Extraordinary factor rotation of late. In early June 2020, momentum and value factor portfolios have been experiencing wild swings. One week it was value very sharply up, and momentum very sharply down, only for the factors to switch places on the leader board the following week. The last time we saw such sharp factor rotation was in September 2019 – and even that was not on the frequency and scale we have seen recently. Indeed, September 2019 was a sharp one-way rotation in favour of value and away from momentum, whereas in June 2020, we have seen multiple and sharp two-way rotations. But nevertheless, the memory of September 2019 has remained fresh in our minds, because it led a spike in market volatility roughly six months later in March 2020. To the best of our understanding, the lead was no accident. September 2019 was all about passive and risk parity investors searching and paying for diversification given extraordinary correlation risk and crowding in their portfolios. Value factors just so happened to offer such diversification, having badly underperformed in prior months, and being positively exposed to yield curve steepening from Fed easing and a truce in US-China trade wars. March 2020 was all about passive and risk parity investors exhausting their search, and being forced to outright de-risk and de-lever in response to an unavoidable volatility shock. Against this backdrop, we have become wary of the risk that history could repeat itself. Therefore, we have been closely monitoring the situation with factor volatility for any clues it might give us about more serious market dislocations to come.

Macro drivers are taking factor volatility to a whole new level. COVID-19, the policy response to the pandemic, and central bank behaviour are clearly distorting factor performance in 1H 2020. COVID-19 is an unprecedented shock to and constraint upon the system, undermining confidence in central banks to alleviate the economic consequences, and increasing uncertainty as a whole. And the fiscal response to the outbreak is just as big a shock to the system, whether in terms of the severity of the economic shutdowns imposed, or the sheer scale of stimulus being brought to the table. Investors are rightly nervous about if and when economies will be allowed to resume normal activity, and if and when inflation could return. Therefore, they do not know whether to position in line with defensive momentum, or to be contrarian and cyclical. Moreover, investors are concerned about de-leveraging risks from the sharp downturn we are already experiencing, and these worries undermine confidence in the ability of fundamentals anchor asset prices, or value factors. Indeed, the policy response to the crisis could end up hurting value investors just as much as the crisis itself, if central banks do not allow yield curves to steepen, detracting from the ability of banks in the value basket to make money by borrowing short and lending long. Finally, to make matters even more complicated, we have the reality that passive and risk parity investors play a much larger role in markets than they used to, and are creating systematic crowding and de-risking cycles in their own right. Therefore, while investors are naturally inclined to search for quality in a downturn, they also fear that crowded quality names could be exposed to passive and risk parity de-risking and de-leveraging behaviour, especially if rates or volatility spike, for whatever reason.

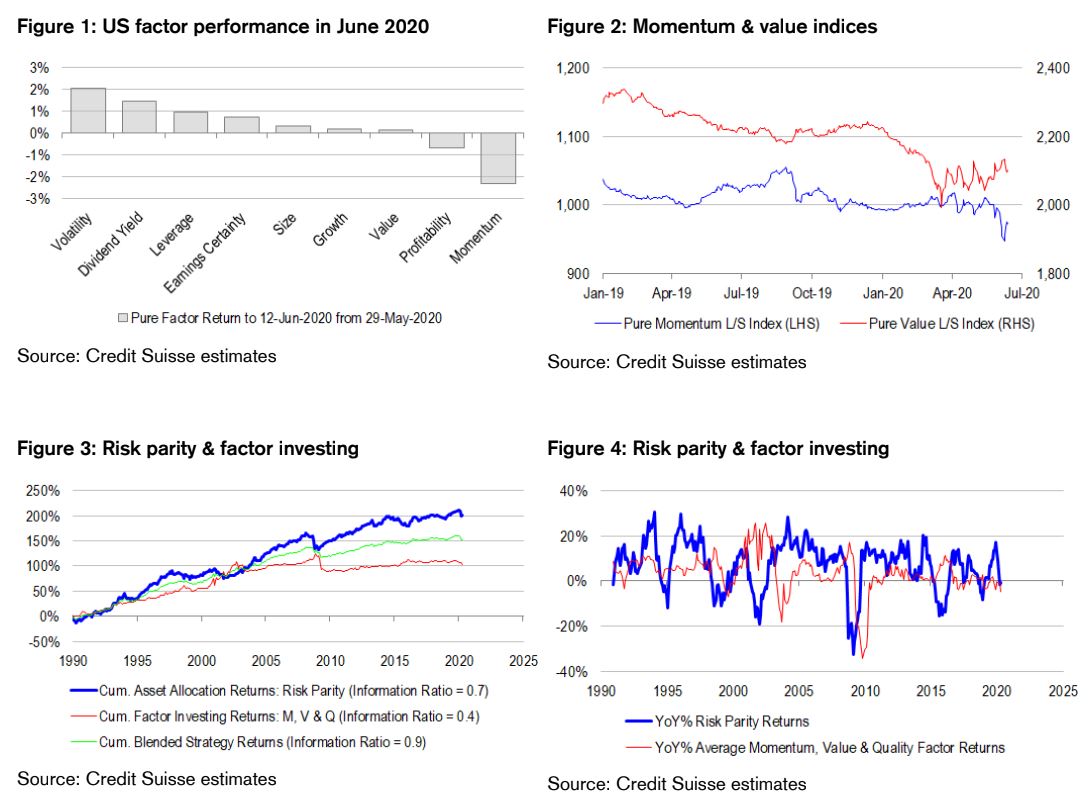

Factors add diversification and new information to asset allocation processes. The conventional wisdom is that equity factor investing merely increases equity beta in portfolios. After all, history does suggest that the cycle in conventional quantitative portfolios based on momentum, value and quality, is led by the cycles in passive and risk parity portfolios. Momentum is often viewed as “glorified beta”, and value the beta “left behind”. But for all of this scepticism, the reality is that equity long-short factors are a powerful source of diversification for asset allocators. For example, since 1990, a standard risk parity portfolio would generate returns with an information ratio of 0.6, while a standard quantitative portfolio would generate returns with an information ratio of 0.4. But the blend of thew two portfolios would generate returns with an information ratio of 0.9. The near additive nature of different portfolio return-to-risk ratios suggests significant diversification potential, regardless of whether or not asset allocators are leading factor investors, or why. The reality is that asset allocation and factor investing are sufficiently out-of-synchronization – sufficiently less-than-perfectly correlated, to create diversification. And this makes intuitive sense, because factors are not straight plays on beta. Conceptually, momentum is not just beta per se, but rather, beta conditional on yesterday’s trends. Value might look like “beta left behind” today – but longer term, the strategy has an impressive positive and right skew, because of its mean reversion properties. And then there is quality – a factor that cannot be defined simply as low-beta, because there are other dimensions to consider in buying high price-to-book multiple stocks – such as profitability, payout and growth. Finally, although history strongly suggests that assets lead factors, we cannot, and should not dismiss the possibility that factors can feed back into assets. After all, many asset allocators are actively thinking about how to cut their portfolios by factor exposure, rather than asset exposures. And the more popular passive factor investing becomes, the more likely it is that we will see pricing dislocations in markets similar to those caused by passive asset allocators in recent years. If only someone would insert statistically significant, and active layers into asset allocation and factor investing processes … but this would require timing the market, as opposed to time in the market. It would require ongoing quantification of risk premia on offer, and not just volatility optimisation.

Introducing cross-factor volatility. We mention the importance of factor investing, over and above standard asset allocation, because we think that it adds new information to the investment process. Therefore, it should also add something new to our understanding of market volatility. Using conventional benchmarks, we can split the equity investing universe into at least nine distinct, or pure factors – momentum, value, dividend yield, profitability, growth, earnings certainty, low-leverage, low-volatility, and size. Clearly, some of these factors will be positively, or negatively correlated with others from time to time. For example, momentum and value are natural opposites. But the exercise of decomposing returns into pure factors is designed to minimize correlation longer term. In order to capture extreme swings in factor performance, and extreme swings between factors, we estimate a variable we call “cross-factor volatility”. Simply put, cross-factor volatility is the standard deviation of pooled returns across all pure factors over a given historical window. Again, there is natural cross-factor volatility from the fact that some factors are positively- or negatively- correlated from time to time. But this is where movements in the indicator are more significant than levels. Recently, we note a material increase in cross factor volatility, reflecting extreme movements in momentum, low-volatility value factors, and also numerous swings between these factors in a very short space of time.

Cross-factor volatility adds value to market volatility models. The conventional wisdom is that option-based measures of equity market volatility like the VIX have a symbiotic relationship with realised volatility. That is, they should in principle lead realised volatility, but nevertheless are strongly anchored to it. Therefore, many investors estimate the variance risk premium – the compensation for getting one’s uncertainty forecast wrong over a given horizon – as the spread between the VIX and realised market volatility. There are many problems with this approach, which we do not delve into here. But what we do highlight is that adding cross-factor volatility into the modeling framework adds value over and above realised market volatility. It does more than to replicate realised market volatility because factors are not just alternative expressions of beta. As it turns out, since 2000, we can explain almost 80% of the daily variation in the VIX using realised S&P 500 volatility and realised S&P 500 cross-factor volatility, estimating both input variables over consistent windows. A 1% increase in realised market volatility corresponds with an 0.4% increase in the VIX, while a 1% increase in cross-factor volatility corresponds with an 0.9% increase in the VIX. Importantly, model forecasts powerfully anchor actual VIX readings, making it possible to profit on paper from valuation signals. Buying (selling) the VIX when it is cheap (expensive) on our model generates significant excess returns on even daily horizons, with an information ratio of 1.3 since 2000. For what it is worth, at time of writing, our VIX model is suggesting tactical “fair value” of 35%, compared with the actual level of 36.1%. Even more interestingly, we note that it is the recent rise in cross-factor volatility which would have helped us to identify a spike in the VIX, if only on a mark-to-market, or “catch up” basis. When the VIX was pushing down towards 25% in early June, it felt as if volatility was much higher than this, looking at the incredible factor rotation that was occuring. In contrast, realized S&P 500 volatility would not have given us much of an early warning.

Longer-term, cross-factor volatility helps to predict market volatility. We recognise that most readers are not high frequency volatility traders. Nevertheless, we suspect that most would recognise that the VIX is becoming increasingly important as a risk signal in light of the shift over the past decade towards passive and risk parity investing. And if there is anything that can help us to forecast it strategically, and not just tactically, it would be quite welcome. With all of this in mind, we note that the ratio of realised cross-factor volatility to realised market volatility is a very useful year-ahead leading indicator of VIX movements. Specifically, when cross-factor volatility is high (low) relative to realised market volatility, we tend to see the VIX rise (fall) in the year ahead. Recently, we note that the ratio of cross-factor volatility to realised market volatility is starting to rise off low levels. We think that the VIX is likely to gravitate towards lower levels foreshadowed by the futures curve in the period ahead – but we also recognise that there are complicating factors which make the path of volatility more volatile. Fundamentally, we are concerned about a potential second wave of COVID-19, rising corporate insolvencies, inflation risks, plumbing problems in money markets and policy errors. But we also think that these risk factors are likely to manifest in heightened cross-factor volatility first, as perhaps we are now seeing.

A sobering lesson from the dual nature of light. In quantum mechanics, there are times when light behaves like a wave, and other times when it behaves like a particle. Indeed, the duality is so complex, that when scientists try to measure light as a wave (particle), it starts to behave in the opposite fashion as a particle (wave). We think that the dual nature of light is something we can learn from to better understand and respect the boundaries of asset allocation and factor investing. Specifically, if the investment world mores too far in favour of passive investing, the risk is that active managers will find more obvious pricing dislocations to profit from, and will start to rise to the fore at the expensve of passive. On the flipside, if everyone chooses to go the way of factor investing, the risk is that conventional asset allocation will become more attractive. There is a natural balance between active and passive investing, as well as between asset allocation and factor investing. The most robust approach is to take all approaches into account, and recognise the circumstances in which each flourishes or fails. With this in mind, we think it incredibly important that investors monitor the predictive power of cross-factor volatility. We note that in the years that passive investing has started to dominate, that the predictive power of cross-factor volatility relative to realised market volatility for the VIX has also risen. This development has not been a coincidence in our view, and indeed, warrants close examination.

What else would you expect when the entire market is the fantasy of competing macro algos?

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.