US consumption disappoints pre-“second-wave”. US consumption rose by a smaller-than-expected 8.1% in May, albeit with upward revisions to prior months’ data. More timely retail sales, chain store turnover and card spending data have been pointing to a stronger recovery, which has not manifested yet in the official data. The rise in consumption occured despite contraction in disposable income, implying a sharp drop in the household saving rate to 23.2% of disposable income from 32.2%. Nevertheless, even after the drop, the household saving rate has still settled at unusually high levels relative to fundamentals. From this starting point, one could easily argue that there remains plenty of room for growth in consumption. However, we have a few short-term concerns. Firstly, it is hard to disentangle forced saving from discretionary saving, especially when fiscal stimulus is so large and volatile. After all, fiscal deficits create deposits which force money on to the private sector. This money must inevitably show up in either corporate or household saving. At any given point in time, it is hard to know whether household saving is falling by choice, or because the fiscal deficit is fluctuating. Indeed, with the sheer magnitude of stimulus injected into the system in April and May, there is argument that spending growth should be stronger … Secondly, the evidence is that a second-wave of COVID-19 is a clear and present danger, meaning that further economic shutdowns (either imposed by the government or self-imposed by the private sector) are a risk. Thirdly, the US consumer is the buyer of last resort of goods and services produced globally. If US consumption growth does not recover strongly enough, it will be difficult to engineer a strong recovery in world industrial production (IP) without significant currency (USD) weakness to help preserve trade financing conditions and prevent shrinkage in global supply chains, in turn to support a decent re-stocking bounce.

Productivity growth improves, but unit labour costs still rise solidly. We maintain and monitor a monthly real gross domestic product (GDP) tracker based on timely partial indicators such as consumption, non-defence capital goods shipments, government expenditure and construction activity. Alongside this tracker, we also use payrolls and average hourly earnings data to monitor unit labour costs and the labour share of GDP. Our GDP tracker works well because consumption represents the lion’s share of GDP, and is rather accurately and well covered among the partial indicators. Most of the partial indicators are looking healthier in May, supporting a bounce in monthly real GDP of around 7%. This bounce in real GDP is ahead of the rise in aggregate hours worked, supporting a recovery in productivity growth. In year-ended terms, growth in our productivity tracker picks up to 3.3% from a negative rate previously. However, we note that the economy’s total wage bill is falling at a considerably slower pace than real GDP in year-to-May terms (-6.3% versus -9.1%), consistent with a rise in unit labour costs of 3.1%. Nominal wages are running ahead of productivity. Indeed, even real wages are running ahead of productivity (headline personal consumption expenditure deflator inflation of 0.5%, core inflation of 1%), mathematically consistent with a rise in the labour income share of GDP. It seems that the labour share of GDP is on the rise for two consecutive quarters despite two consecutive quarters of negative real GDP growth and extreme loosening of labour market conditions undermining wage bargaining power. The output gap is proving both difficult to measure and conceptually problematic in such unprecedented times, as supply is being challenged as much as demand by permanent business closures and supply chain disruptions, not to mention the unwillingness or inability of US workers to take pay cuts. But perhaps a good place to start is to recognize that the output gap pre-crisis was probably much tighter than many people thought, a conclusion supported by negligible rates of potential GDP growth embedded in inflation-indexed bond yields.

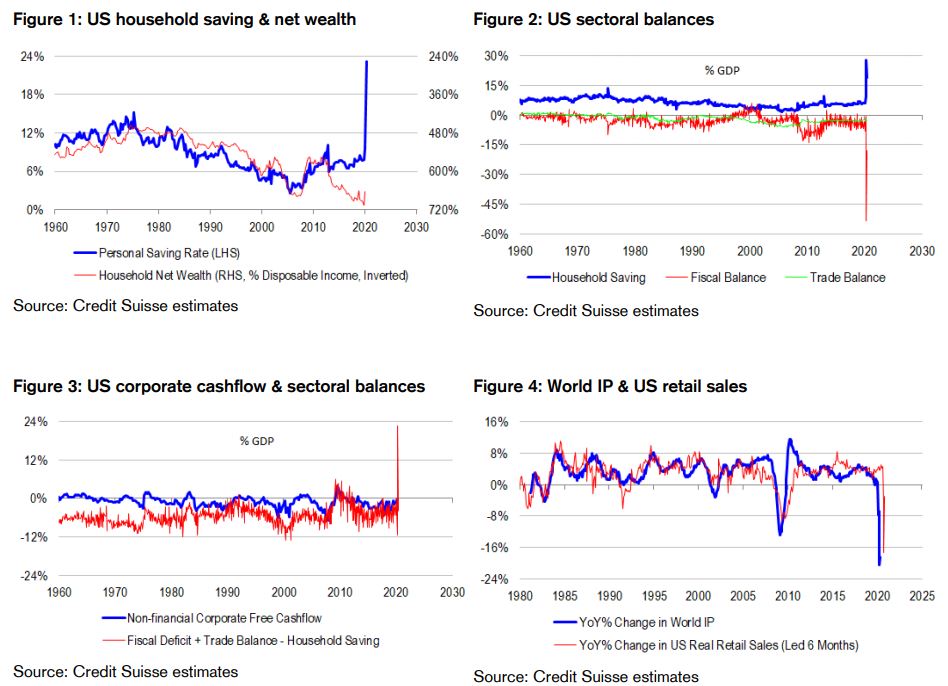

Stimulus impulse to corporate profit margins falls flat. The so-called Kalecki equation for corporate profits, based on the national accounting identity, is pointing to the impulse from large scale fiscal stimulus falling flat in May. The sum of saving across all sectors must equal zero. In other words, the sum of household, corporate, government and foreign saving must net out to zero. Re-arranging, corporate saving must equal the trade balance plus fiscal deficit minus household saving, while corporate profits must equal this subtotal plus business capex. Indeed, historical relationships suggest that corporate free cashflow is highly correlated with the residual of other sectors’ balances. In May, we note a sharp narrowing of fiscal deficits to 18% of GDP from 53%, while household saving falls to 19% of GDP from 28%, and the trade balance deteriorates modestly to -2.9% from -2.7%. In other words, fiscal fade greatly overshadows the fall in household saving. Mathematically, corporate saving suffers. And when we consider that business investment only increases moderately in May (as evidenced by a small 1.8% rise in non-defence capital goods shipments), this also means that the impulse to corporate profits from stimulus drop off. Corporate profits as a share of GDP, or profit margins could come under pressure. Of course, this state of affairs could very easily change, or take a little while to materialise in the official data. But our point is to highlight that fiscal stimulus is significantly distorting the data we are monitoring and is therefore a significant source of volatility, especially when the comparables are unfavourable. The private sector is not yet ready to stop holding the public sector’s hand.

Cost-push pressures could still drive inflation ahead of growth. A rising labour share of GDP has historically been a source of inflation pressure. The labour share should have fallen in the circumstances, but clearly has moved against the grain of economic and labour market weakness. There was, and remains a risk that corporates could take advantage of the stimulus-fuelled environment to pass through cost pressures. May data suggests that this window of opportunity was quite limited. There was and remains a risk that wage outcomes could catch down to the weaker state of the economy with a longer-than-normal delay. Nevertheless, there has clearly not been the deflationary consequences we would have expected from such a sharp shock to the economy. And going forward, should the economy recover or supply chain disruptions linger (or worsen), we could see higher inflation than what the bond market is looking for. Indeed, the wider dispersion of potential inflation outcomes alone should warrant higher pricing of inflation “break-evens”.

Long quality and commodities, short momentum and value. Uncertainty is high geo-politically, medically and with respect to inflation. This undermines our confidence in following yesterday’s trends and momentum investing. In any case, momentum is starting to become more equivocal in its defensive-cyclical bias. We are concerned also about value investing given that there are still material de-leveraging pressures to contend with, masked only by fiscal stimulus which is in itself fading and volatile. Indeed, we note that bank credit is starting to fall, but this decline can go unnoticed for as long as the public sector is levering up. We are long quality for both inflationary and deflationary regimes. The deflation case for quality is self evident, while the inflationary case revolves around the de-risking that could occur should passive and risk parity funds get wrong-footed in their assumptions about lower-for-longer bond yields and lower-for-longer volatility. Finally, we think there is a bit more inflation in the pipeline than what markets expect, and look for more re-rating in inflation hedges like commodities. From an Australian investor perspective, we note that gold and large-capitalisation resources names also screen well for quality either on historical beta, or strength of balance sheets.

It’ll only get worse while the second wave intensifies.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.