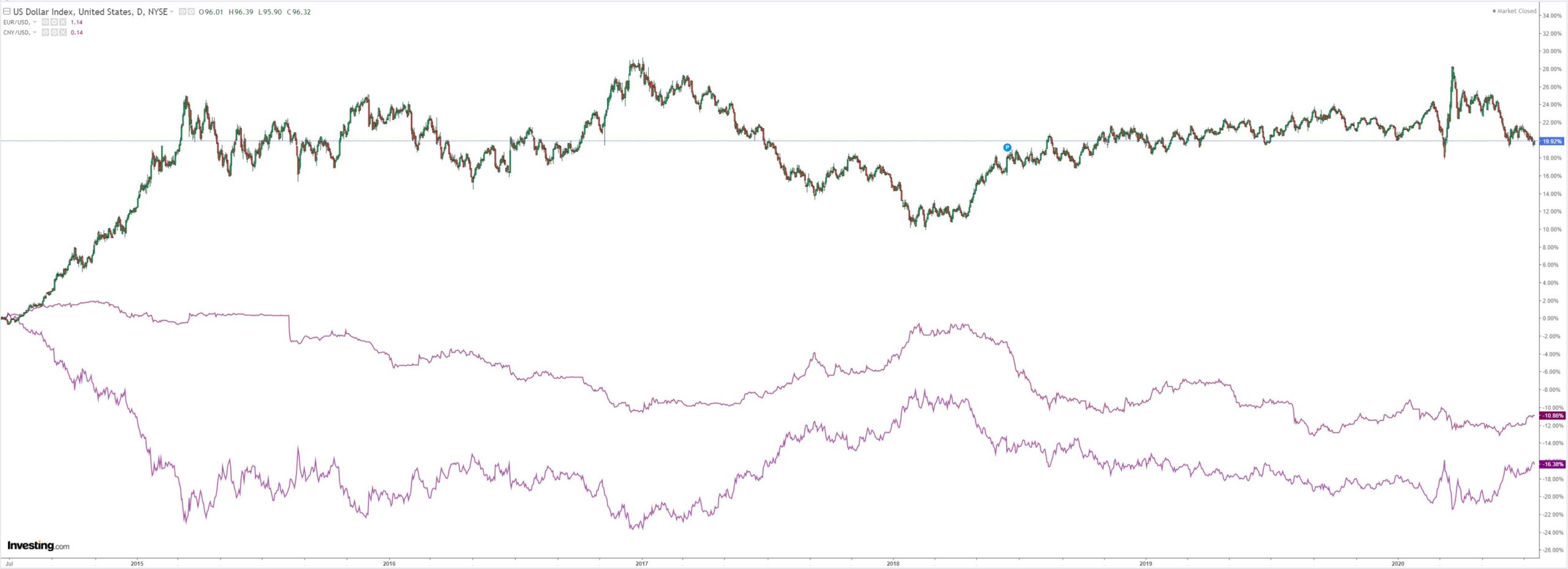

DXY was up last night:

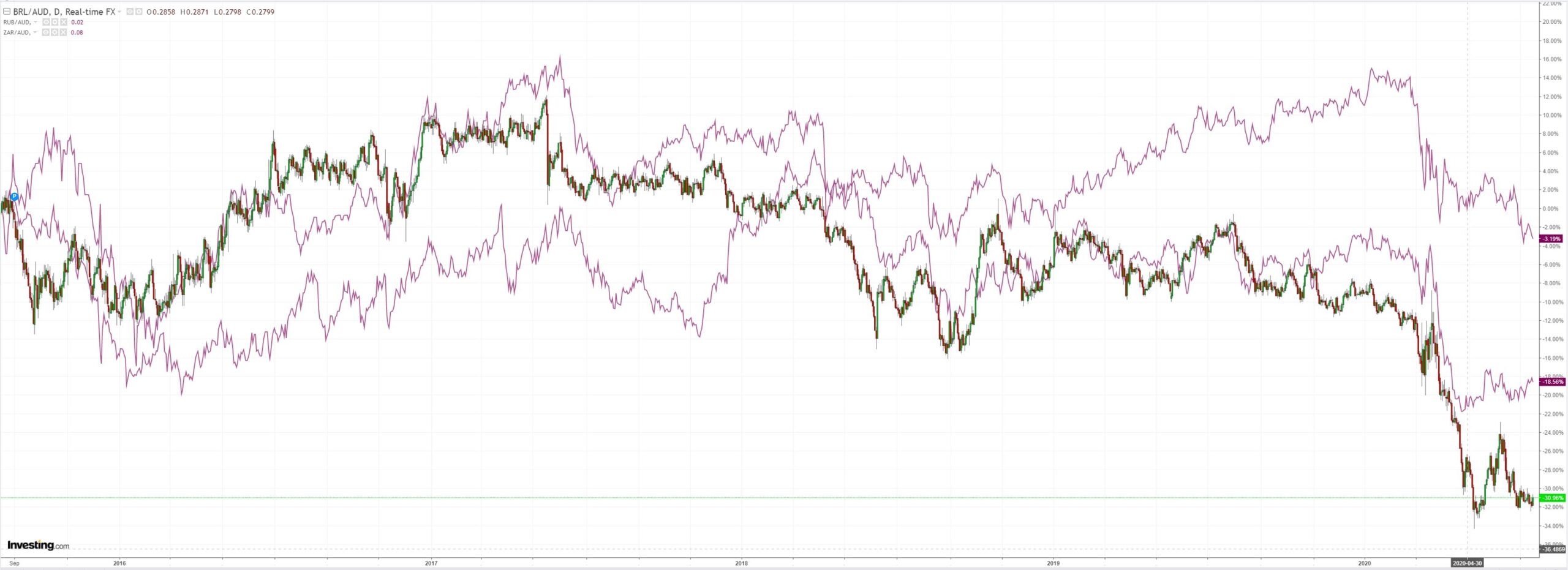

Australian dollar fell sharply:

EMs were worse:

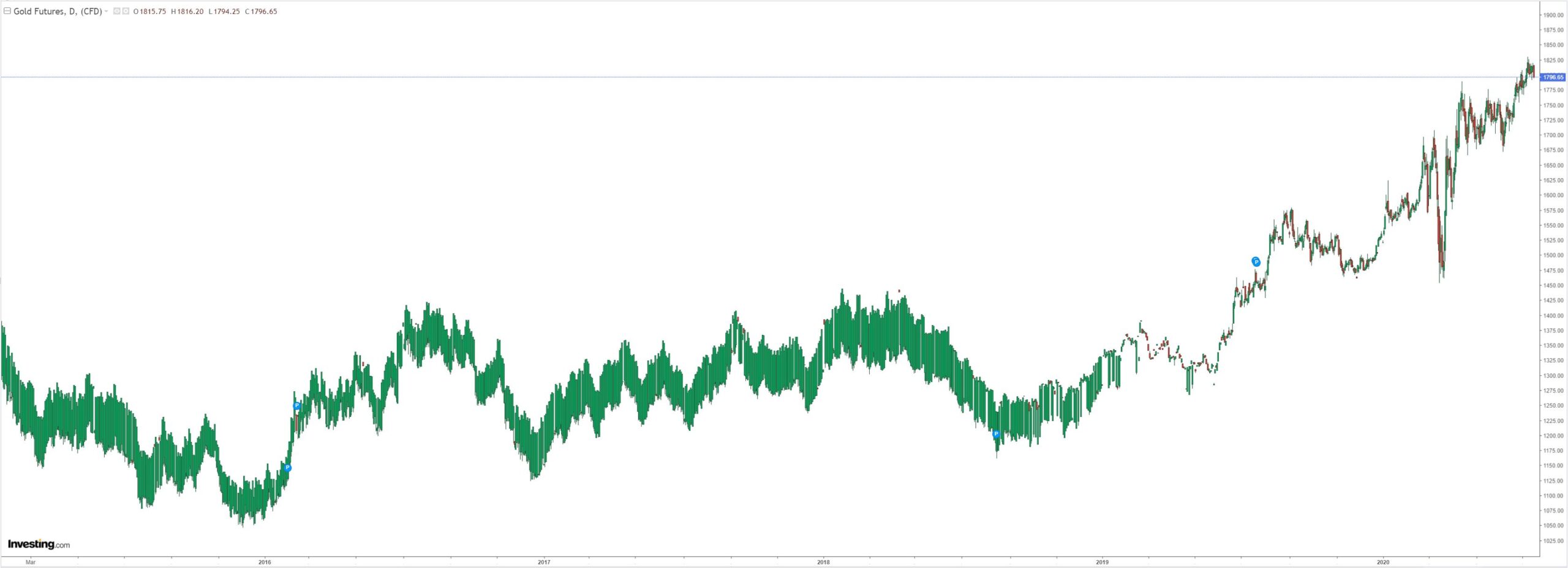

Gold was hit below $1800:

Oil is hanging on:

Dirt has flamed out:

Miners were mixed:

EM stocks reversed:

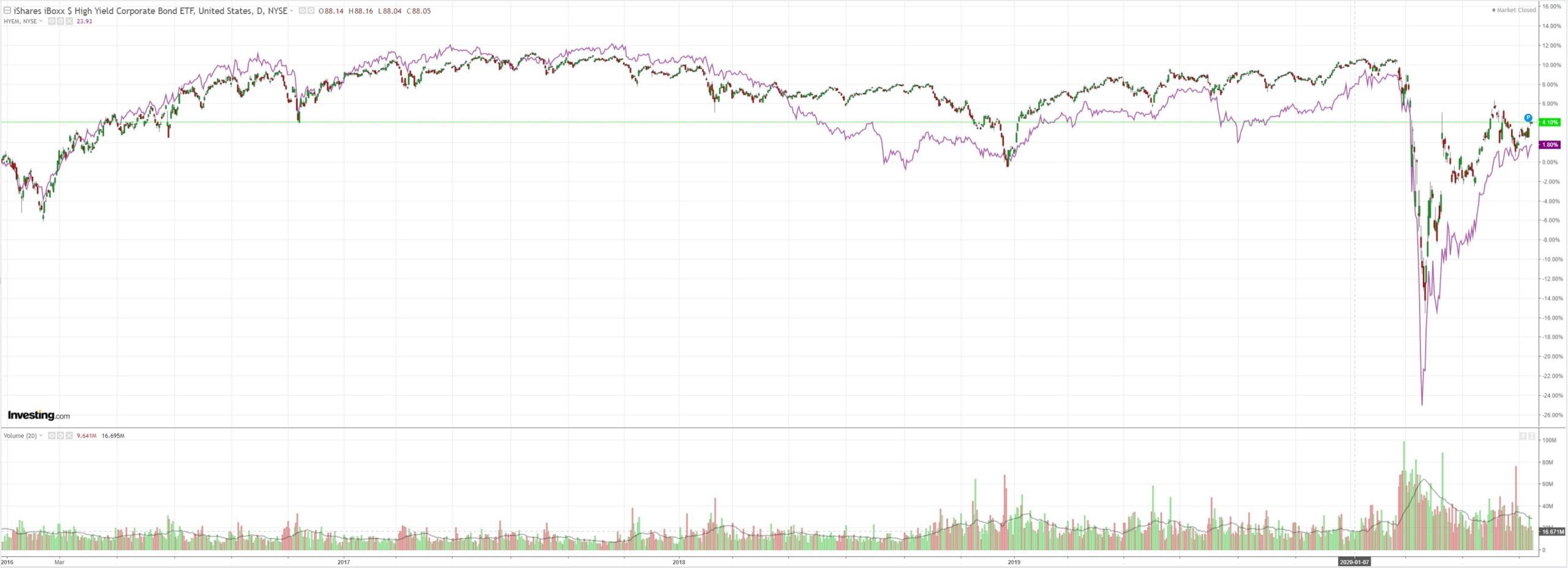

Junk was fine:

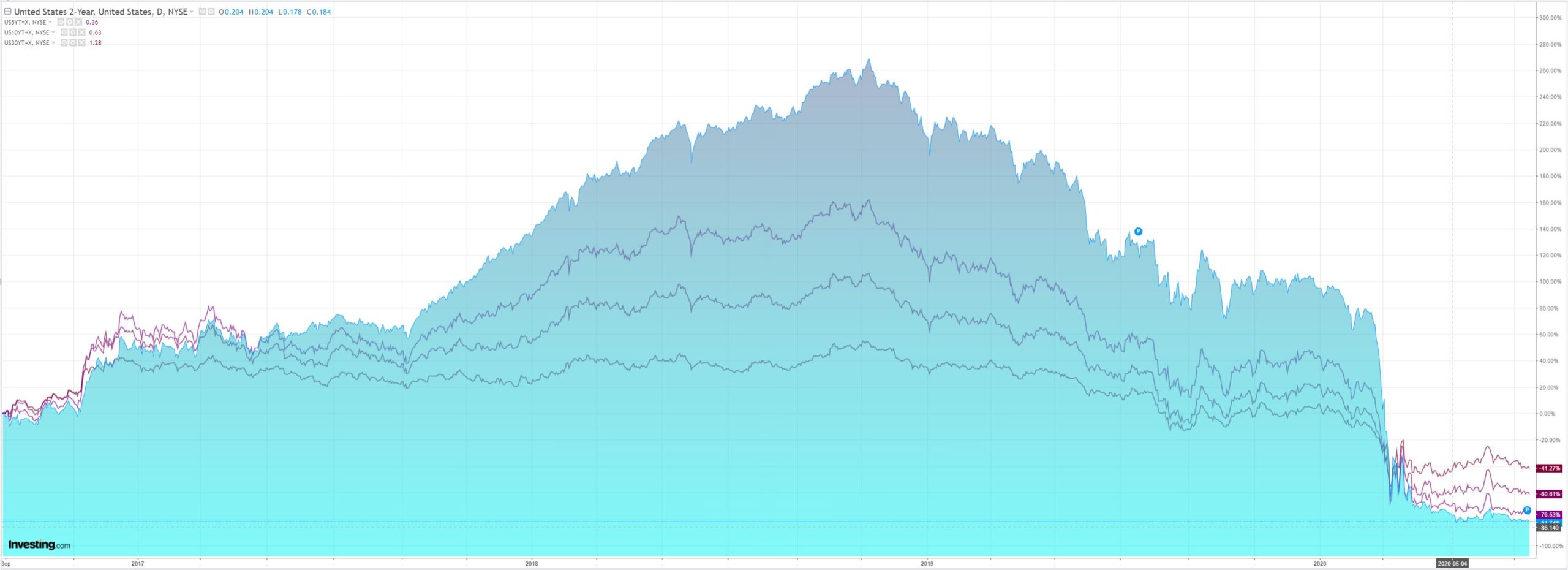

Treasuries were bid:

Stocks reversed at resistance:

Westpac has the wrap:

Event Wrap

ECB left policy unchanged, as universally expected, at their July policy meeting. The statement provided little new colour and though Lagarde spoke of short term data providing -evidence of recovery and affirmation that there was good demand for the ECB’s liquidity provisions through TLTRO-III’s there was little of market interest. Even the Press conference statement from Lagarde that the ECB hoped the EC will swiftly approve their Recovery Fund and plans had little impact.

US June retail sales proved to be firmer than expected posting further rebounds of +7.5%m/m for headline sales and 6.7%m/m for ex-auto and gas (est. +5%m/m for both). However, the outcome was well within the wide range of estimates and failed to assuage concerns that retail activity may subside in 2H.

The Philly Fed July business survey dipped less than expected after last months surge. The headline dipped to a firm 24.1 (est. 20, prior 30.2) supported by sound new orders but an especially firm rise in employment to 20.1 from -4.3. However, the enthusiastic outlook did pullback to a still sound 6.0 from the prior high 66.3 as COVID cases may have reduced optimism. Initial job claims remained at 1.3mn (est. 1.25mn) but continuing claims pulled below 18mn to 17.34mn (est. 17.5mn).

The US July NAHB housing data was firmer too at 72 (est. 61, prior 58) but strength in searches for suburban homes hid concerns over a slowing economy and rising COVID cases.UK’s employment report was generally sounder than expected with a smaller decline in employment of -125k (est. -275k) in the last 3months and unemployment remaining steady at 3.9% (est. 4.2%). A solid headline lift in average wages disguised a drop in low earners and hours worked was low, reflecting furloughing of employees.

Event Outlook

NZ: BizNZ June PMI is expected to rise from the prior 39.7 but may struggle to regain the inflection point of 50 towards expansion.

Singapore releases its notoriously volatile Non-oil Domestic Exports (Nodex) for June. Lower petrochemical exports are likely to lead the data lower, market estimate. -4.6%m/m.

Eurozone final June CPI is unlikely to differ from its preliminary release of +0.3%y/y and core of +0.8%y/y given the lack of variations at national levels.

US releases June housing starts and permits which are expected to show further sound post-lockdown rebounds (+4.3% and +14.4% respectively) followed by the University of Michigan’s consumer survey where sentiment is expected to drift off last month’s 80 reading (est. 78.1) due to the recent rises in COVID-19 cases in the Sun-belt States.

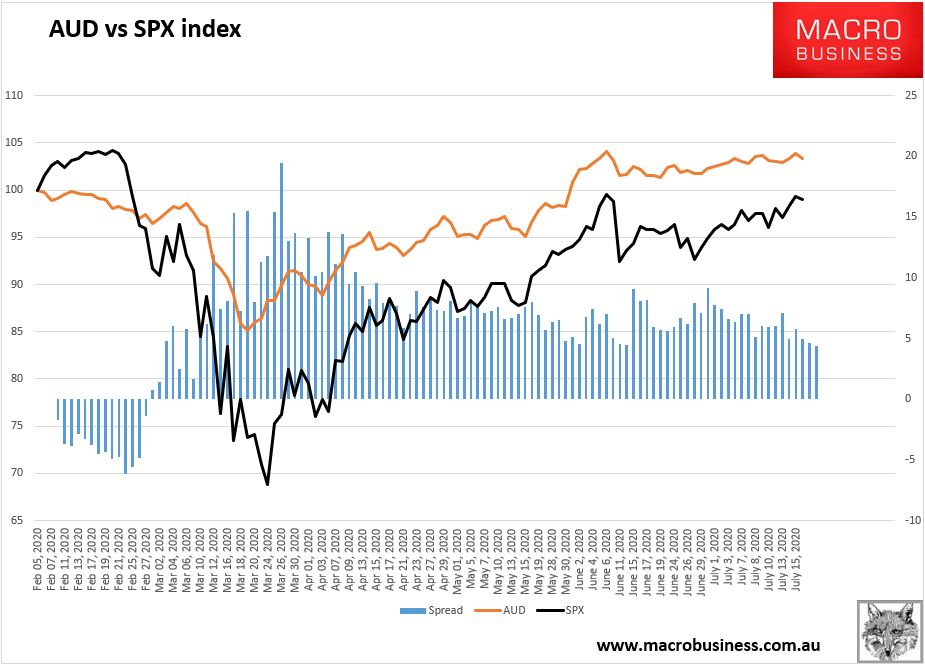

The only chart that matters saw the AUD slowing to the weakest correlation with stocks since the crash:

We can put that down to a number of reasons:

- the Chinese equity surge was crushed by authorities;

- Chinese data was not very good, except for iron ore;

- S&P gains have slowed and it may be as well that risk is getting tired;

- perhaps most importantly, the south-eastern outbreak is bubbling away with a rising risk of a Sydney lockdown.

The immediate fate of the currency will likely be determined by the last point. A Sydney lockdown is the end to Australia’s virus exceptionalism.

Worse, it raises the distinct prospect of a national house price crash which is one reason why the AUD was underperforming coming into crisis in the first place.