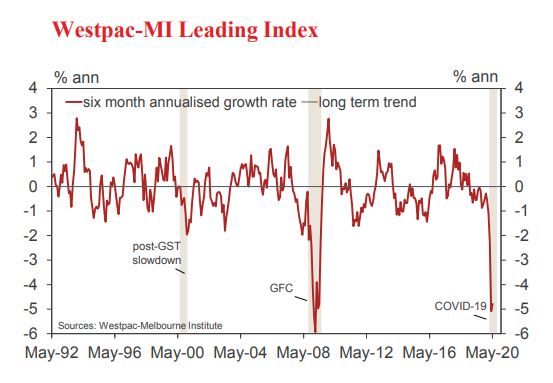

Despite the slight improvement, the Index growth rate remains in deep negative territory consistent with an economic recession.

Following the release of the March quarter national accounts, which showed the economy contracting by 0.3% in the March quarter, Westpac revised its forecast for the cumulative contraction in the economy for the first half of 2020 from 8.8% (0.4% in Q1 and 8.4% in Q2) to 7.3% (0.3% in Q1 and 7% in Q2). That reflected an earlier than expected easing of restrictions in the June quarter, although a deep recession is still forecast which is consistent with the signal from the Leading Index.

The Leading Index growth rate has weakened sharply over the last six months, dropping from –0.28% in December to the –4.79% in May. Two components account for the bulk of the 4.5ppt slump: US industrial production (–3.3ppts) and aggregate monthly hours worked (–1.8ppts). Both have been directly impacted by the COVID-19 health emergency and associated shutdowns – US industrial production plunged 15.3% between February and April, and hours worked in Australia dropped by 9.2% in the April month alone. Equity markets have provided an additional 0.6ppt drag although the S&P/ASX 200 has now clawed back about a third of the sharp sell-off in February–March.

Other components have seen net improvements over the last six months, adding to the Index growth rate. The most notable positive contributions have been from commodity prices, measured in AUD terms (+0.5ppts); the yield spread (+0.2ppts); and Consumer Unemployment Expectations (+0.2ppts) – the latter dropping sharply in March-April only to regain all of these losses in the last few months.

The Reserve Bank Board next meets on July 7. The minutes of the June Board meeting noted that it was possible that the downturn would be shallower than earlier expected. Accordingly, it seems likely that when the Bank releases its revised growth forecasts on August 7 it will adjust its current forecast for a 6% contraction in the economy over 2020 to something more in line with our own revised view – still a huge contraction but, nevertheless, ‘shallower’ than previously expected.

Policy is set to remain firmly on hold for the foreseeable future. Westpac currently expects the 0.25% target for the three year bond rate to be adjusted in 2022 while the 0.25% cash rate will remain in place beyond the end of 2023.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.