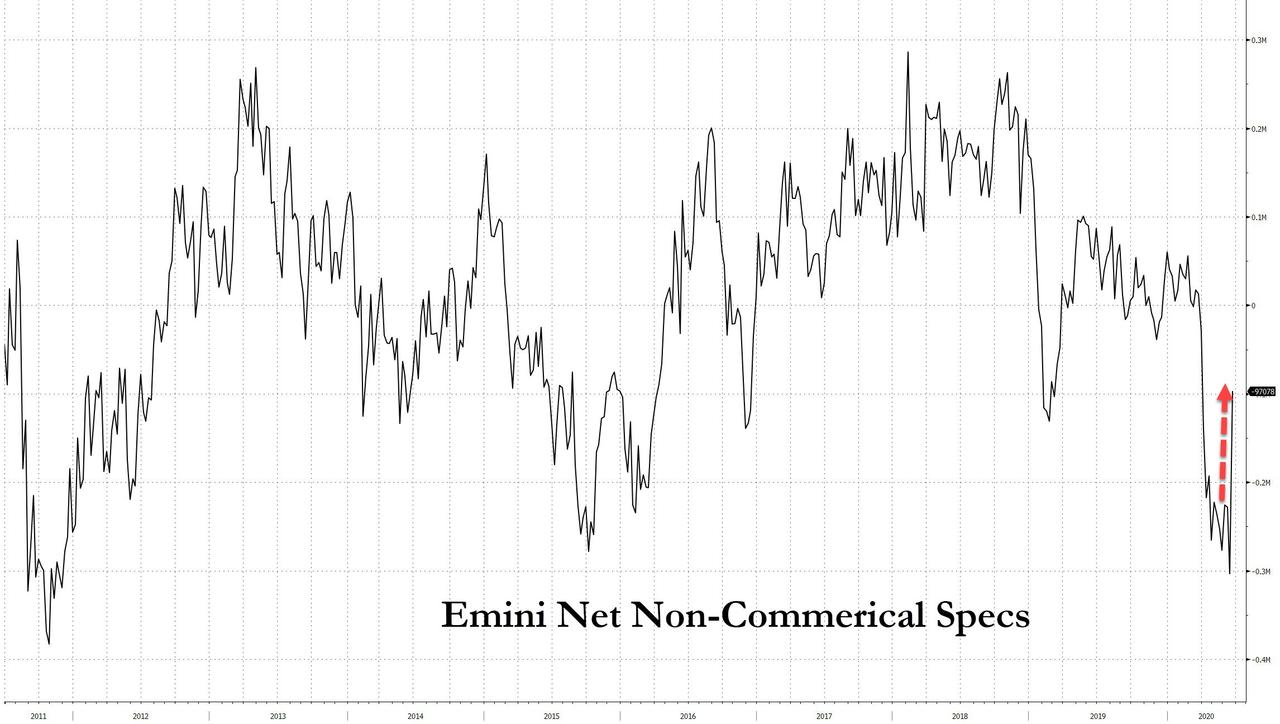

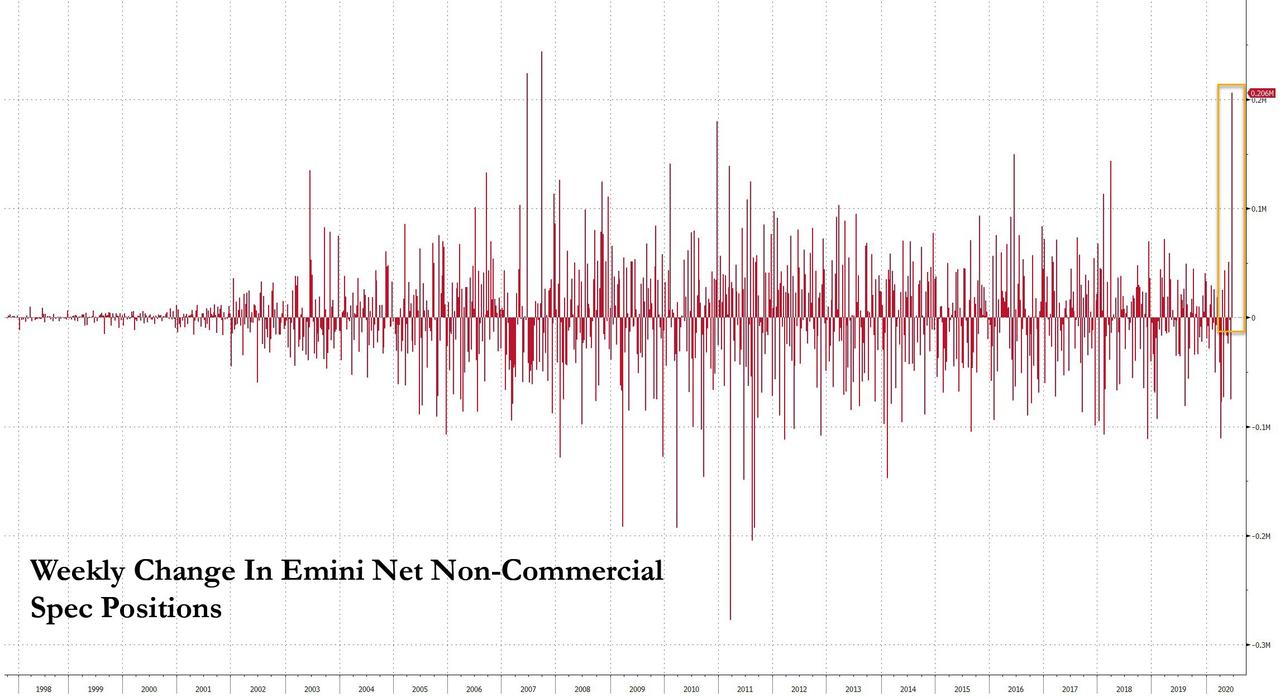

After three months of relentless contrarian bearishness by institutional investors, even as retail investors first, and hedge funds subsequently (latest HF net leverage is 99%-ile) flooded into stocks, large institutions such as vanilla mutual funds and pensions finally capitulated to the Fed which is now openly pushing stock prices higher. In the CFTC’s latest weekly futures data, the amount of net short covering of Emini futures among non-commercial speculative investors exploded, and was the biggest since 2007 and the third highest on record.

As a result, in the week ended June 23, ES net specs surged to -97,078 from -303,305 which was the biggest ES net short position since the Sept 2011 US credit rating downgrade. The collapse in short exposure of more than 206K contracts was the third biggest on record, and was surpassed only by two short-squeezes observed right around the time of the great quant crash in the summer of 2007.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.