AMP Capital chief economist Shane Oliver says that while consumer confidence and spending is recovering, the Australian economy faces a long road back to recovery:

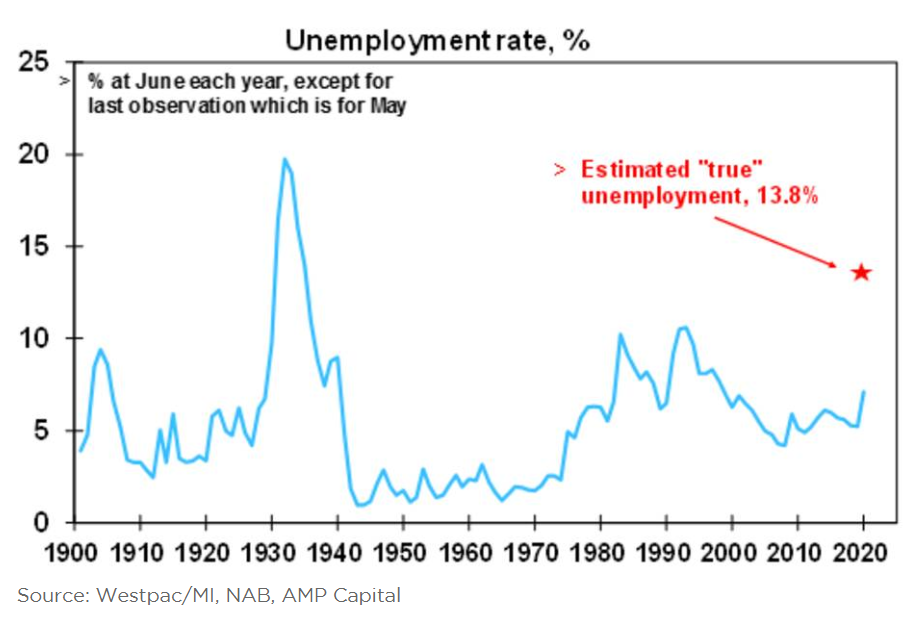

ABS labour force data showed a further sharp deterioration in the Australian labour market into mid-May with employment falling another 228,000 and unemployment rising to 7.1%. This is worse than economists including ourselves expected but still far better than we expected a month or two ago when we saw unemployment going rapidly up to just below 10% this quarter. Whatever it is it’s a devastating outcome for those impacted.

The bad news is that the “true” unemployment rate is probably a lot higher than 7.1%. The change to JobSeeker that allows people to receive it and not have to look for work has contributed to a 3% decline in the participation rate (from 65.9% to 62.9%) since March. If the participation rate had only fallen by around 1% as occurred in the early 1990s recession unemployment would have risen to 10%. Furthermore, JobKeeper covering 3 to 3.5million jobs has prevented an even steeper fall in employment – a rough guesstimate of which is around 500,000 jobs. If this is also allowed for it would take the “true” unemployment rate up to around 13.8% which would be the highest since 1935.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.