By Chris Becker

Stock markets continue to diverge from economic reality with Wall Street lifting higher despite rising civil unrest and growing tensions with China over Hong Kong and other trade disputes. The latest ISM manufacturing survey had some glimmer of hope within but still showed extremely weak conditions across the US as unemployment ravages the country. The USD is down to a three month low with all the majors surging again while US Treasuries yields lifted slightly.

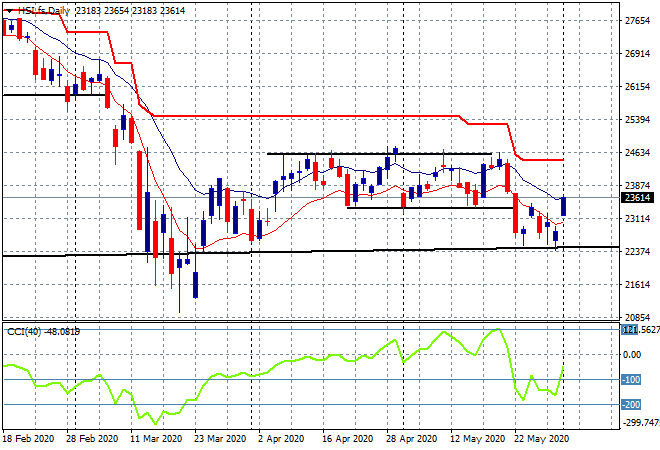

Looking at share markets in Asia from yesterday’s session where in mainland China, the Shanghai Composite was up more than 2% in reaction to the non-reaction from the US on trade disputes with Hong Kong, closing at 2915 points, while the Hang Seng Index gapped over 3% higher to 23735 points. This brings price well back above previous firm support at the 23300 point level, after briefly toying with breaking back down to the March lows, but not yet out of the woods: