Ian Marshman and Frank Larkins from the Centre for the Study of Higher Education at the University of Melbourne have released research assessing which Australian universities are most exposed to the downturn in international students.

Below are key extracts:

Summary

The predicted revenue losses of 38 Australian universities to 2024, as a result of the decrease in overseas student revenues linked to the COVID-19 pandemic, are modelled in this study. A 2020 outcome and two longer term scenarios to 2023-2024 are modelled. It is demonstrated that the universities face very serious challenges with varying degrees of financial management risk.

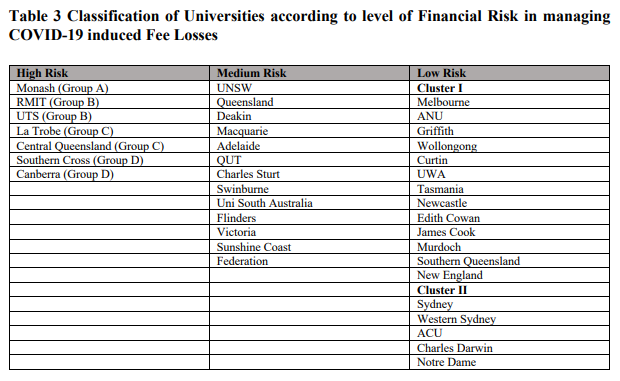

Based on the analyses conducted universities are placed into three categories in accord with the financial management risk challenges that have been identified. Universities are predicted to face either high, medium or low risks over the period from the present to 2024, because of the loss of overseas fee revenue…

Seven universities are placed in the highest financial management risk category – Monash, RMIT, University of Technology Sydney, La Trobe, Central Queensland, Southern Cross and Canberra universities. Another 13 universities are assessed to face medium financial management risk. The remaining 18 universities, just under half of the total sector institutions, have been categorised as facing management risks that are of lower severity.

The nature of the risk varies according to the relative reliance on international fee revenue and the underlying financial resilience of individual institutions. The adverse consequences of the COVID-19 pandemic on the university sector are both immediate and can be anticipated to endure for many years…

Data and Analysis Methodology…

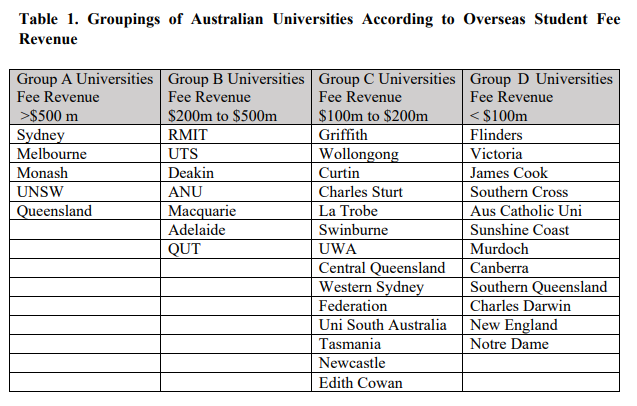

For the purpose of the present in-depth modelling the universities are clustered into four groups determined according to the size of their international student activities as listed in table 1. Group A is the cluster of 5 universities profiled previously (1) with overseas student revenues in 2018 in excess of $500m. Group B includes 7 universities with 2018 revenues between $200m and $500m. Group C has 14 universities with overseas revenue in 2018 between $100m and $200m. The remaining 12 universities in group D had overseas student revenues of less than $100m…

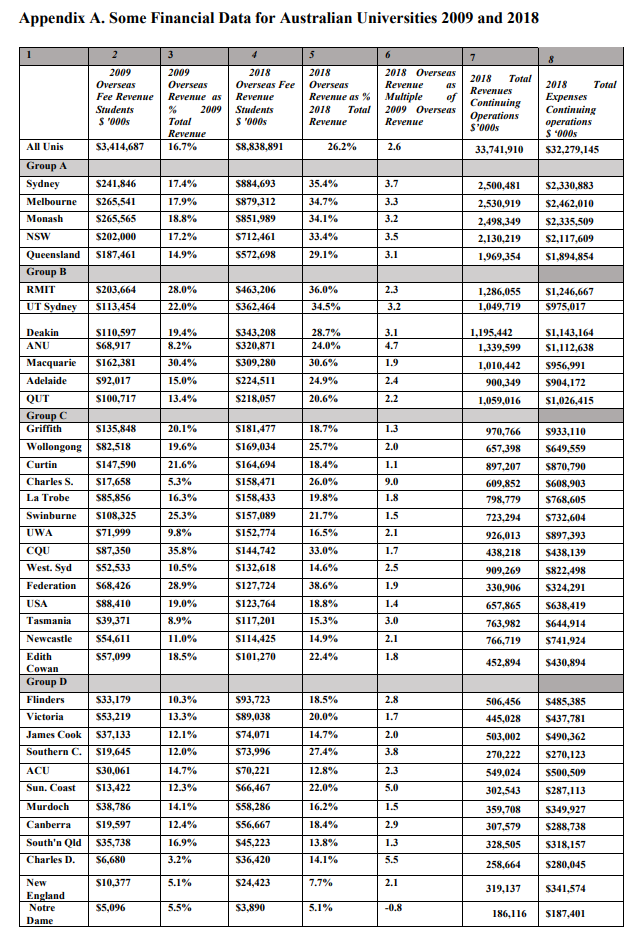

The relative importance of the four clusters of universities in aggregate in terms of their contribution to international student activities is shown in table 2, ranked in appendix A according to overseas fee revenue…

The 12 universities in groups A and B enrolled 57% of the overseas students in 2018 and received 70% of the fee revenue. The group A revenues were 3.4 times greater than the 2009 result and the group B revenue 2.6 times the 2009 figure. Collectively, these universities are the dominant players in the overseas student market and ended 2018 in a strong financial position…

At an individual university level, the Group A Universities (Sydney, Melbourne, UNSW, Monash and Queensland) achieved the most sustained rate of increase in international student fee revenue of more than three times the 2009 figure over this period (appendix A, column 6).

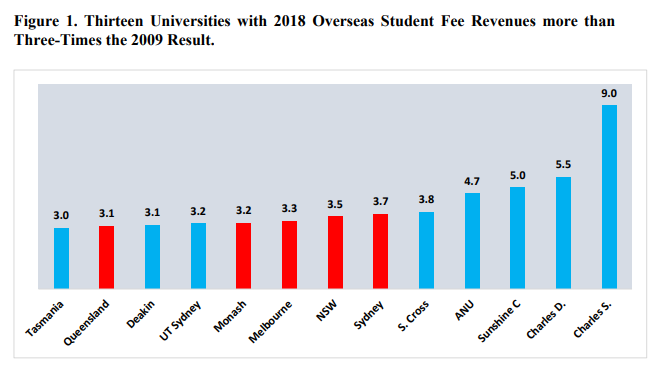

Other strong performers in group B with a multiple of more than three times were UTS, Deakin and ANU. A small number of universities in group C and D also reported strong growth over the decade as their international activities expanded from a comparatively low base. The 13 universities with exceptional growth are shown graphically in figure 1. The five group A universities are shown in red…

These data would indicate that Australian universities have enjoyed a decade of remarkable revenue growth as a result of the expansion of international education. This would suggest that, assuming the exercise of prudent financial stewardship over the past decade, most universities will have had the capacity to build up reserves to help deal with at least a temporary major revenue shock occasioned by COVID-19. The subsequent analysis indicates that this is not the case for all universities. Some of those with pre-existing weak balance sheets or with very large international student programs appear not to have been able to build an adequate buffer of reserves…

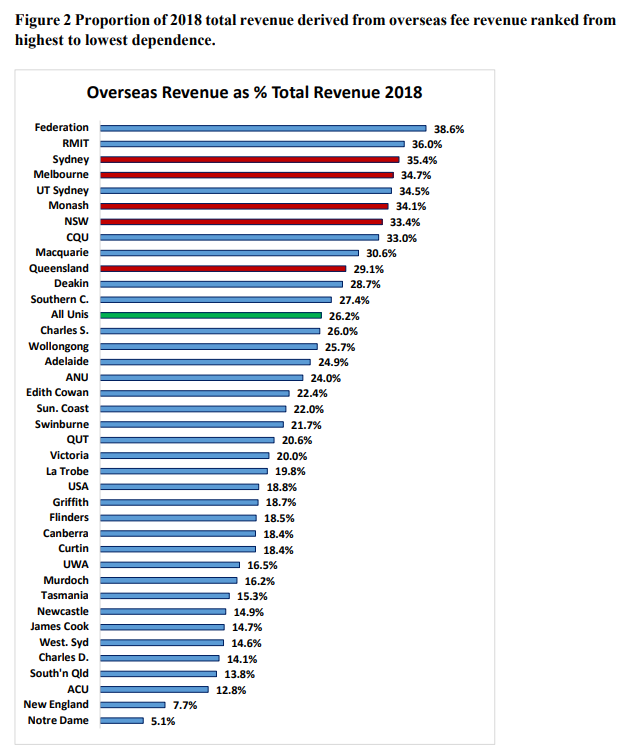

Some 12 universities have a dependence greater than the sector-wide average of 26.2%. These universities in rank order are: Federation (39%), RMIT (36%), Sydney (35.4%), Melbourne (34.7%), UTS (35%), Monash (34.1%), UNSW (33.4%), Central Queensland University (33%), Macquarie (30.6%), Queensland (29.1%), Deakin (28.7%) and Southern Cross (27.4%) It is noteworthy that all the group A universities (shown in red) are among universities with the greatest dependence. The average for all universities is shown in green…

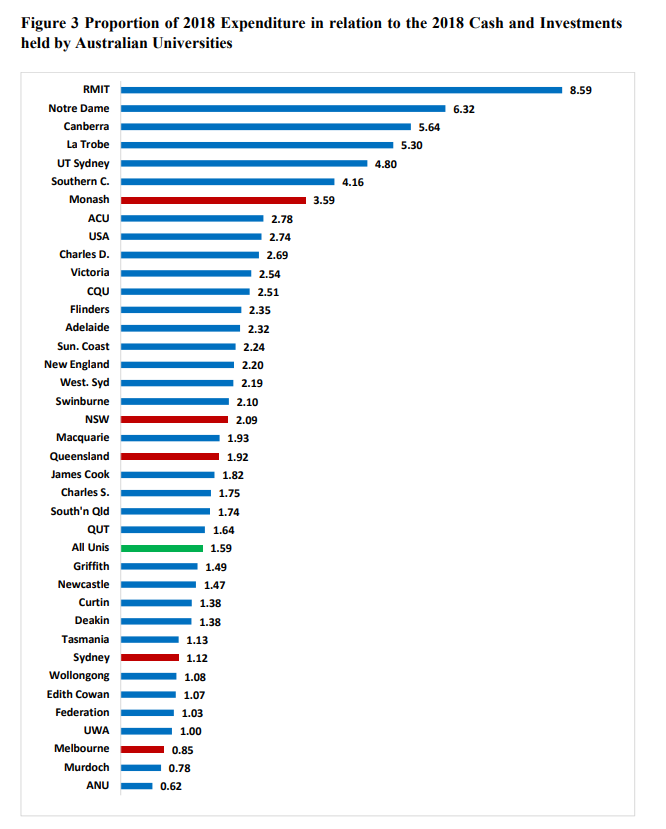

The 2018 expenses on continuing operations as a ratio of the cash and investments held by universities is shown in figure 3. The universities are again ranked from the highest to the lowest ratio. A number greater than one means that the university has annual expenses greater than their accumulated total cash and investments reserves. RMIT is the most vulnerable university with annual expenses being 8.6 times reserves. ANU is in the strongest position with annual expenses less than reserves at a ratio of 0.62…

Integrating the data shown in figures 1 and 2, there are nine universities for which international student fee income constitutes at least 30% and there are seven universities with 2018 expenditure that is more than three times 2018 cash and investments…

Three large metropolitan universities, RMIT, UTS and Monash are the only ones included in both of these extreme subsets. These are potentially the least resilient and among the most financially exposed to a loss in overseas fee revenue…

Based on the analyses conducted, consistent with the scenarios modelled, universities are placed into three categories in accord with the financial risk management challenges that have been identified. The categorisation of universities as facing high, medium or low financial risk over the period from the present to 2024 is based on the impact of loss of overseas fee revenue. Other sources of potential revenue loss have not been considered in the present analysis but are briefly covered in the Conclusion below. The categorisation of universities is shown in table 3…

This analysis and associated modelling demonstrate that both in the short term and the longer term under both benign and more lasting impact scenarios of COVID-19 several Australian universities appear to have little funding capacity, in terms of readily available current assets, to be able to absorb the likely loss in revenue as a result of a significant decline in international student enrolments. Within the sector a number of universities will be greatly challenged by the consequences of COVID-19. For a few this may create existential issues in terms of ongoing financial viability…

Three of the most vulnerable universities and ten of the 13 medium risk universities are metropolitan universities for which the scale of international student enrolments has become the greatest risk factor.

The universities in the High Risk category face significant financial challenges well above their capacity to absorb within available reserves. This suggests that without an alternative source of revenue growth they are facing a significant period of cost containment as a central part of any longer term financial sustainability strategy in the event actual COVID-19 impacts reflect the assumptions on which both the optimistic and the pessimistic scenario are based.

Four of these universities were identified in section 4 as already the least resilient irrespective of the consequences of the COVID-19 pandemic.

Clearly, the concept of risk management has escaped many of Australia’s universities. Rather than taxpayers coming to their rescue and rewarding their poor judgement, they should be exposed to their folly.

Otherwise, Australia’s universities will be incentivised to take greater risks in the future to maximise revenues, knowing that Australian taxpayers will bail them out when things go bad.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.