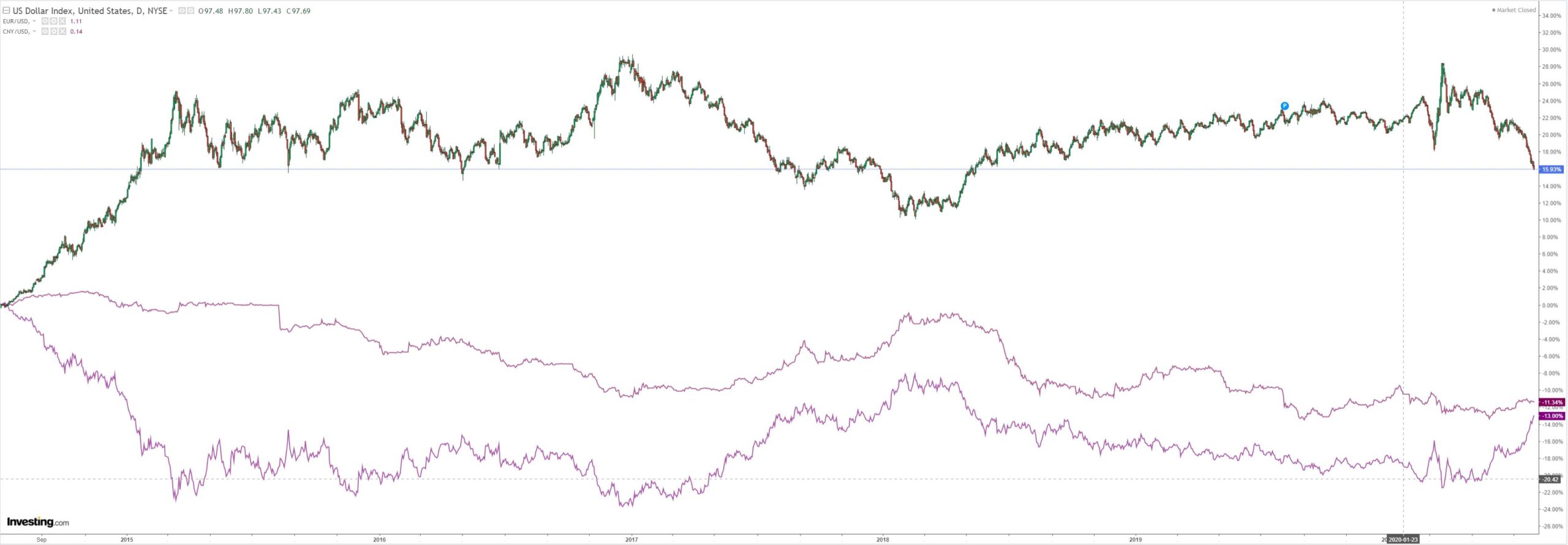

It’s swift becoming a DXY tank for the ages. EUR is out of control. Germany must be ruing eurobonds already. CNY is riding DXY coattails down in its usual evil supply-side grab:

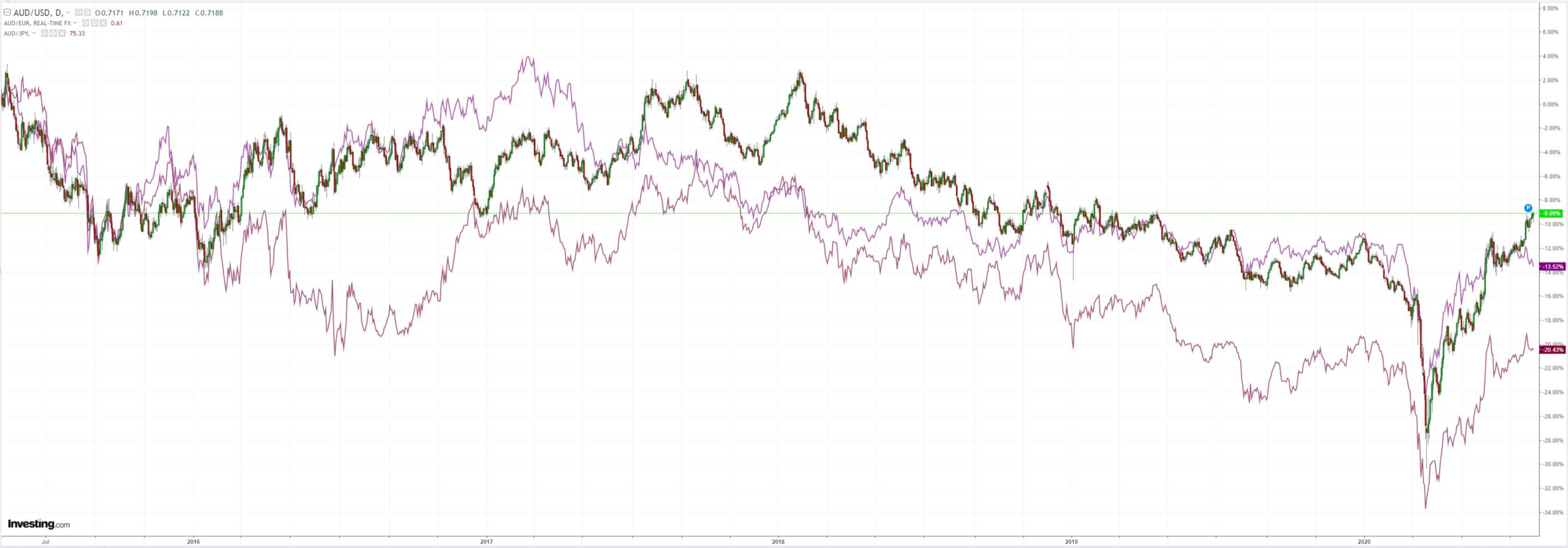

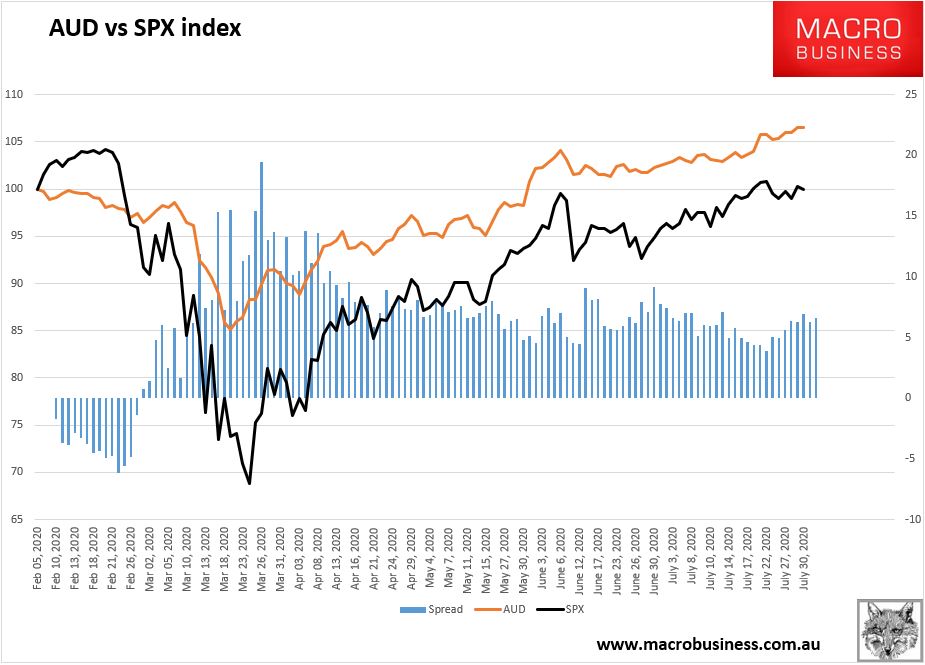

Nobody should be cheering the AUD. We’ve been pivoting to EU for our offshore hedge:

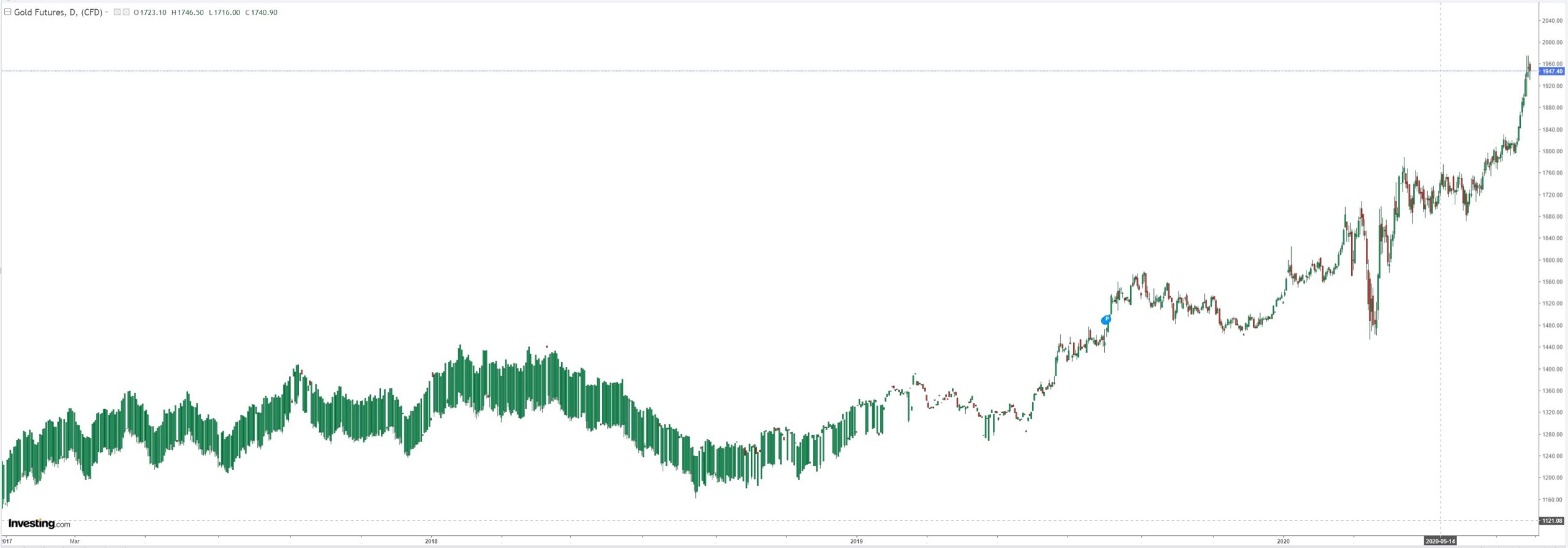

Gold is consolidating after its run:

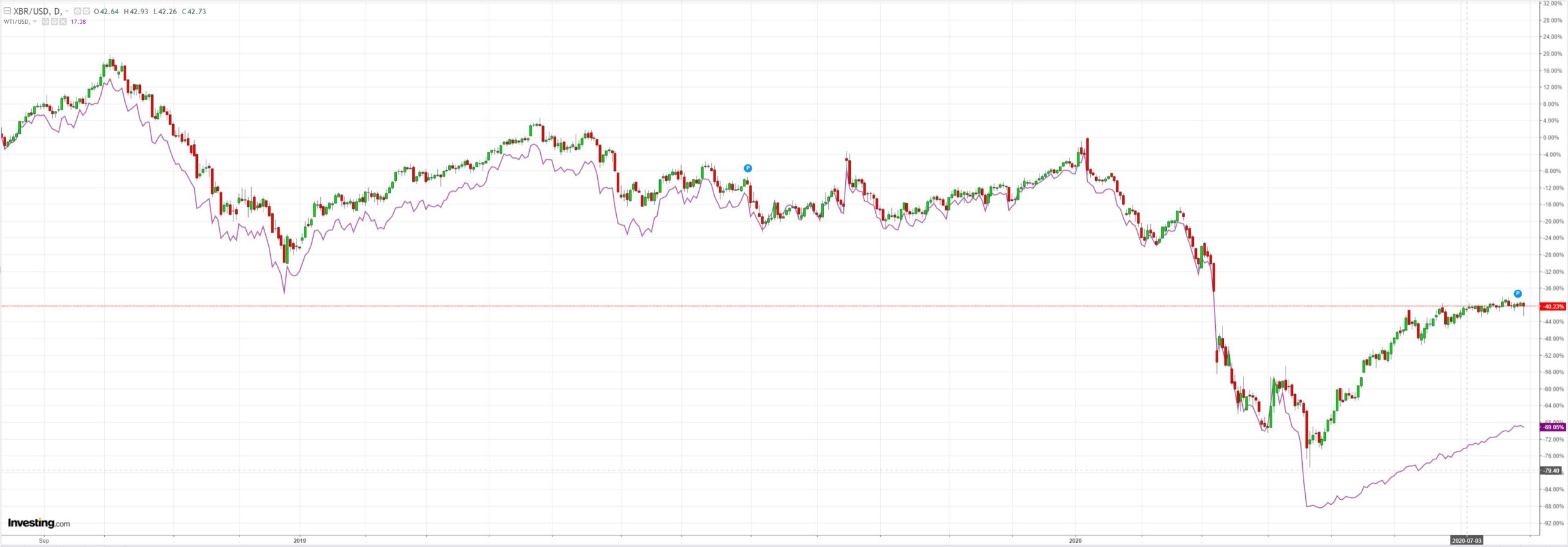

Oil was hit:

Dirt too:

And miners. All profit-taking I’d say:

EM stocks are poised:

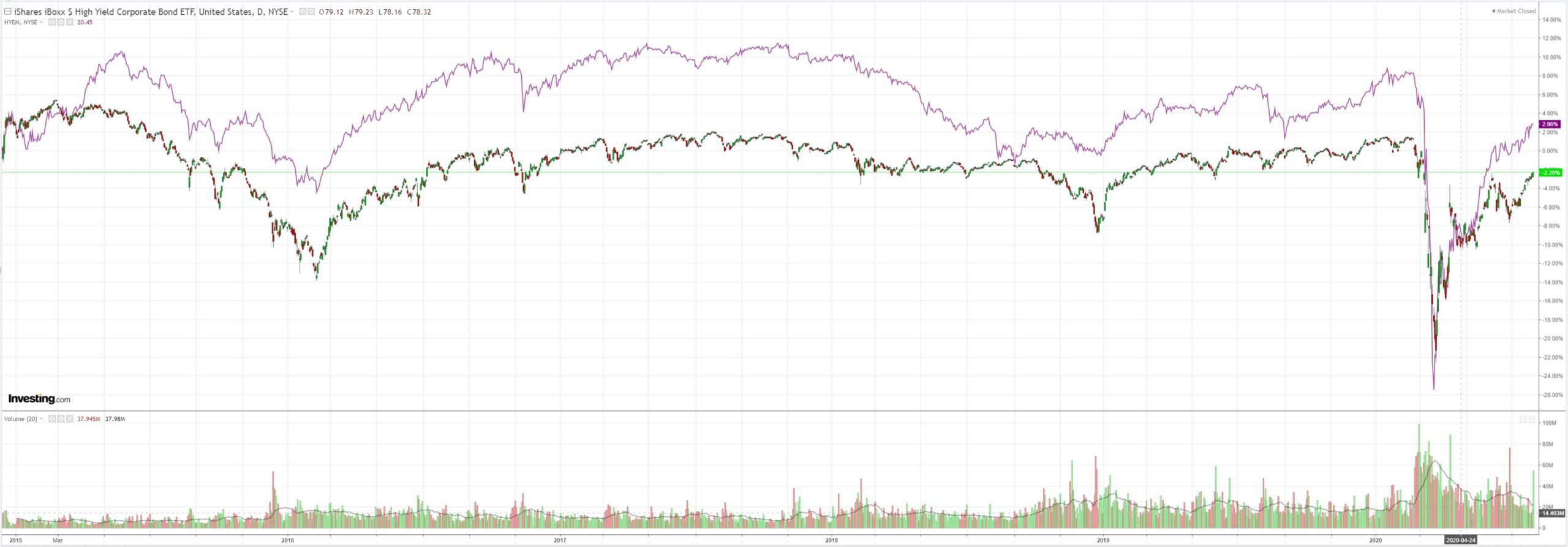

Junk on the march:

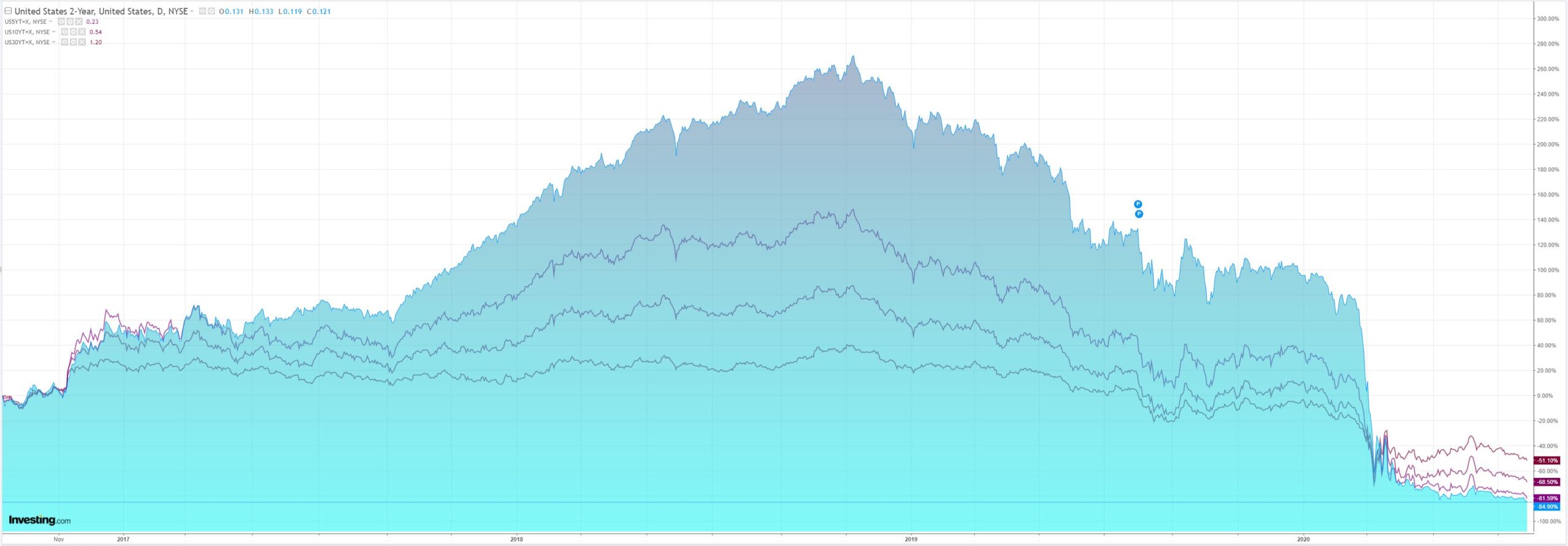

Yields smashed:

Stocks were soft. EUR is going to crush Continental bourses:

The only chart that matters soldiers on:

Westpac has the wrap:

Event Wrap

US Q2 GDP fell a record -32.9%q/q annualised (vs median estimate -34.5%). Core PCE growth fell to -1.1% (prior +1.6%). A sharp fall in personal spending was slightly offset by net exports and government spending. Perhaps of more concern was the rise in continuing jobless claims to 17.0m (vs 16.2m estimate and prior) as the impact of persistent COVID cases started to impede employment. Initial jobless claims were close to expectations at 1.4m.

German Q2 GDP was soft at -10.1%q/q (vs est. -9%q/q). July CPI fell, at -0.5%m/m and flat y/y (est. -0.2%m/m and +0.3%y/y). German July unemployment surprised with a decline of -18k and a rate of 6.5% (est. +40k and 6.5%) but Eurozone June unemployment reflected weakness in other national releases and rose to 8.8% (est. 8.6%).

Event Outlook

Australia: Private sector credit growth will hover around the previous rate of -0.1% in June, due to a weak housing market and declining business activity (market f/c: -0.1%, Westpac: -0.2%). Falling energy prices will lead to a fall in Q2 PPI growth from 0.2% previously.

New Zealand: ANZ consumer confidence will find firmer ground in July due to the rise in spending (prior: 104.5).

Asia: Factory output is rebounding across the region, with Japan and Korea set to see a material improvement in the June prints; from -8.9% to 1.0% and -6.7% to 2.3% respectively. Taiwan Q2 GDP is vulnerable to downside risks after clinging to growth in Q1 (prior: 1.59%, market f/c: 0.0%).

China: Manufacturing and non-manufacturing PMIs have been robust of late. Broadening growth will support the PMIs in July; from 50.9 to 50.8 and 54.4 to 54.5, respectively.

Eurozone: The bulk of economic pain from COVID-19 will be seen in Q2, with consensus estimates predicting a deterioration in GDP growth from -3.6% to -12.0%. CPI inflation pressures will remain negligible for the foreseeable future (prior: 0.3%, market f/c for July: -0.5%).

US: Personal income fell in May after an initial boost from government handouts. June will see an improvement (prior: -4.2%, market f/c: -0.7%). Personal spending is recovering but remains at risk as states battle the virus (prior: 8.2%, market f/c: 5.3%). The bounce in the June PCE deflator from 0.1% to 0.4% will be the result of energy prices, the core measure remaining at 1.0%y/y. Soft wages growth will be a lasting consequence of COVID-19, with growth in the employment cost index set to moderate from 0.8% to 0.6% in Q2.

With DXY so high still, and collapsing at spectacular speed, the AUD rocket is not finished.