APRA has released its weekly update on the federal government’s early superannuation release policy, which reveals that another $1,590 million funds were withdrawn in the week ending 24 May, with total withdrawals topping $12.2 billion:

As illustrated above, just over 1.6 million applications have been paid averaging $7,252.

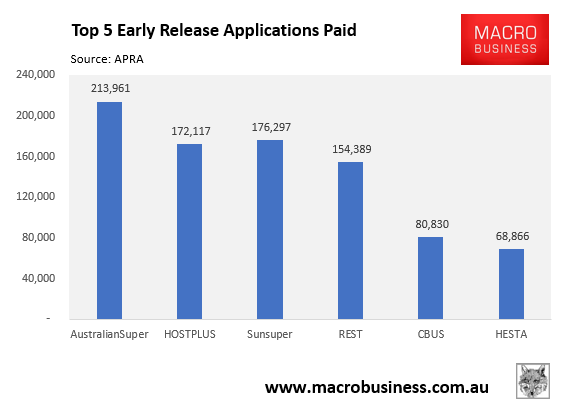

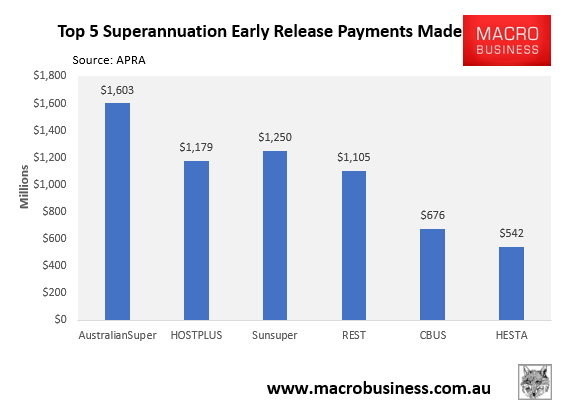

Breaking down withdrawals at the individual fund level, we can see that industry funds suffered the six biggest draw downs, with the below six funds alone accounting for just over half ($6.4 billion) of total early superannuation withdrawals:

Given superannuants are permitted to withdraw an additional $10,000 from their funds from 1 July, we are likely to see more heavy withdrawals from industry funds, whose member base is generally younger and more exposed to COVID-19 job losses.