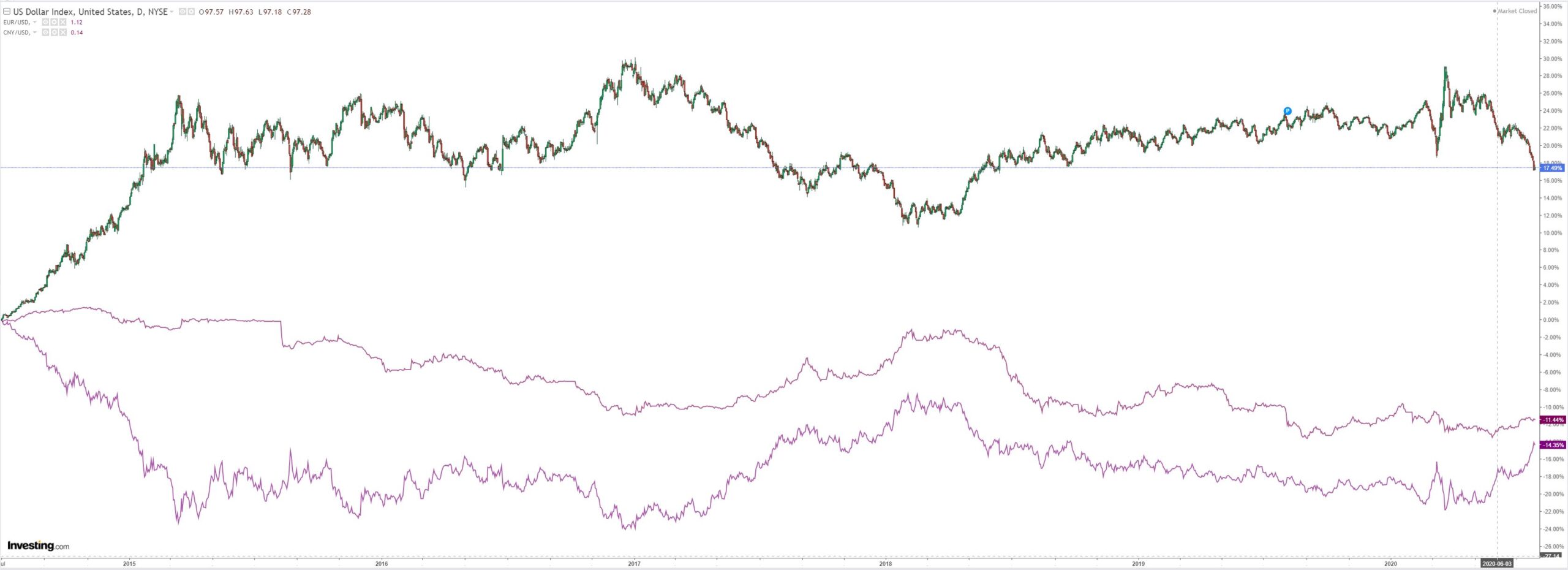

Nasdaq looks toppy as S&P fights for support. Europe is stuffed by its rising currency:

Advertisement

Westpac has the wrap:

Event Wrap

The US Federal Reserve announced an extension of most of its emergency lending measures, which were due to expire around 30 September, until year end, with the exception of their Commercial Paper Funding Facility extended to March 2021. “The three-month extension will facilitate planning by potential facility participants and provide certainty that the facilities will continue to be available to help the economy recover from the Covid-19 pandemic,” the Fed statement said. Since mid-March, the Fed has started nine emergency programs aimed at pumping liquidity into short-term credit markets and extending credit to businesses and local governments affected by the economic fallout from COVID.

US Conference Board July consumer confidence expectations component fell from 106.1 to 91.5, dragging down the headline to 92.6 (prior 98.3, est. 95.0). The decline in expectations indicates the rise in US COVID cases is unsettling confidence more broadly which is likely to be apparent in August surveys. Richmond Fed July manufacturing survey rose to 10 (est. 5, prior zero) but once again the wide range of estimates really meant that this was within the market’s expectations.

UK’s CBI (business body) July retail sales managed to beat gloomy expectations, with a rebound in overall activity led by essential purchases. The headline index rose to +4 from -37 in June (ave. est. -25). However, optimism over future sales remains soft.

Event Outlook

Australia: Plunging fuel prices and free childcare are set to jolt headline CPI inflation in Q2, the market and Westpac expecting a record quarterly decline of -2.0%qtr and -2.4%qtr respectively (prior: +0.3%qtr). The trimmed mean should see a more modest, but still likely negative, outcome (prior: 0.5%qtr, market f/c:-0.1%qtr, Westpac: -0.2%qtr).

Hong Kong: Q2 GDP is expected to show back-to-back contractions following Q1’s growth hit (prior: -8.9%, market f/c: -8.2%)

US: A record decline in May wholesale inventories of -1.2% has primed the market to expect another negative reading in June of -0.5%. June pending home sales are meanwhile set to confirm the bounce back in real estate volumes following May’s colossal jump of 44.3% (market f/c: 15.0%). The FOMC is expected to hold fire in July, but participants will be watching the post-meeting press conference closely for comment on risks and monetary/ fiscal options for further easing (04:30 AEST).

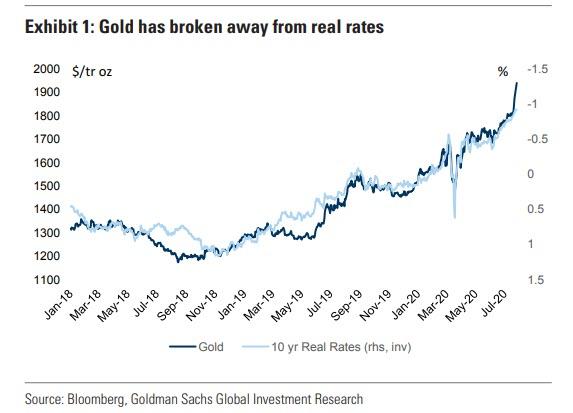

Goldman chimed in with more gold bullishness:

Advertisement

…real concerns around the longevity of the US dollar as a reserve currency have started to emerge.

…[we have] long maintained gold is the currency of last resort, particularly in an environment like the current one where governments are debasing their fiat currencies and pushing real interest rates to all-time lows, with the US 10-year TIPs at -92bp is 5bp below the 2012 lows.

…with more downside expected in US real interest rates we are once again reiterating our long gold recommendation from March and are raising our 12-month gold and silver price forecasts to $2300/toz and $30/toz respectively from $2000/toz and $22/toz.

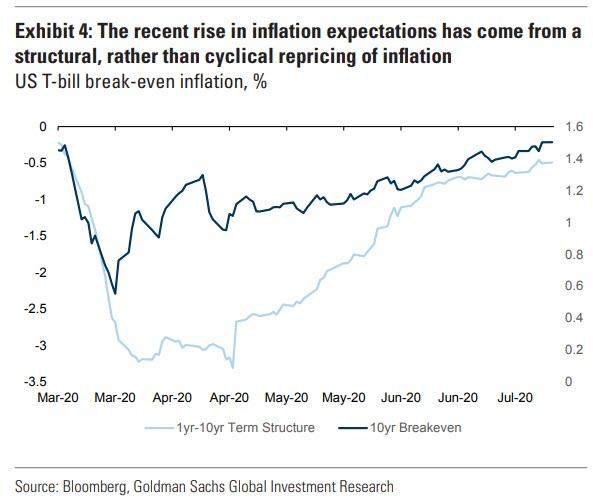

This relentless decline in real interest rates against nominal rates bounded by the US Fed has caused inflation breakevens to rise (see Exhibit 3) in an environment that would ordinarily be viewed as deflationary, i.e. a weakening US labor market as the country re-enters lockdown.

The deflationary shock caused by the pandemic drives the need to expand balance sheets to support demand today, as seen in the latest US $1.0 trillion Phase 4 stimulus and the €750 billion pan-EU recovery fund. The resulting expanded balance sheets and vast money creation spurs debasement fears which, in turn, create a greater likelihood that at some time in the future, after economic activity has normalized, there will be incentives for central banks and governments to allow inflation to drift higher to reduce the accumulated debt burden.

…asset managers have real concerns today about persistent unanticipated shifts in inflation that can create large discrepancies between current expected real returns and actual realized returns.

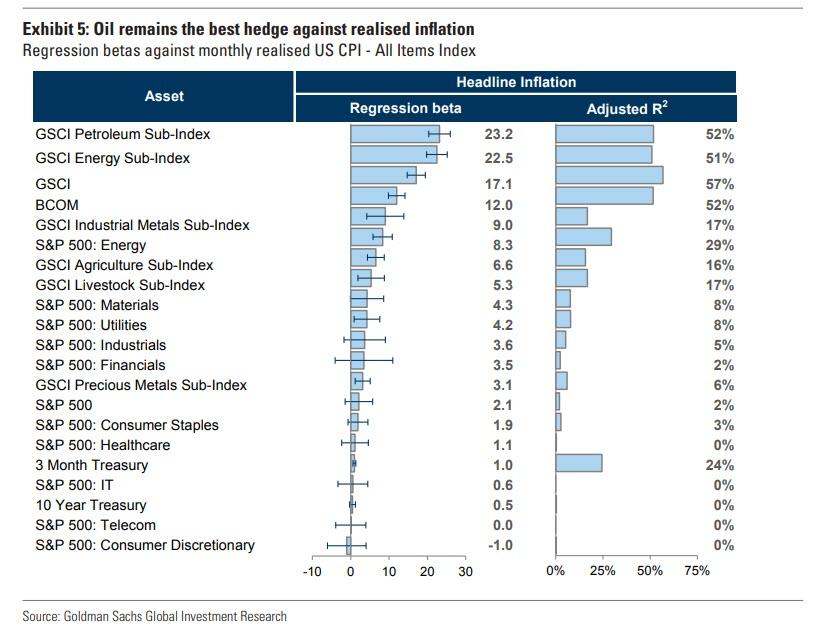

The key point from a hedging perspective is that asset managers care about the level of inflation, not the changes in inflation, and from a level perspective, inflation hedges like commodities and equities are likely far cheaper today than in the future when inflation could arrive. When discussing the drivers of investment demand for gold and commodities, it is important to distinguish between debasement and inflation. The key is that the current debasement and debt accumulation sows the seeds for future inflationary risks despite inflationary risks remaining low today. While debasement in many cases leads to inflation, it is not always the case as witnessed over the past decade. Equally, the best debasement hedge (gold) is not always the best hedge against inflation (oil). Indeed, the word debasement comes from adding base metals like tin or copper to the precious metals that acted as hard currency; therefore, owning the pure precious metal is then the best hedge against debasement.

…today the risk is from debasement of fiat currencies that sows the risk for inflation and gold is the best hedge against debasement. Further out as inflation risks rise, oil and equities hedge unexpected and expected inflation respectively better than gold (see Exhibit 5), and given the size of the bond portfolios built over the past decade that will need to be hedged against inflation risks, the sheer size of investment demand for commodities is likely to be massive, underscoring the need to act today.

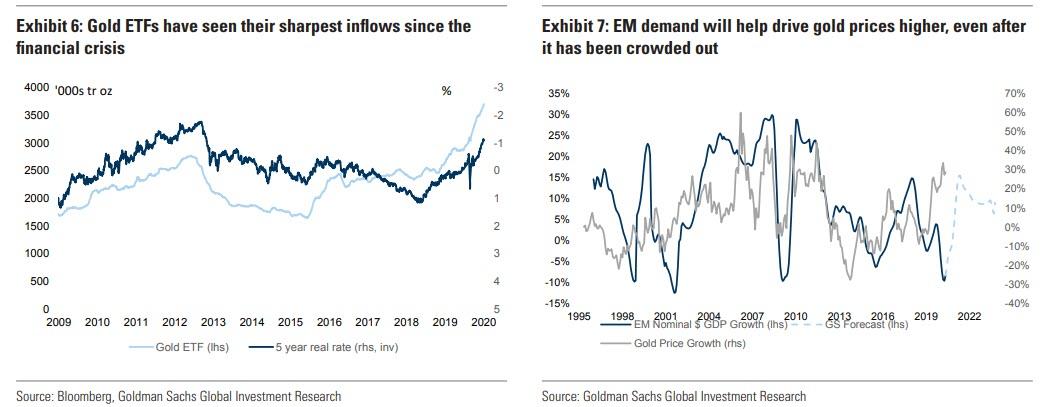

DM investment demand strength has continued with ETF additions in both Europe and US running high (see Exhibit 6). We see this trend persisting for some time as investment allocations into gold increase inline with allocations to inflation-protected assets, similar to what happened after the financial crisis. Following the GFC, inflation fears peaked only at the end of 2011 as the bounce back in inflation ran out of steam, bringing the gold bull market to a halt. Similarly, we see inflationary concerns continuing to rise well into the economic recovery, sustaining hedging inflows into gold ETFs alongside the structural weakening of the dollar, we see gold being used as a dollar hedge by fund managers. Indeed, decomposing our gold forecast, with returns of 18% over the next 12 months, we estimate 9% of the growth is driven by 5yr real rates going to -2% over the next 12 month, (an est. elasticity of 0.1), while the second 9% comes from the 15% increase in the EM dollar GDP (an est. elasticity of 0.5) (see Exhibit 7).

…the stretched valuations in equities, low real rates and high level of economic and political uncertainty all point toward continued inflows by high net worth individuals.

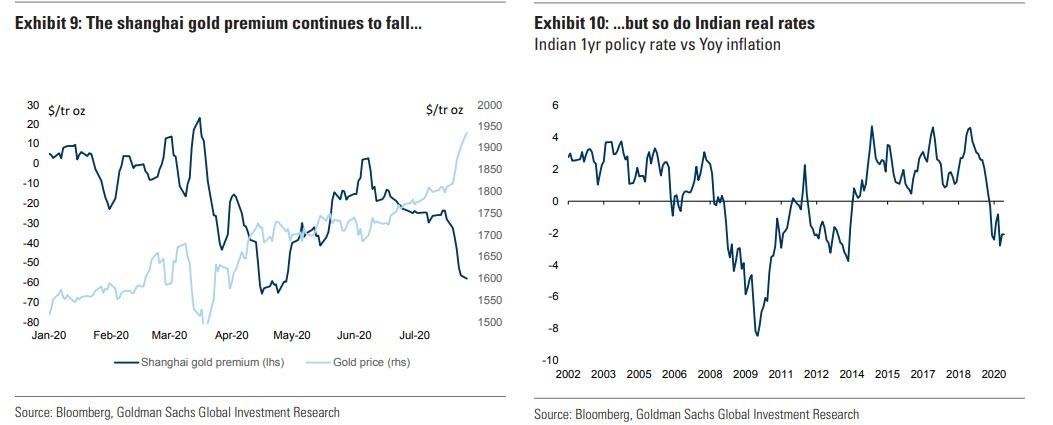

Indian gold imports are still down 80% yoy in June and the Chinese gold premium is beginning to turn negative again (see Exhibit 9). More recently, however, the weakness in EM demand has been driven more by gold’s high price, as consumers cannot afford to buy gold products at those levels. However, EM currencies are no longer under pressure and India has begun to see the rupee strengthen over the past month. EM growth is also beginning to recover with EM activity entering positive YoY territory in June for the first time since January and our economists seeing the worst of the EM outlook behind us (see Exhibit 10). EM retail investment demand is also boosted by easier monetary policy together with continued inflation driving EM real rates down. In India, policy rates fell below the YoY inflation rate for the first time since 2013.

We will likely see this demand materialize when price stabilizes somewhat and DM investment purchases slow down, creating more room for EM consumers. We feel that for now, investors should not be concerned by weak EM demand prints.

That’s what you might call a gold “royal flush”.

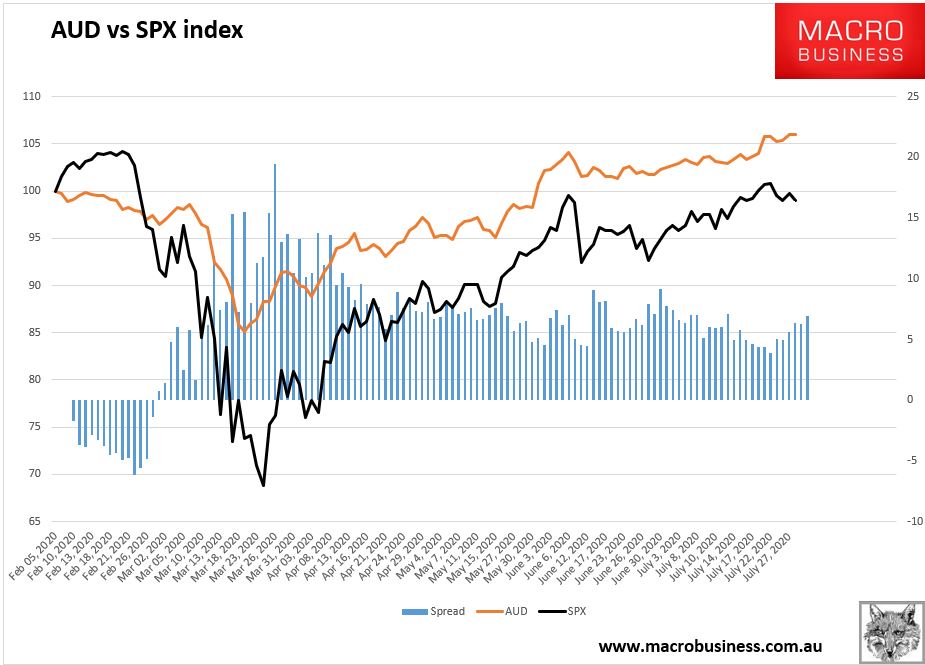

The broader commodities hedging bid is obviously AUD bullish as well which helps explain why the AUD has outperformed stocks in recent days:

But only so long as the risk trade survives and I still think that the mushrooming house price bust will kill the AUD rally in the end, which makes Australian miners especially attractive.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.