Via the ABC:

Reserve Bank economists considered urging the Federal Government to shut down the real estate industry, “pausing” sales of established homes to avoid perceptions of a coronavirus-inspired housing market crash.

Highly classified documents from inside Australia’s central bank also suggest house prices could slump up to 15 per cent.

The internal reports contradict a much rosier public view the Reserve Bank of Australia has been displaying about the billions of dollars and millions of jobs tied up in housing, construction and real estate.

Minutes of the board’s May 5 meeting, released publicly, noted “demand for both new and established housing had fallen” and falling incomes, confidence and population growth “were expected to affect demand for new housing for an extended period”.

But inside the RBA, which sets key interest rates and economic direction, the warnings were clearer and more severe.

“It’s become clear that there has been a big drop-off in demand for new housing,” said speaking notes for assistant governor (economic), Luci Ellis, which were obtained through a Freedom of Information (FOI) request.

Beyond difficulties inspecting and selling houses, people were worried about job security.

“Contracts are being cancelled, early-stage buyer interest is very weak and the pipeline is emptying,” it noted.

“Anything that hadn’t already been started has been deferred”.

A day earlier, there were more stern warnings in a “COVID-19 liaison messages update”.

“Demand for new housing has declined substantially since mid-March and is expected to decrease further,” it read, with “sharp falls in sales, enquiries and foot traffic [and] increases in contract cancellation rates”.

A sharp fall in house prices is predicted in a note marked “highly restricted” and created on April 18.

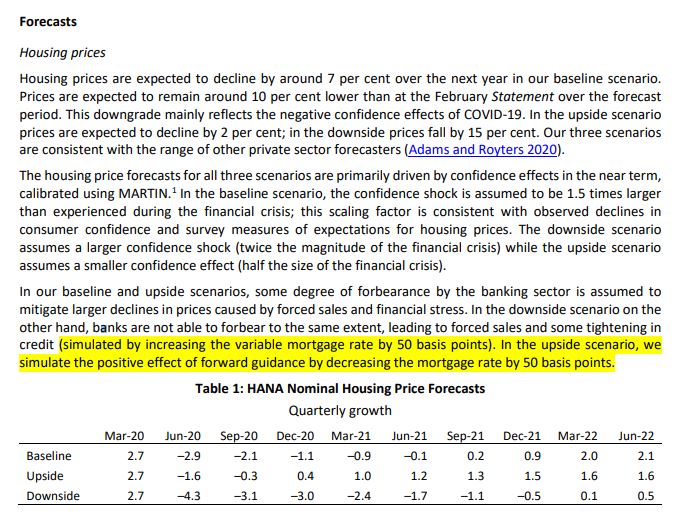

“Housing prices are expected to decline by around 7 per cent over the next year. Prices are expected to remain around 10 per cent lower than at the February Statement over the forecast horizon,” it read, putting most of this down to a loss of confidence because of COVID-19.

The overall security of the banking sector — and its ability to weather some mortgage failures — will “mitigate larger declines in prices caused by forced sales and financial stress”.

The fall in house prices could be as little as 2 per cent in the best scenario, “in the downside [worst scenario] prices fall by 15 per cent”.

Real estate shutdown considered

In April, economist Nick Garvin wrote to colleagues, warning them the RBA should stop discussing the housing market as if it were operating normally, and calling for a halt — as happens to stock market trading in emergencies.

“I think it’s dangerous for regulators to be reporting on housing prices as though the market is currently functioning,” he wrote.

The “pause” would not mean there was no activity, he wrote, “although it could indeed be wise to recommend that the [Government] temporarily halt all sales of established dwellings”.

Shutting down real estate sales would send a statement that “we’re in a different category of situation” and that normal reporting of clearance rates and average prices was “misleading”.

Even without shutting all sales, pausing reporting on the market would “be a fair classification” because real estate agents could not work normally.

“If people start mistakenly thinking that we’re experiencing a housing market crash, it’s not going to help things,” he added.

Bank may have prompted HomeBuilder scheme

The RBA’s reports on the deteriorating situation in construction may have influenced the announcement of the Government’s HomeBuilder program in early June.

In an April report marked “highly restricted”, the Reserve Bank warned the industry was staring at a cliff.

“Although some builders and developers have sufficient work for the next four to six months, the weakness in demand for new housing and the potential deterioration of financing conditions pose downside risks to future activity,” it said.

In Melbourne, some of the RBA’s contacts have seen new home sales drop by half.

By May, things were worse: “Builders of detached housing expect weak demand to weigh on construction activity and cash flow beyond their current pipeline (around four to nine months). Builders and developers report that domestic banks and non-bank financiers have become more conservative in their lending.”

“Most firms intend to defer or cancel investment, many firms have reduced staff hours worked (more so than headcount) and an increasing number of firms expect to implement a wage freeze in the year ahead.”

Talk about desperados. Here is the latest forecast from the FOI:

There’s 88 pages of pearl-clutching to go through.