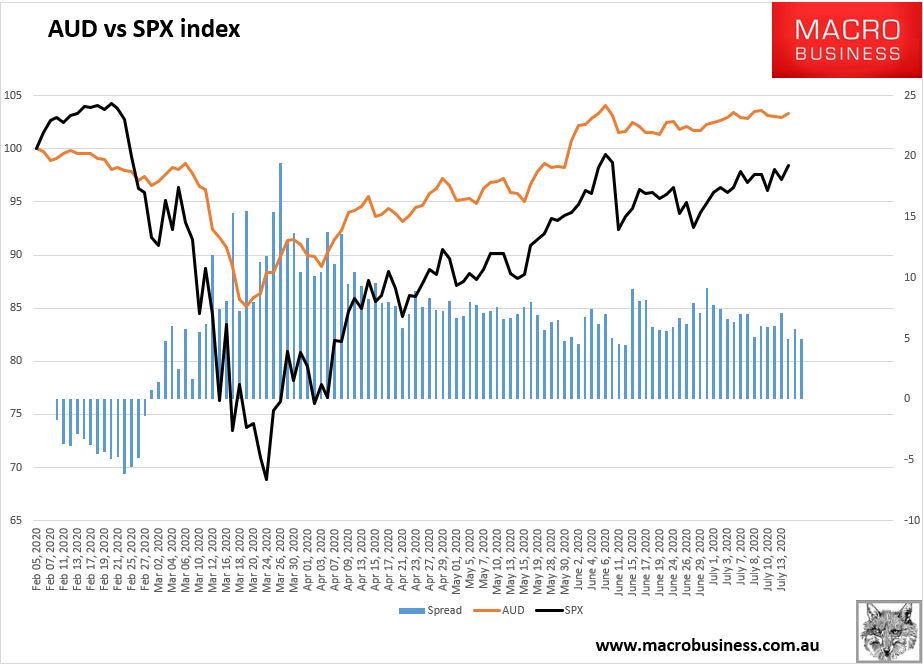

The Australian dollar was firm against DMs:

EMs did better:

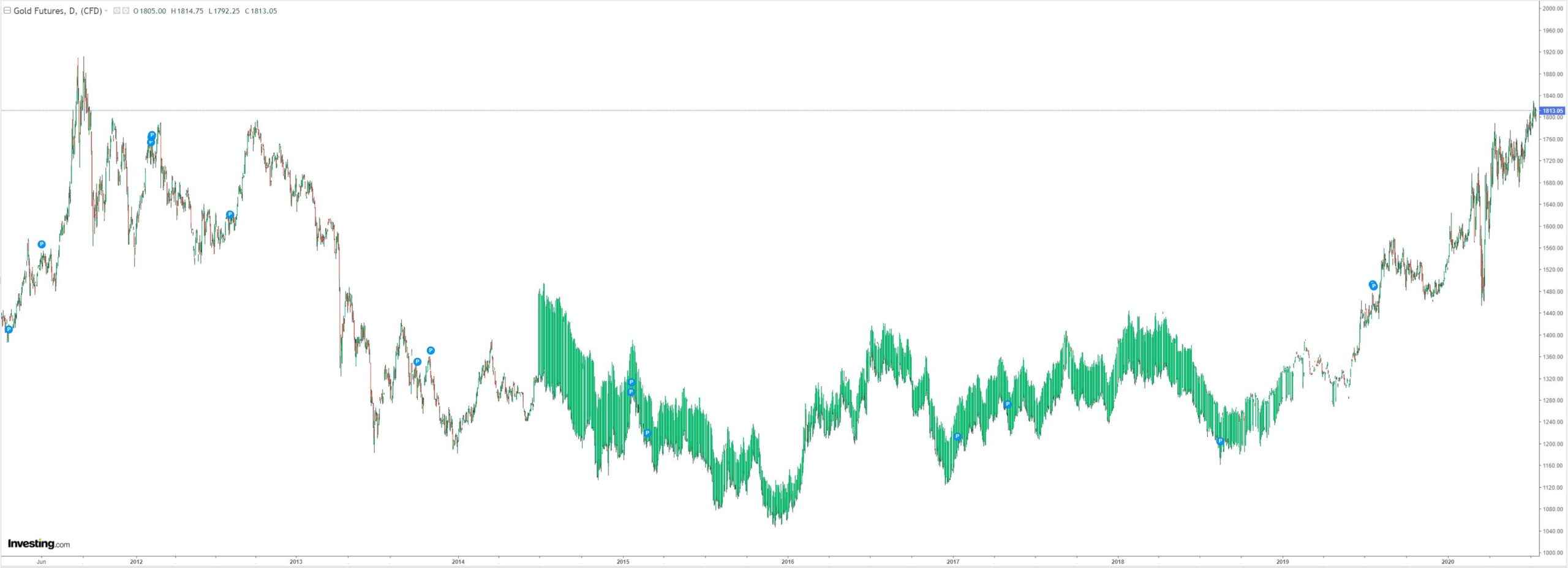

Gold bulled higher again:

Oil held on:

Dirt flamed out:

Miners to the moon:

EM stocks not so much:

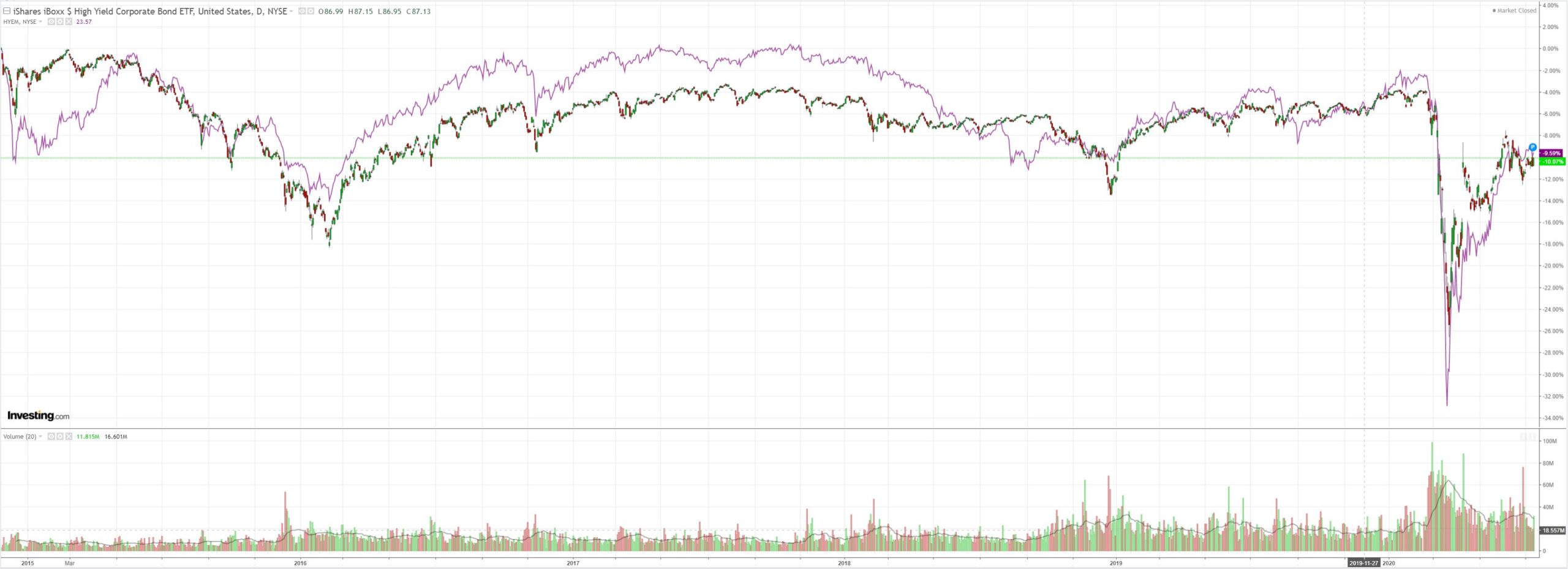

Junk bounced:

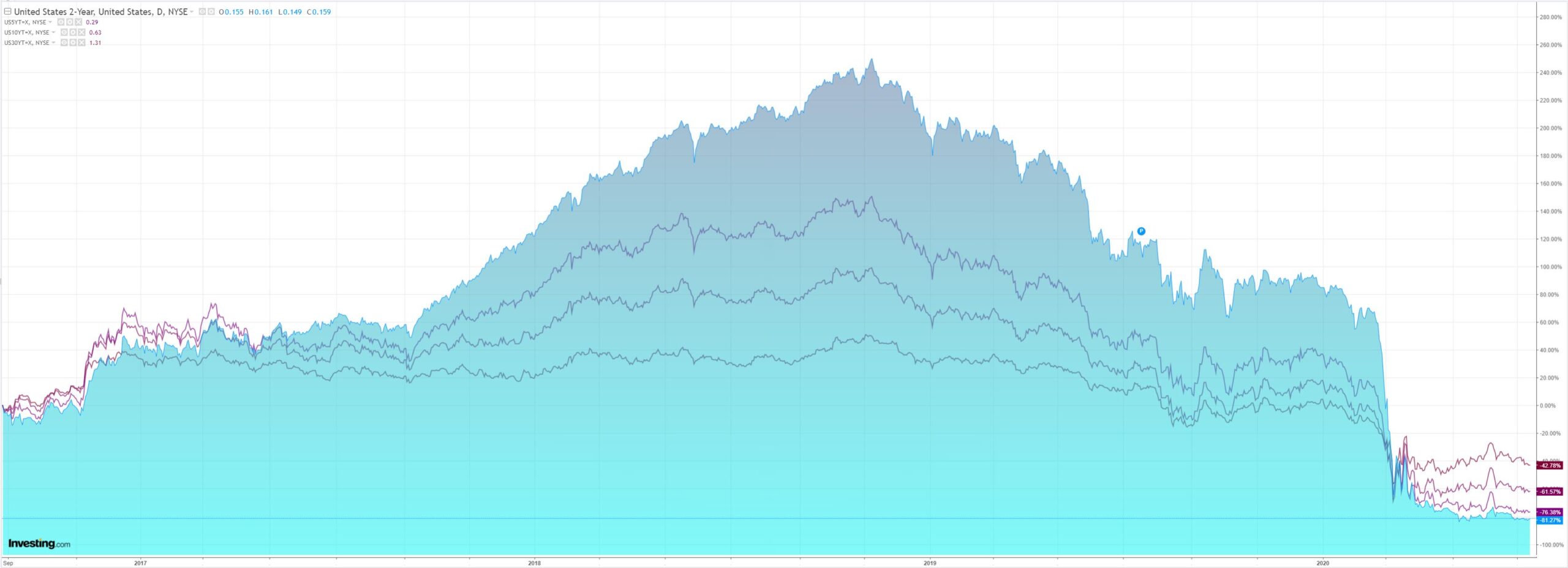

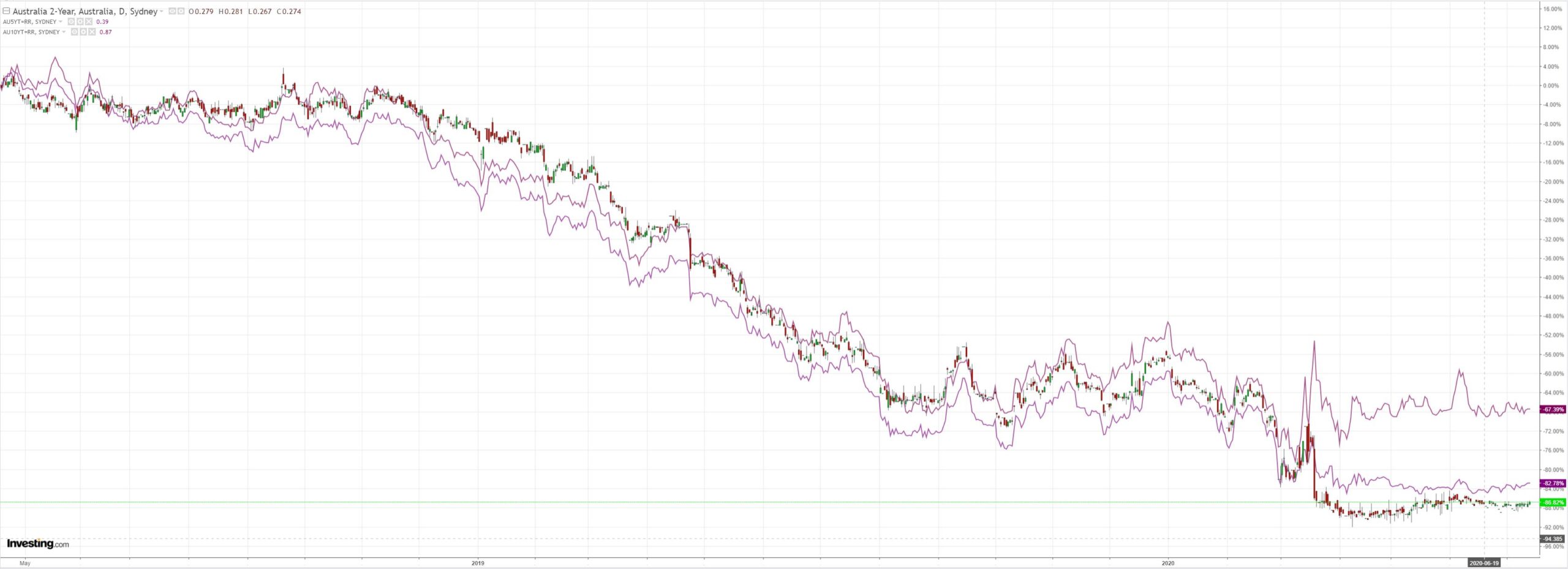

Yield curve control is all the rage:

Stocks took off again:

Westpac has the wrap:

Event Wrap

US June CPI inflation was slightly above estimates (0.6% vs 0.5% est) but remained benign. Headline of +0.6%y/y was as expected, while core CPI at 1.2% y/y beat estimates by +0.1%.

FOMC member Brainard called on the Fed to do more to support the economy, saying monetary policy “will have to shift from stabilization to accommodation,” with balance sheet policies helping extend accommodation. She also suggested yield curve control could help, though it will require additional analysis and discussion. She noted that some high frequency data “suggest that the strong pace of improvement in May and the first half of June may not be sustained.”

Bank earnings: JP Morgan and Citigroup slightly beat estimates on the back of strong trading performances, while Wells Fargo disappointed with its first quarterly loss since 2008.

Eurozone May industrial production rebounded +12.4%m/m (vs estimate of +15%m/m, prior -18.2%m/m). Eurozone ZEW July investor surveys were little changed from June. German expectations fell slightly to 59.3 (est. 60) from 63.4 in June, whilst expectations for the Eurozone firmed to 59.6 from 58.6.

UK monthly production data failed to meet expectations. May GDP bounced a mere +1.8%m/m (est. +5.5%m/m, prior -20.3%m/m), manufacturing rebounded (+8.2%m/m, est. +7.8%m/m), services struggled to pick up (+0.9%m/m, est. +4.8%m/m), and both construction (+8.2%m/m, est. +15%m/m) and industrial production (+5.0%m/m, est. +6.5%m/m) missed expectations.

Event Outlook

Australia: Rising COVID cases and the partial lockdown in Victoria will hit WBC-MI consumer sentiment in July (prior: 93.7).

India: May exports climbed off depressed levels to narrow the trade deficit. Consensus estimates suggest a similar reading in June (prior: -$3.15bn, market f/c: -$3.5bn).

UK: Flat CPI inflation reads will persist in the post-COVID recovery (prior and market f/c: 0.0%)

Canada: Both Westpac and the market expect the BoC to keep rates at the lower bound (0.25%) in the face of COVID headwinds.

US: The market anticipates another 1.0% rise in import prices following the advance in May which was driven by higher fuel prices. The July Fed Empire state survey index will likely conform to the positive regional survey trend of late (prior: -0.2, market f/c: 10.0). June industrial production will be released today and likely indicate the bounce in factory output has yet to run its course (prior: 1.4%, market f/c: 4.4%).FOMC’s Harker (02:00 AEST) and Logan (03:30 AEST) will speak before the Federal Reserve’s Beige book is released (04:00 AEST).

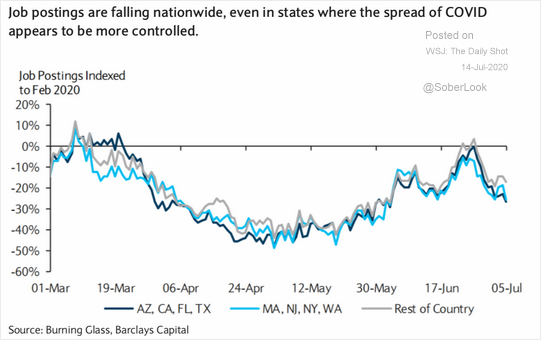

The latest “only chart that matters”:

Let’s pretend for a moment that other relationships matter too. The US is slumping back into viral depression:

Europe, in the other hand, still has the virus under control and forex markets see it as a better option for rebounding growth of the two major currency blocks. There is also some fiscal co-ordination taking away fears of various exits.

For now, that is holding sway with the Euro rebounding driving down DXY. That is an environment in which the Australian dollar will be biased upwards.

Until the only chart that matters implodes.