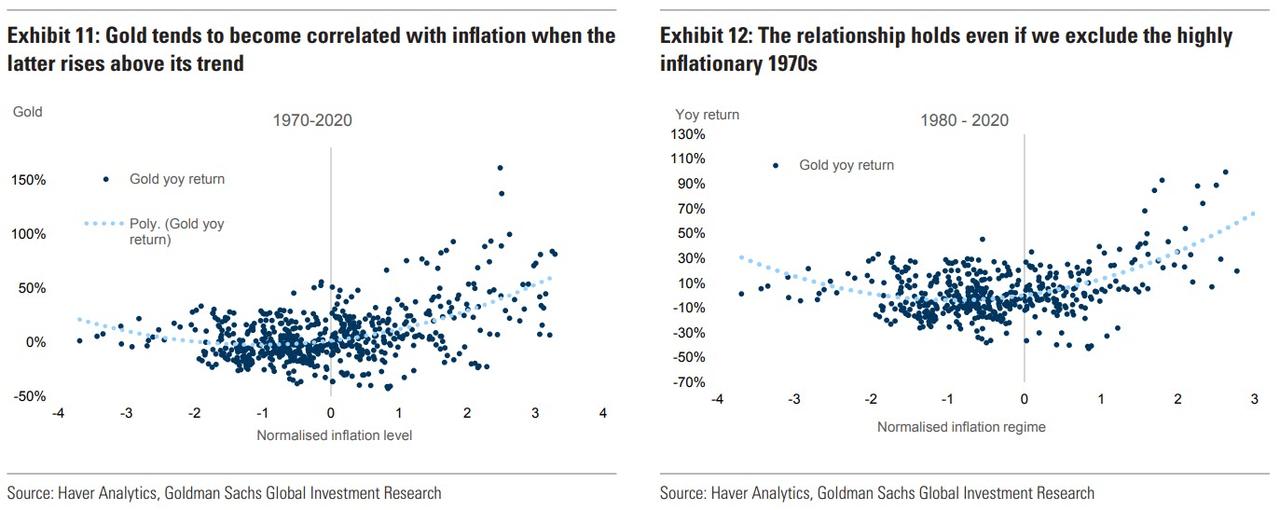

Historically, gold’s relationship with inflation is non-linear. Gold does not display a strong correlation with inflation while the latter is moderate but becomes strongly correlated when inflation gets above a certain threshold. Gold also tends to go up moderately in deflationary environments.

In fact, we find that what matters most is the deviation of inflation from its trend, rather than its absolute level (see Exhibit 11 and Exhibit 12).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.