An un-natural vision of stability. The US trade deficit, a proxy for foreigners’ US dollar (USD) saving, is exhibiting remarkable stability of late. Ordinarily, stability tells us that there is nothing further to see – but sometimes, it can actually be a deceptive sign of instability. Consider that the national accounting identity says that the sum of saving across all sectors – households, corporates, government and the rest of the world – must equal zero. Re-arranging, the trade balance should equal the sum of household, corporate and government saving. In this context, it is very interesting, and perhaps even un-natural that the US trade balance is barely moving despite extremely large swings in household, corporate and government saving.

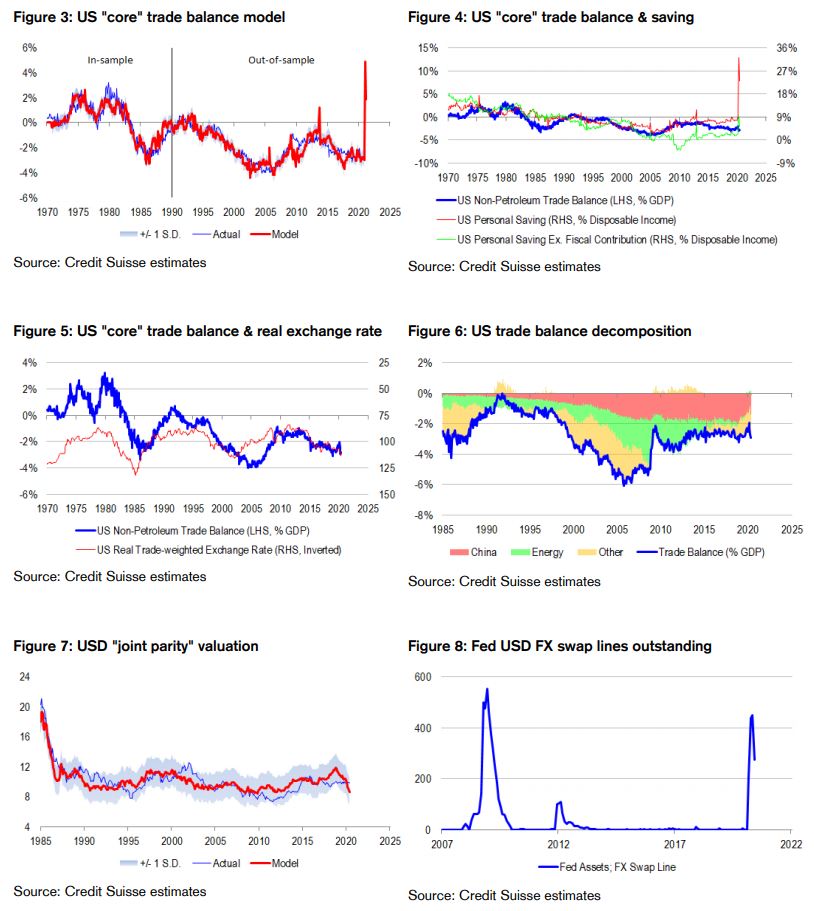

“Make America Great Again” coming soon? We have constructed a model of the US core, or non-petroleum trade balance, based upon the real trade-weighted exchange rate, household saving and government saving. The model has historically been able to predict the core trade balance with a lead time of almost a year. Importantly, model parameters have proven quite stable through time, giving us some confidence in the framework’s “out-of-sample” forecasting properties. Since 1970, higher (lower) domestic saving and a weaker (stronger) real exchange rate have typically resulted in trade balance improvement (deterioration). With the US household saving rate spiking to 23-32% of disposable income in April-May, and the USD depreciating modestly over the same period, our model has started projecting a large swing in the core trade balance to a 2% of GDP surplus from a 3% deficit. Crisis dynamics should already be “Making America Great Again”, even apart from protectionist policies and rhetoric.

A potentially large US dollar shortage from trade, but for the Fed’s swap lines. If the US becomes a smaller net importer of goods and services from the rest of the world, it is also becomes a smaller net exporter of USDs to pay for them. This matters, because the world at large is on a so-called “eurodollar” system, where USD-denominated funding is key. Our concern with recent and future dynamics is that a sharp 4-5% of GDP swing in the trade balance to surplus from deficit could very easily disrupt the flow of USDs to the broader world, resulting in material USD funding shortages for any economy or entity dependent on such funding, whether directly through foreign (USD) currency-denominated borrowing, or indirectly through hard (USD) currency pegs. The good news has been that the Fed, together with other central banks, has been hard at work trying to fill a potential trade-driven void in USD funding through portfolio channels, notably through the extension of foreign exchange (FX) swap lines. Foreign central banks have been given the right and ability to provide USD liquidity to foreign financial institutions, by borrowing it first from the Fed. In March and April, outstanding FX swap lines increased by 11% and 12% of GDP respectively, vastly outstripping any USD shortages that could have emerged from trade. But the bad news is that from May onwards, these swap lines have started to mature, dragging on USD liquidity and contributing to shrinkage of the Fed’s balance sheet. A risk has arisen that, in the absence of active and growing FX swap lines, USD liquidity could very quickly dry up as a result of trade dynamics. Therefore, the criticality of FX swap lines to the post-March veneer of stability we have experienced should not be underestimated.

Corporates are dealing and struggling with short-term frictions. Our model says that the trade balance needs to improve on the back of household de-leveraging, manifesting in a higher saving rate, causing imports to fall disproportionately to exports. But for as long as it is not doing this, despite extremely large fiscal deficits, and high household saving, the national accounting identity tells us that corporate saving and profits should be suffering. The official narrative is one of extraordinary supply chain disruption, and business surveys strongly indicate this to be the reality, with supplier delivery times rising sharply of late. The question then is why corporates are not acting more aggressively to re-position for trade dynamics. The obvious answer is that it is not a quick process to take back outsourced production capacity, in part because companies have taken decades to push their activities abroad and logistically cannot turn around the situation on a dime. On the flipside, China and emerging markets will not so easily give up their claims on the global supply chain. In part, the sluggish adjustment is also because the shoring up of supply chain security comes at the cost of erosion of competitive advantage, making cost-benefit analysis a tricky exercise. Yet another possibility is that the very act of extending FX swap lines is helping to preserve access to trade financing, preventing a much more aggressive pace of shortening of supply chains globally.

Expect more foreign exchange and inflation volatility ahead. We are concerned about the deflationary aspects of the US shifting to a trade surplus whether because of crisis dynamics or trade protectionist policies. But we also think there is an easy fix – for the Fed to simply re-extend or roll FX swap lines should the need arise. Clearly, there are timing issues to deal with here that could create significant FX and inflation pricing volatility. On top of all of this, we have to deal with the rigidities of trade dynamics, which are proving somewhat costly for corporates near term, and could be inflationary longer term. Also, there is fiscal and unconventional monetary stimulus working in the background to lift money supply and inflation, as well as the ever-present threat of more COVID-19 waves and shutdowns working in the opposite direction. The net sum of all of these forces is quite ambiguous, with the balance hanging in the hands of the Fed and the virus.

A favourable starting point of excess liquidity. For what it is worth, we think that the world is still flush with money, and so we resolve this uncertainty as best we can in a glass “half-full” fashion while recognizing the ebbs and flows along the way. Our proprietary measure of world excess liquidity is the de-trended level of world money supply to nominal output. Currently, this indicator is in extremely positive territory (+14%) suggesting that there too much money chasing too few goods, and certainly more money “out there” than the private sector is accustomed to. Of course, USD liquidity is superior to rest-of-the-world liquidity in terms of the pecking order of significance for the global economy, and so potentially sharp trade shifts are a threat to this state of affairs. To account for the distribution of liquidity and not just the level, we augment our world excess liquidity indicator with our new, USD shortage indicator. The USD shortage indicator has two components – quantity and price. The “quantity” version is equal to the predicted change in the US “core” trade balance net of the change in Fed FX swap lines outstanding (all) expressed as a share of GDP, plus a USD liquidity spread (derived from US money market spreads and cross-currency basis swap spreads). It is designed to capture USD funding availability via trade, credit and central banking channels. The “price” version of the USD shortage indicator is the cheapness of trade-weighted USD relative to fundamentals such as relative price levels, relative terms of trade and real interest rate differentials, in our “joint parity” framework. Interestingly, price and quantity versions of the indicator are highly correlated through time, and so we combine the two versions into a single indicator. Higher (lower) readings are consistent with less (greater) USD funding availability in offshore markets. Our augmented liquidity indicator simply subtracts the USD shortage indicator from our original world excess liquidity indicator. On this basis, we find that even accounting for a trade shock, the world will still have excess money supply, albeit less than before when we give primacy to USD flows. Our USD shortage indicator is set to rise to almost +2% from negative (or surpkus) territory, but this incremental funding shortage only moderately eats away at world excess liquidity tracking at 14%. Even if we take more aggressive estimates of the USD shortage based on quantities rather than prices, we still end up with a state of excess liquidity in the world.

Pack your bags for a long journey with lots of ups and downs. We think that in a pinch, the Fed will come good on its put, and boost USD liquidity in the world further if needed. And considering that the USD is overvalued on a “joint parity” basis, we believe there is certainly room to weaken the USD further, giving the Fed a credible starting point. The trouble is timing. Also, we need to be careful what we wish for. Bond markets are significantly discounting the prospects of inflation – but if the Fed is successful in its endeavours, supply chain de-globalization continues in earnest, and demand stimulus gains traction, inflation should lift. Therefore, nominal bond yields ought to rise, but for Fed intervention to suppress real yields as much or even more than inflation expectations rise. Lower real yields and a weaker USD support commodities at an asset allocation level. Of course, the path is very volatile, not the least because of potentially large movements in the trade balance, a reactive Fed, fiscal stimulus volatility and of course COVID-19. Indeed, when we combine potentially higher and more volatile rates pricing with high COVID-19 uncertainty, we get a toxic mix for risk parity and passive investors who optimize for lower-for-longer rates and lower-for-longer volatility. At a stock selection level, we do not want to be momentum-chasers, following these asset allocators into the defensive abyss, because they could easily get wrong footed in their risk assumptions and be forced to de-risk and de-leverage, putting their most favoured investments up for “fire sale”. But we also do not want to give up on quality either given the prevailing risks. We recommend having a long commodities asset allocation overlay with long quality, short momentum and short value factor positioning. As for currency, “joint parity” fair value for the AUD/USD is close to 75c – but we can understand why investors are uncertain whether there currency will get there given upcoming volatility from the US side of the equation …

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.