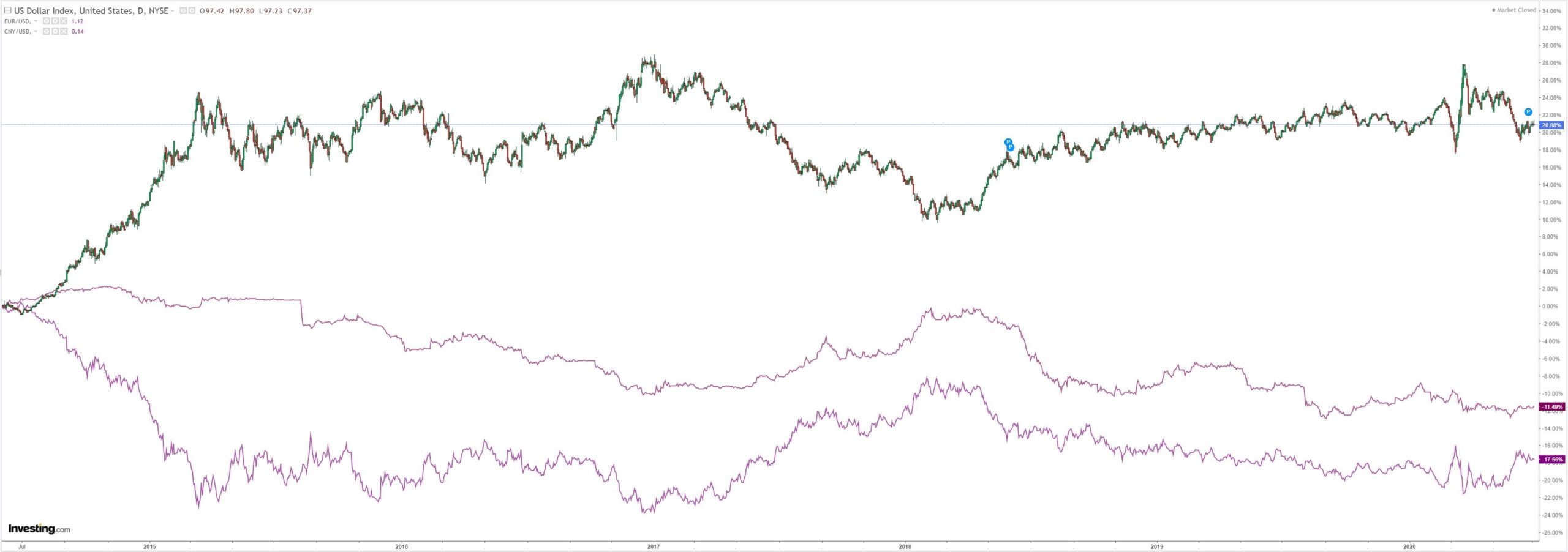

DXY was softish last night:

The Australian dollar rose against everything:

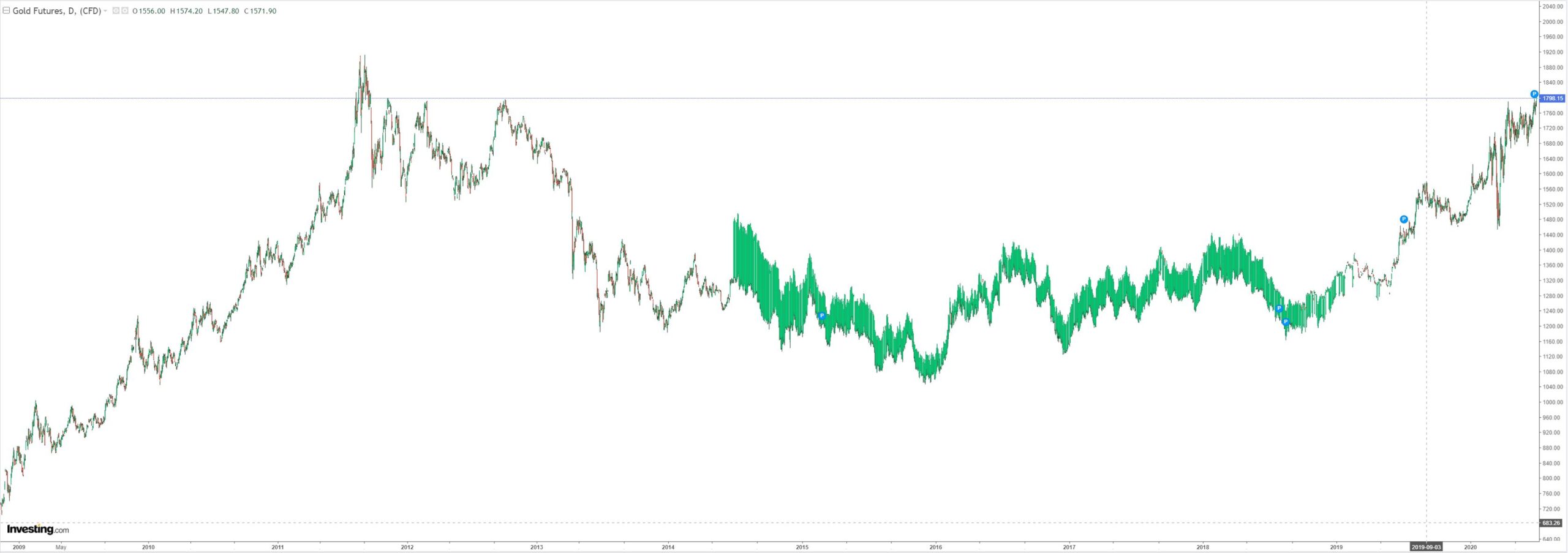

Gold put some light between it and the break out:

Oil was soft:

Dirt mixed:

Miners firm:

EM stocks weak:

Junk better

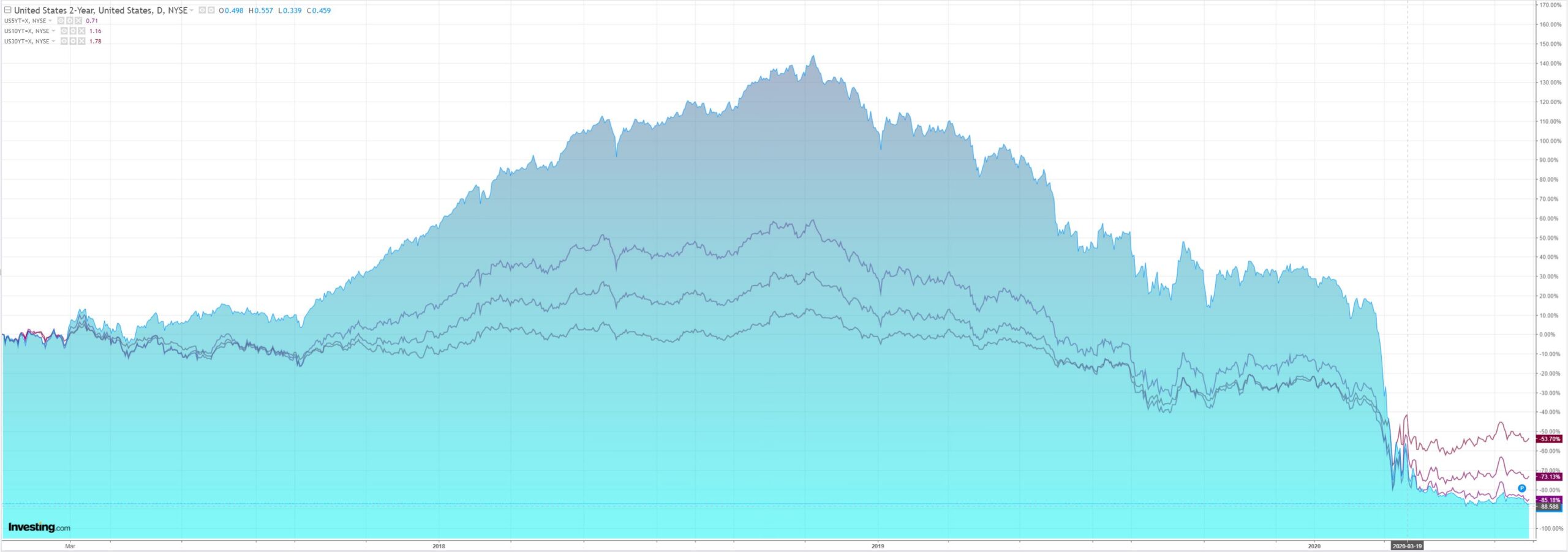

Bonds were soft:

Stocks took off for year end:

Westpac has the wrap:

Event Wrap

US infectious disease expert and senior official Fauci told a Senate panel that the US is “going in the wrong direction” in its efforts to contain Covid, and that daily cases could rise from 40,000 currently to 100,000 if behaviours don’t change (citing crowded indoor bars, as an example).

Fed Chair Powell said the economy’s path forward is “extraordinarily uncertain and will depend in large part on our success in containing the virus,” in his prepared testimony. And he reiterated that “a full recovery is unlikely until people are confident that it is safe to reengage in a broad range of activities.” He did note that incoming data were reflecting a resumption in activity, though he noted the challenges in keeping the virus in check amid the re-openings. He concluded the testimony by reiterating that the Fed is “committed to using our full range of tools to support the economy and to help assure that the recovery from this difficult period will be as robust as possible.”

FOMC member Williams said that no decision has been made on yield curve control. On negative rates, he said they weren’t appropriate for the current circumstances, and that he and other Fed officials don’t believe they would be effective.

US Conference Board consumer confidence beat estimates (of 91.4) with a rise to 98.1 (prior 85.9), but it remains well below its heady pre-COVID levels above 125. Chicago Fed PMI disappointed as it merely “edged up to 36.6 in June” (est. was 45, prior 32.3).

Eurozone June CPI was in line with expectations following a beat in Germany and a miss in France. Headline CPI rose +0.3%y/y (est. +0.2%) and core CPI rose +0.8%y/y (as est.).

UK final 1Q GDP was marked lower to -2.2%q/q (initial -2.0%), reflecting weaker private (-2.9%, initial -1.7%) and government consumption (-4.1%, initial -2.6%), as well as weaker trade and investment. BoE Chief Economist Haldane maintained his more hawkish tone (the lone dissenter in the MPC) and did not focus on weakness in the economy but on the potential of a V-shaped recovery and positive high frequency data (despite the high levels of uncertainty). He played down the potential of NIRP although keeping all options on the table.

Event Outlook

Australia: The Corelogic home price index is expected to continue its correction in June, falling 0.7% after a 0.5% decline in May. May dwelling approvals are expected to capture the full COVID-19 impact; the market forecasts a 7.8% decline, Westpac -10.0% (prior: -1.8%).

New Zealand: Westpac anticipates May building consents will show signs of catch-up activity following the relaxation of containment measures (prior: -6.5%, Westpac: 14.0%).

Japan: A severe hit to the Q2 Tankan large manufactures index has been priced in by the market. It is predicted to fall from -8 to -31, marking a sixth quarter of declines as business sentiment and exports plummet.

Asia: A raft of manufacturing PMI data will be released for Malaysia, Indonesia, South Korea, Taiwan and India.

China: Last month saw the Caixin manufacturing PMI cross into positive territory at 50.7. The market expects it to stabilise at this level.

Europe: Markit manufacturing PMIs look promising. Flash results reported a rebound for the Eurozone, UK and Germany.

US: The market continues to expect the worst is over for the US labour market. ADP payrolls are expected to bounce from -2760k to 2850k in June. The Markit manufacturing PMI was last seen hovering just below the expansionary benchmark at 49.6. The market forecasts little change in June. The June ISM manufacturing index is expected to improve to a similar level (prior: 43.1, market f/c: 49.7). The forecast for May construction spending is upbeat at 1.0% after it slumped in April, -2.9%.

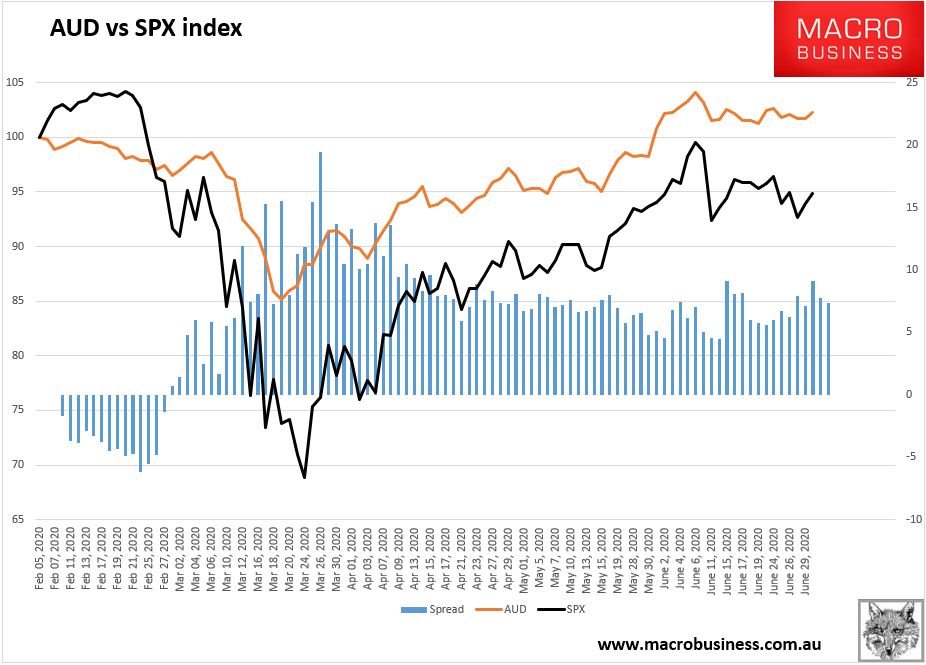

The AUD was correcting solidly last night after the VIC lockdowns but the AUD/SPX is still all that matters and it was up so end of story: