DXY is at the verge of a major breakdown as EUR surges:

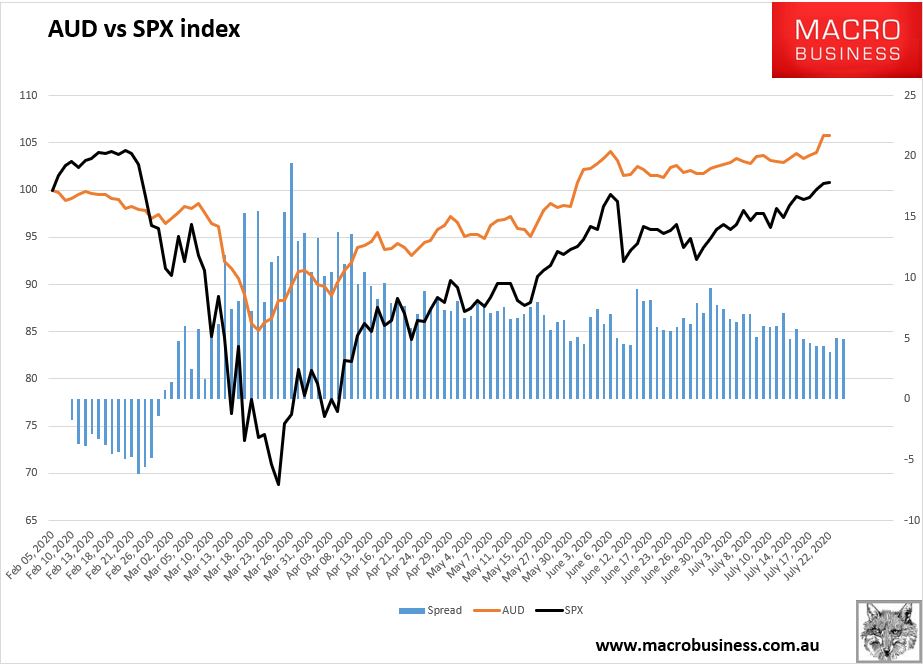

The Australian dollar is a virtual EUR proxy:

It was mixed versus EMs:

Gold has its ears pinned back:

Oil grinds on:

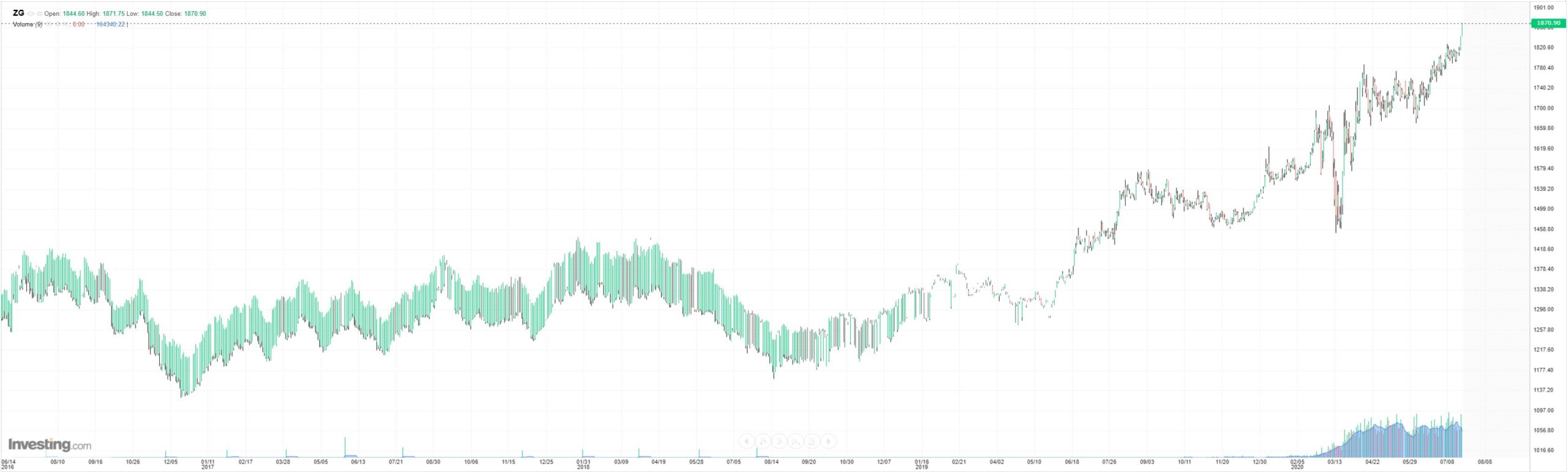

Dirt has flamed out:

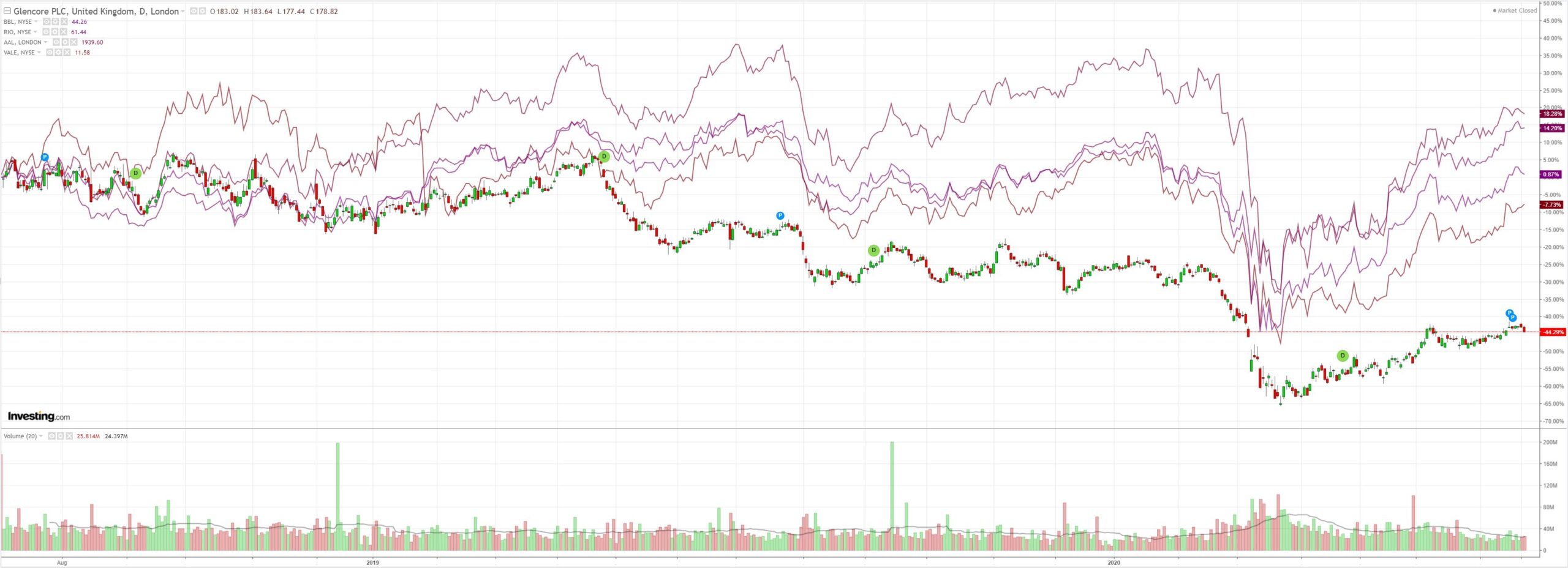

And miners:

EM stocks too:

Junk has a new lease on life:

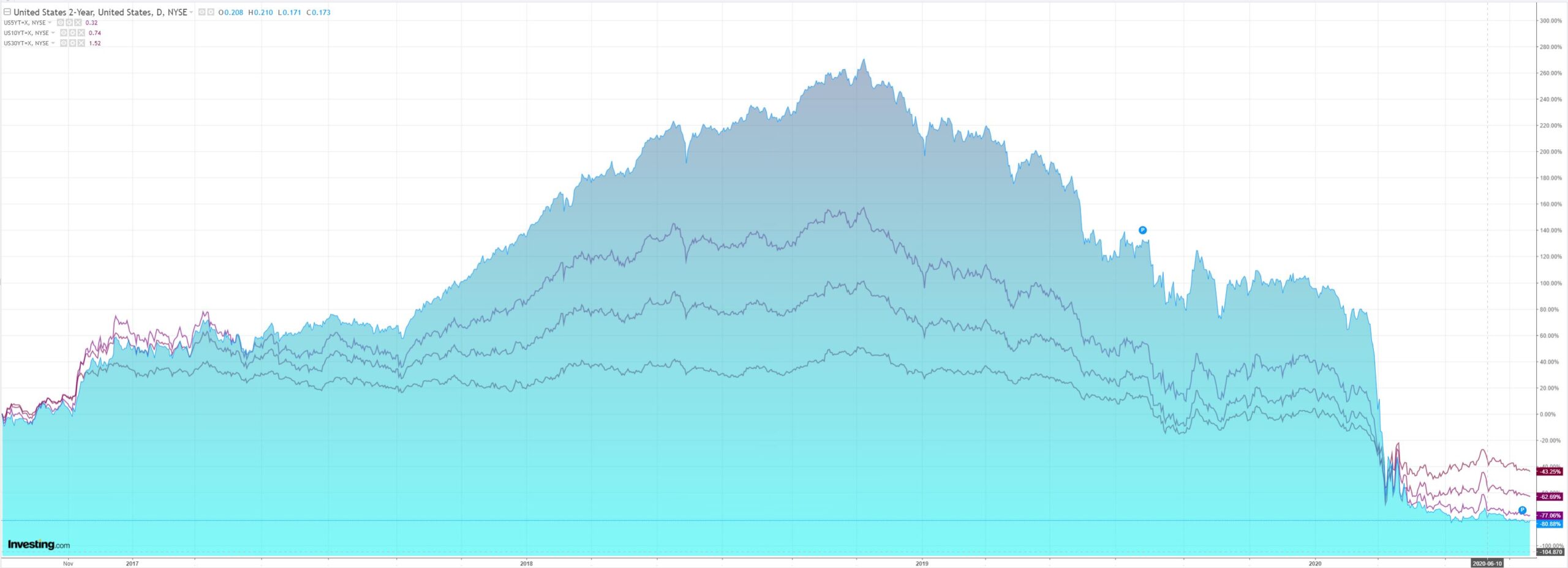

Yields are dead:

Stocks only go up in the US:

The only chart that matters is beginning to fade in importance:

Why? This in Europe:

Investors will view Europe’s €750bn pandemic recovery fund with a mixture of hope and apprehension.

Apprehension, because even though the scheme has won the approval of the EU 27, there can be no guarantees of a smooth journey from this point. Keeping sceptics such as Austria, Denmark, the Netherlands and Sweden on board will be fraught with difficulty.

The region’s “frugal four” economies may have secured key concessions but will demand constant scrutiny of how the money is spent. Fund recipients can expect zero tolerance if they backpedal on reforms, which could mean further political disputes and spending delays.

Still, hope is in sufficient supply. Much of it comes in the form of Franco-German resolve. There is every possibility that Europe’s two economic powerhouses — upon whose shared vision the plan is built — succeed in bridging the gaps.

Indeed, whenever the two have worked in tandem, they have proved a formidable pairing. It was their alliance that kept Britain out of the European Economic Community for years in the 1960s, and it is to their collective effort that the euro owes its very existence. Given that the frugal four account for just one-tenth of the bloc’s total population, it is a fair bet that Paris and Berlin — which speak for almost two-fifths — will prevail again.

If they do, they may end up transforming the investment landscape. Europe’s bonds, currency and stocks could become much bigger features of international portfolios.

Whether it stands the test of time won’t matter for a while. For now, EUR is stable and its recovery is better than the US as well.

This bid into EUR is going to kill the continental economy before very long. With or without eurobonds it is still an export-driven economy. But that, too, will take time. And while the EURO rises it lends a huge tailwind to global reflation as it sinks DXY.

A falling USD lifts all boats, with capital flows dropping interest rates and boosting investment across the emerging world. Commodity prices take off. And currencies follow.

It also puts a healthy earnings tailwind behind hugely overvalued US stocks which will help backfill the bubble a little.

Alas, for Australia, it is all bad news. Sure, commodity prices lift but that is now borderline irrelevant to income and living standards. No investment of substance will follow given we’re built out for a century of expanding demand ahead of time, leaving labour bereft and the nation wrestling with an uncompetitive currency. Especially so since the RBA is still operating in the twentieth century on these matters.

The Australian dollar will tail the EUR higher until the local economy is weak enough to kill the rally. That won’t take long but given how recalcitrant the RBA is on more easing it will take a lot longer than it should. During the post-GFC period RBA neglect reached apocalyptic levels with a currency to match:

The Australian dollar is now headed upwards into EUR hell.