The US jobs report was good as it was always going to be, via Calculated Risk:

Advertisement

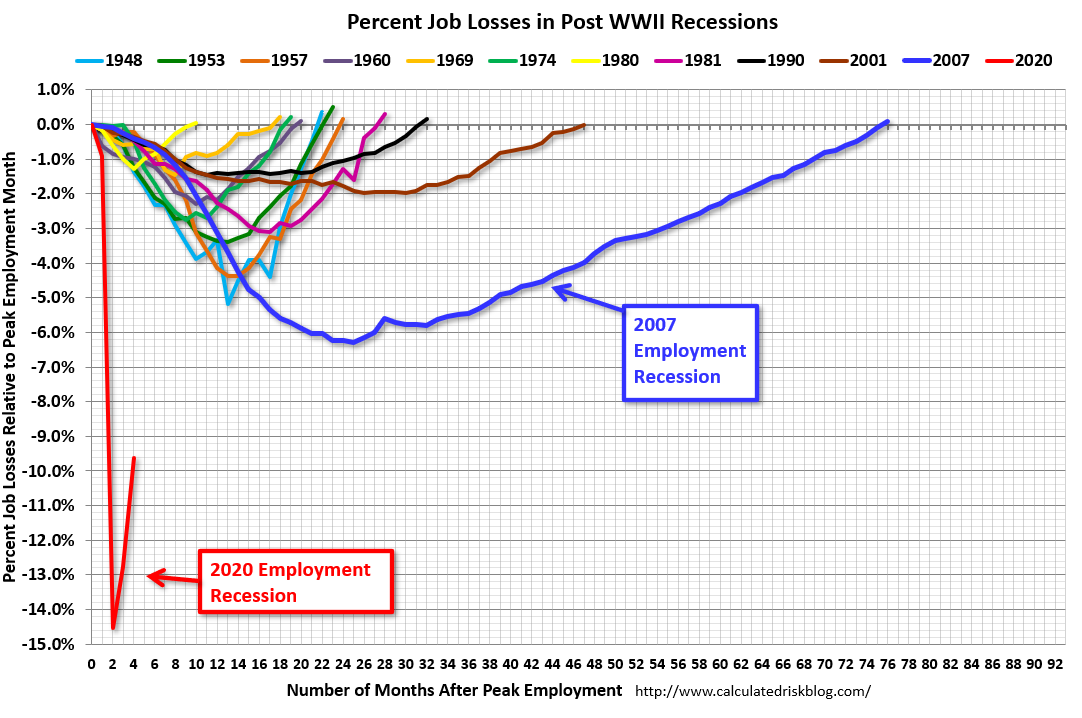

The headline monthly jobs number was well above expectations and the previous two months were revised up 90,000 combined. The headline unemployment rate decreased to 11.1% .

Last month I noted that the “reopenings” would be a June story, and that is what this report suggests. In addition, companies using PPP had to rehire employees to convert the loans to a grants. Unfortunately, the surge in virus infections and related closures, will probably negatively impact the July report. In addition, we will probably start to see more PPP related layoffs.

As a reminder, the course of the economy will be determined by the course of the pandemic.

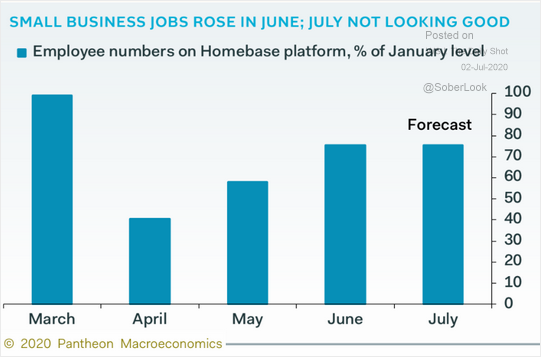

The question has always been how far and fast does the recovery get? The leading indicators already suggest that the virus has stalled the bounce in July for jobs:

Advertisement

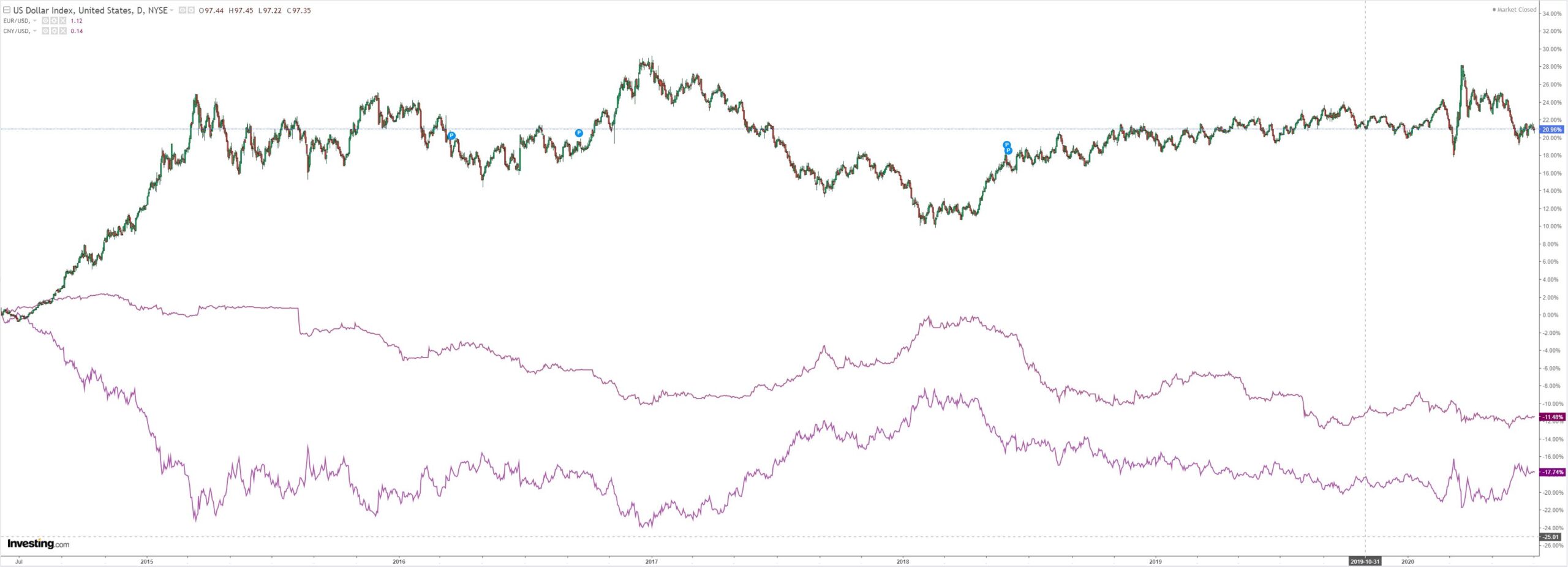

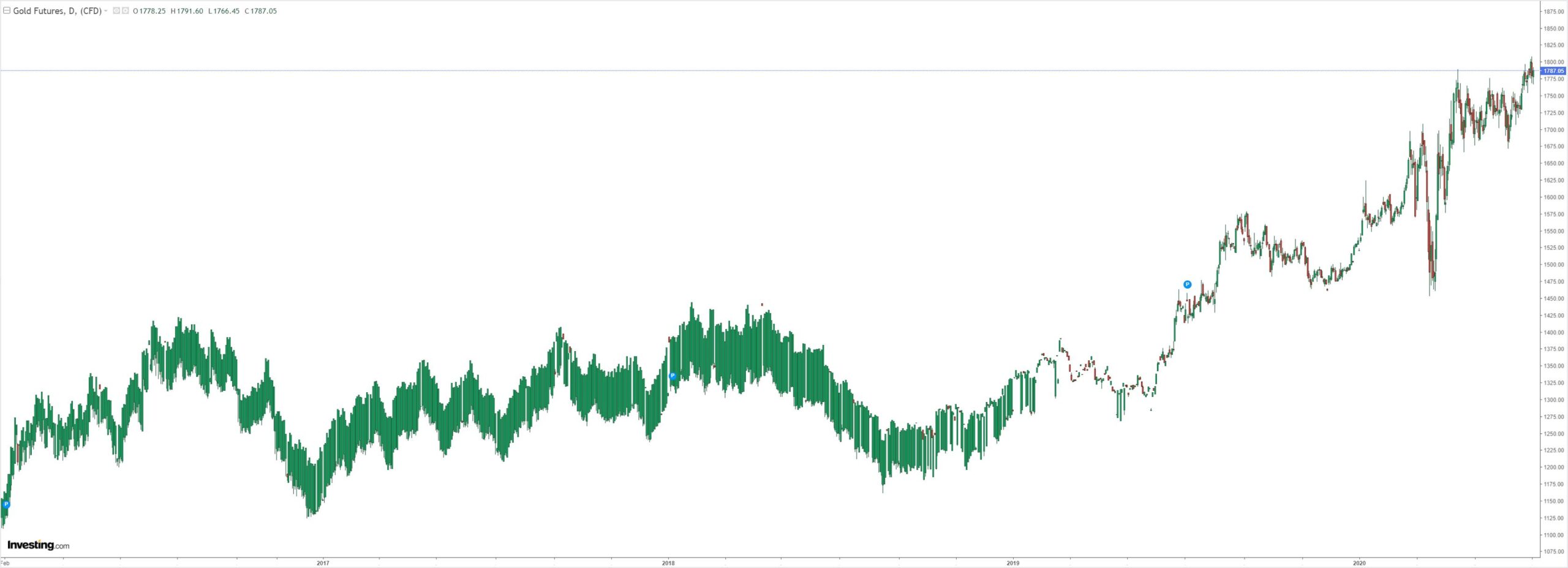

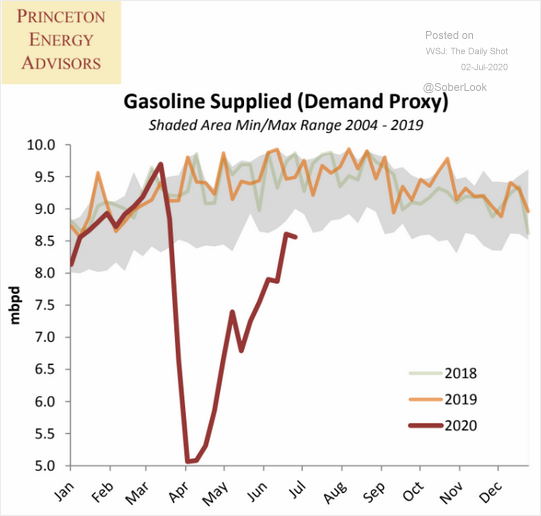

For demand:

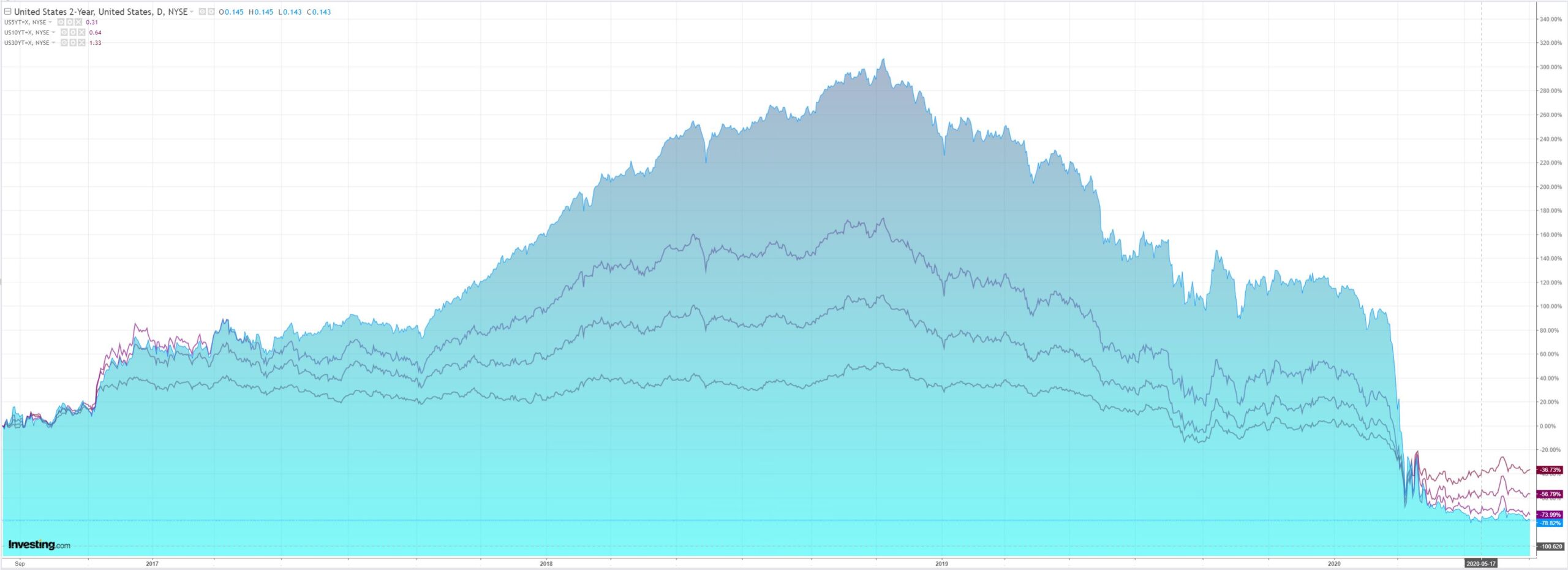

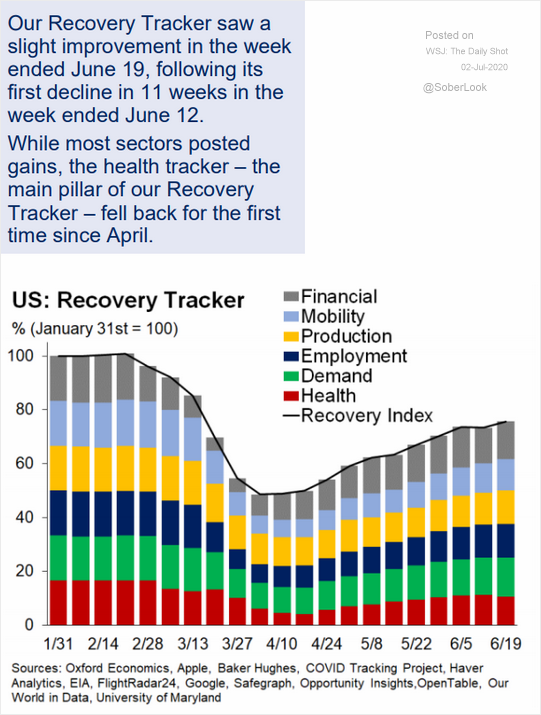

For the trajectory of recovery:

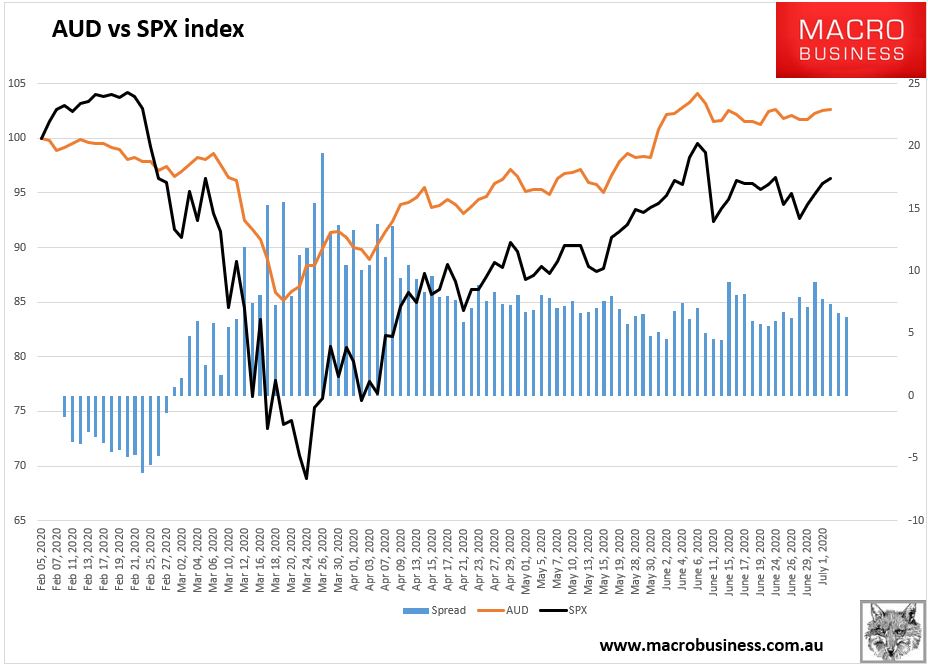

In short, what comes next is the flattening swoosh recovery not the “v-shape” and a stall well below previous levels of output with huge implications for earnings.

Advertisement

Though when stocks and the Australian dollar will recognise that is another question.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.